Download

1 / 10

120 likes | 164 Views

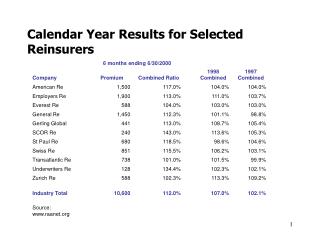

Reinsurers are required to provide loss estimates for 25 catastrophic events, including financial, life insurance, property catastrophes, special lines, man-made catastrophes, and other events, to ensure model completeness and facilitate comparisons. The stress test is a complement to internal models, assessing gross loss, net loss, recoveries, and assumptions.

E N D

Stress Testingfor Reinsurers SST for Reinsurers April 4, 2006

Stress Testing for Reinsurers • Reinsurance companies are asked to provide their loss estimates for approx. 25 catastrophic events • The events are standard events defined by FOPI • The evaluation of the events is a complement to the internal model • Each event is subject to a materiality test • Purpose: • Check list for model completeness • Comparison between companies • The 25 catastrophic events are grouped into six broad categories

Financial Events • Stock market crash 1987 • Nikkei crash 1989 • European currency crisis 1992 • Interest rate scenario 1994 • Russia/LTCM 1998 • Stock market crash 2001

Life Insurance Scenarios • Pandemic scenario • Longevity

Property Catastrophes • European windstorm • UK flood • US hurricane • California earthquake • New Madrid earthquake • Japanese earthquake • Japanese windstorm • Other territories

Special Lines Catastrophes • Aviation catastrophe • Energy catastrophe • Credit event

Other Man Made Catastrophes • Terrorism event • Industry event • Nuclear event

Other Events • Adverse loss developments • Downgrading • Company specific scenarios

Required Information • Gross loss • Net loss • Breakdown of recoveries by major retrocessionaires • Breakdown of gross loss by line of business • Narrative describing the company’s assumptions

Stress Test for Reinsurers • Is a complement to a company’s internal model • Based on comprehensive set of events • Based on standard set of events • Each event is subject to a materiality test