Download

1 / 17

320 likes | 611 Views

CHAPTER 7. ACCEPTING THE ENGAGEMENT AND PLANNING THE AUDIT. Client acceptance and Retention. Step associated with Client Acceptance and Retention. Evaluating the Integrity of Management. Communicate with Predecessor Auditor. Make inquiries of Other Third Parties.

E N D

CHAPTER 7 ACCEPTING THE ENGAGEMENT AND PLANNING THE AUDIT

Evaluating the Integrity of Management Communicate with Predecessor Auditor Make inquiries of Other Third Parties Review Previous Ecperience with existing Clients

Identifying Special Circumstances and Unusual Risk Assess Prospective Client’s Legal and Identify Intended Users of Audited Statements Identify Scope Limitations Evaluate the Entity’s Financial Reporting Systems and Auditability

Evaluating Independence Identify Circumstances Impairing Independence Identify Professional Staff Financial and Business relationships Identify Conflicts of Interest with other clients

Making the Decision to accept or Decline the Audit Integrity Of Managemet Special Circumstances and Unusual Risks Competence Issues Independence Issues

Preparing The Engagement Letter • Clear identification of entity and financial statements to be audited • Objective or purpose of the audit • Reference to professional standards to be followed

Preparing The Engagement Letter • Explain nature and scope of audit and auditor’s responsibilities • Statement that not all material fraud may be detected • Reminder of management responsibility for financial statements and internal controls • Indicate potential request for written representations

Preparing The Engagement Letter • Describe any auxiliary services to be provided • Basis on which fees will be computed and billing arrangements • Request to confirm terms of engagement by signing and returning a copy to the auditor

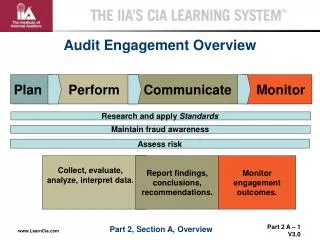

Key Steps in Performing Risk Assesment Procedures 1 Identify relevant financial statement assertions Obtain an understanding of the entity and its environment 2 3 Making preliminary judgements about materiality 4 Perform analytical procedures

Key Steps in Performing Risk Assesment Procedures 5 Consider audit risk, including the risk of fraud Develop preliminary audit strategies for significant assertions 6 Obtain an understanding of the entity’s system of internal control 7

Key Steps in Understanding The Entity and Its Environment Obtain an understanding of the entity and its environment • Industry, regulatory, and other external factors • Nature of entity, including selections and application of accounting policies • The entity objectives, strategies, and related business risks. 1

Key Steps in Understanding The Entity and Its Environment Develop a knowledgeable perspective about the entity’s and its financial statements 2 3 Asses the risk of material misstatements In order to asses the risk of material misstatements, and auditor should examine internally generated information used by management and external (third party) evaluations of the company.

Measurement and Review of the Entity’s Financial Performance An auditor might consider before performing analytical procedures during the planing phase : • Key ratios and operating statistics • Key performance indicator • Employee performance measures and incentive compensation policies • Use of forecasts, budgets and variance analysis • Analyst reports and credit rating reports • Competitor analysis • Period-on-period financial performance ( revenue growth, profitability, leverage) • Trends.