Understanding Your Credit Score: Key Factors and Insights for Consumers

200 likes | 332 Views

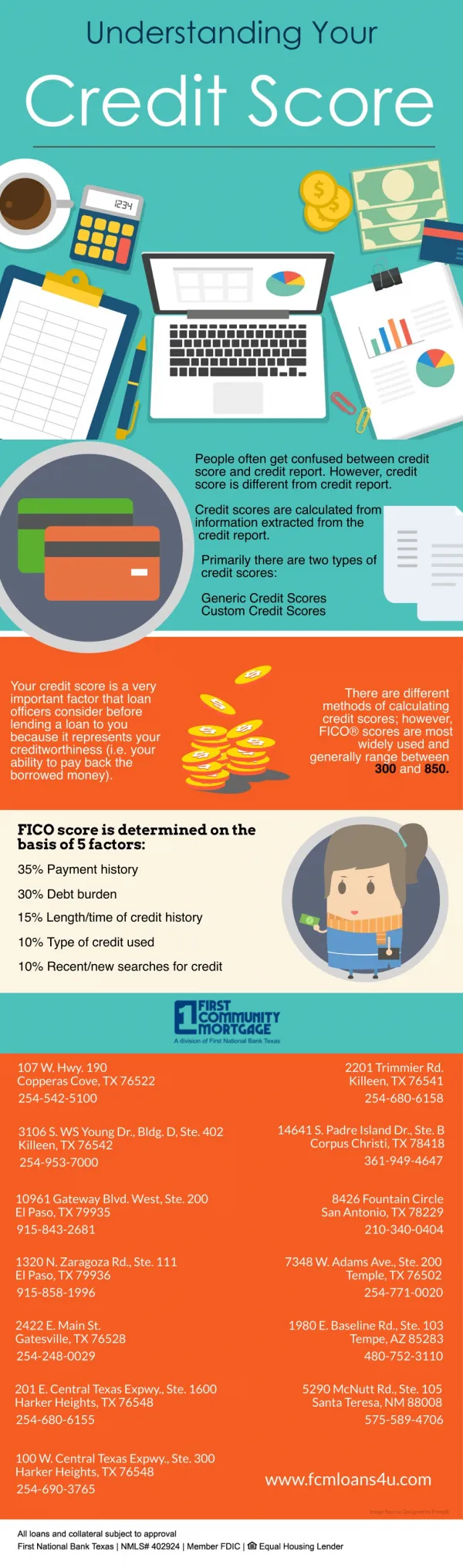

In today's lending landscape, credit scores play a crucial role in determining loan eligibility and interest rates. Developed by Bill Fair and Earl Isaac, the Fair Isaac Credit Scoring model uses mathematical algorithms to predict the likelihood of repayment, replacing outdated methods based on subjective judgment. Credit scores range from 300 to 850, affecting your ability to secure favorable loan terms. Key factors influencing your score include payment history (35%), amounts owed (30%), length of credit history (15%), types of credit (10%), and recent inquiries (10%).

Understanding Your Credit Score: Key Factors and Insights for Consumers

E N D

Presentation Transcript

Understanding Your Credit Score Consumer Credit Nationwide

First -- some background… • In the old days…banks relied on their own records and sometimes even the loan officer’s instincts, (or their gut), when making lending decisions. • Obviously, while this worked some of the time, it wasn’t necessarily the most effective, or fair method of determining whether or not someone was qualified for a loan. • Bill Fair (an Engineer) & Earl Isaac (a Mathematician) came up w/ an idea! • They said that math could better predict future behavior than the “gut” of a loan officer…So • They developed the Fair Isaac Credit Scoring model.

Credit Score defined • A number that attempts to “measure” the odds that someone will pay the bank back if the bank gives that person money

Some other details • Your score is a number between 300 - 850 • A high score means a good credit rating which means your interest rates will likely be lower • A low score means a bad rating, which means interest rates will likely be higher • Your score measures activity over the past 7 years • Giving greatest weight to most recent information (6 months to 2 years)

School Grading Scale 100% - 93% A 92% - 85% B 84% - 70% C 69% - 60% D 60% - 0 F * The above scale ranges may vary. Credit Grading Scale 850 – 720 A 719 – 680 B 679 – 620 C 619 – 600 D 599 – 300 F Median Score 723 Comparing your Credit Score to a Grading Scale in School

What factors are used to make up your Score? • 35% Payment History • 30% Amounts Owed (current balances vs. amount available on credit line)

Remaining Factors • 35% Other • Including: Length of time you’ve had credit (15%) • Types of Credit (10%) • New credit (10%) • Inquiries • Note: The statistical formula that is used create your score is a secret. The above are guidelines that have been given to consumers to help “explain” the score.

Payment History (35%) • Account payment information on specific types of accounts (credit cards, retail accounts, installment loans, finance company accounts, mortgage, etc.) • Presence of adverse public records (bankruptcy, judgments, suits, liens, wage attachments, etc.), collection items, and/or delinquency (past due items) • Severity of delinquency (how long past due) • Collection items • Time since (recency of) past due items (delinquency), adverse public records (if any), or collection items (if any) • Number of past due items on file • Number of accounts paid as agreed • Greatest weight given to the largest payment creditor

Amounts Owed (30%) • Amount owing on accounts • Number of accounts with balances • Debt Utilization Ratios – Amounts owed/Credit Given • Proportion of credit lines used (proportion of balances to total credit limits on certain types of revolving accounts) • Proportion of installment loan amounts still owing (proportion of balance to original loan amount on certain types of installment loans)

Other Factors • Length of Credit History (15%) • The longer you’ve had credit the better your score. • What is measured? • Time since accounts opened • Time since account activity

Other Factors (cont’d) • Types of Credit (10%) • Number of (presence, prevalence, and recent information on) various types of accounts (credit cards, retail accounts, installment loans, mortgages, consumer finance accounts, etc.)

Other Factors (cont’d) • New Credit (10%) • Number of recently opened accounts, and proportion of accounts that are recently opened, by type of account • Number of recent credit inquiries • Time since recent account opening(s), by type of account • Time since credit inquiry(s) • Re-establishment of positive credit history following past payment problems

Inquiries • This is a list of who has been checking your credit. • 2 types of inquiries – • Inquiries you initiate • Ex. You apply for a loan, or apply for insurance • This type of inquiry will have an impact on your score but generally not a significant one. If you are shopping for a loan, the multiple inquiries will have the impact of a single inquiry within a 15 day period. • Inquiries others initiate or self-check of credit • Ex. Bank wants to offer you a pre-approved offer or you check your credit yourself. • The score does not count “consumer-initiated” inquiries – requests you have made for your credit report, in order to check it. It also does not count “promotional inquiries” – requests made by lenders in order to make you a “pre-approved” credit offer – or “administrative inquiries” – requests made by lenders to review your account with them. Requests that are marked as coming from employers are not counted either.

Income Gender Race Age Zip Code Credit Counseling What is not in your Score?

Facts and Fallacies • Fallacy: My score will drop if I apply for new credit.Fact: If it does, it probably won't drop much. If you apply for several credit cards within a short period of time, multiple requests for your credit report information (called “inquiries”) will appear on your report. Looking for new credit can equate with higher risk, but most credit scores are not affected by multiple inquiries from auto or mortgage lenders within a short period of time. Typically, these are treated as a single inquiry and will have little impact on the credit score. (Myfico.com)

Facts and Fallacies • Fallacy: A poor score will haunt me forever.Fact: Just the opposite is true. A score is a “snapshot” of your risk at a particular point in time. It changes as new information is added to your bank and credit bureau files. Scores change gradually as you change the way you handle credit. For example, past credit problems impact your score less as time passes. Lenders request a current score when you submit a credit application, so they have the most recent information available. Therefore by taking the time to improve your score, you can qualify for more favorable interest rates.

How do I improve my score? • Pay all bills on time • Pay off old collection accounts • Get current & Stay current • Keep balances low in relation to credit limits • Only use credit when needed

How do I get a copy of my Credit Report? • By Phone: 877-322-8228 • By Web: www.annualcreditreport.com • By Mail: Annual Credit Report Request Service P.O. Box 105281 Atlanta, GA 30348-5281

Identification Name Address Soc. Sec. Number Year of Birth Gender Employer Address Public Information Bankruptcies Judgments Tax Liens Account History Company Name Acct Number Type of account Date Opened Date Reported Credit Limit Highest Balance Current Balance Monthly Payment Past Due Amount Payment History for last 24 mos. What information is on my Credit Report?

Additional Questions?Please contact us: Consumer Credit Nationwide 3509 Spring Street * Suite 4 Davenport, Iowa 52807 563-359-8830 * 800-Debt Help (332-8435) Info@800DebtHelp.com