Download

1 / 35

350 likes | 549 Views

Applications of RQA to Financial Time Series. F. Strozzi 1 , J. M. Zald à var 2 and J. P. Zbilut 3. 1 Quantitative Methods Institute, Carlo Cattaneo University, Castellanza (VA), Italy 2 European Commission, DG Joint Research Centre, IES, Ispra (VA), Italy

E N D

Applications of RQA to Financial Time Series F. Strozzi1, J. M. Zaldívar2 and J. P. Zbilut3 1Quantitative Methods Institute, Carlo Cattaneo University, Castellanza (VA), Italy 2European Commission, DG Joint Research Centre, IES, Ispra (VA), Italy 3Department of Molecular Biophysics and Physiology, Rush Medical College, Chicago, USA

Outline • High frequency financial data sets • Use of RQA (% Recurr) for detecting correlation between time series. • Use of RQA (% Det, %Lam) to distinguish financial time series from surrogate (linearly correlated noise). • Use of RQA (%Det, %Lam) for measuring volatility in financial data sets • Conclusions

High Frequency Financial Data Sets They are observations on financial variables taken daily or at a finer time scale. They have been widely used to study market microstructures. They are also useful for studying the statistical properties, volatility in particular, of asset returns at lower frequencies. They are irregularly spaced and they need a preliminary treatment. HFDF96, exchange rates -->correlation Spot electricity prices --> surrogate, volatility

High Frequency exchange rates • Belgium Franc (BEF) • Finnish Markka (FIM) • German Mark (DEM) • Spanish peseta (ESP) • French Frank (FRF) • Italian Lira (ITL) • Dutch Guilder (NLG) • ECU (XEU) • Australian Dollar (AUD) • Canadian Dollar (CAD) • Swiss Frank (CHF) • Danish Krone (DKK) • British Pound (GBP) • Malaysian Ringgit (MYR) • Japanese Yen (JPY) • Swedish Krona (SEK) • Singapore Dollar (SGD) • South African Rand (ZAR) • HFDF96:Olsen & Associates,high freqency, ½ h, Exchange rates between the US Dollar and 18 other foreign currencies from 1.1.1996-31.12.1996 Historical events in 1996: • 14 October FIM joined ERM • 25 November ITL retunes in ERM ERM=Exchange Rate Mechanism

exchange rates: data treatment • HFDF96 logarithmic medium price ym normalised data [0-1]

Correlation in HFDF96: %recurrence on epochs • Time delay Dt (first minimum of the mutual information function): 232-283 i.e. 4.8-5.9 days. • Embedding dimension dEusing False Nearest Neighbour algorithm and E1&E2 methods: 7-14 Dt=260 dE =11 Epochs of 336 points (1 week) shifted by 48 points (1 day). Linear correlation coefficient CHF XEU

%recurr: correlation coefficients for the high frequency currency exchange rates time series

Stable Distribution Is it possible to distinguish between real and random stable distributed data? A stable probability distribution is defined by the Fourier transform of its characteristic function a(0,2], b[-1,1] g[0,) d(-,) • is the tail index, β is a skewness parameter • is a scale parameter, is a location parameter : Gaussian Chauchy Levy

Fitting and generating stochastic data with stable distributions • Using STABLE for univariate data http://www.cas.american.edu/~jpnolan • We fitted the distribution of the first difference y(t+1)-y(t) with a stable distribution. • All zeros values were eliminated. After they were introduced at the same locations in the random time series. Fitted density plot for the Japanese Yen (JPY) exchange rate data

Correlation coefficients for the stochastic time series with the same stable distribution and zeros

Comparison financial time series- stochastic stable distribution time series using RQA Sign test: Null hypothesis: the median of correlation coefficient for real data is the same that the median of correlation coefficient for stable random data In 96 pairwise comparisons, over 153, on the currency exchange rate time series, the values of the correlation coefficients are higher than the higher value for the random time series, i.e. 0.646. the null hypothesis can be rejected at 5% level of significance if nmedianrefers to the number of observations lower than the median of random stable data. n is the total number of observations.

Figure 100. Plot of the %recurrence for the Euro and the Finnish Markka. Blue values before the entrance in the EMS, green values after the entrance.

Use of RQA to distinguish electricity spot prices from surrogate (linearly correlated noise).

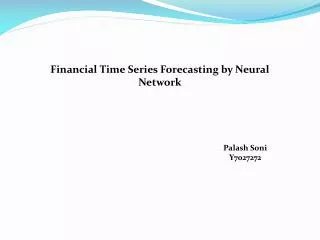

High Frequency spot electricity prices Hourly spot prices in the Nordic electricity market (Nord Pool) from January 1999 until January 2007.(EUR/MWh) Hourly spot prices in the Nordic electricity market (Nord Pool) from May 1992 until December 1998. (NOK/MWh) Norway Statnett Market Sweden Nord Pool Finland W Denmark E Denmark Kontek 1996- EU Electricity Directive starts to have impact: EU countries open their electricity markets to competition ( high consumers can choose their provider). 1993- Nord Pool (Nordic Electricity Market) was created by Norway. …… 2005-KT area. (Kontek cable connection Zealand-Germany). A competition starts between Nord Pool and European Energy Exchange (EEX)

Spot electricity price: dependencies • The variation of the prices in the Nord Pool system is well correlated with the variations in precipitations because of its dependence from hydropower generation. • In the “dry” periods the price and its volatility increase due to the dependence from other source of energy (petrol)

Surrogate data: Null hypothesis Linearly correlated noise. The null hypothesis : the time series are originated by a linear random process with the same autocorrelation function or, equivalently, with the same Fourier Power Spectrum. etis un uncorrelated Gaussian noise of unit variance s is chosen so that the variance of the surrogates matches with the one of original data ak contain information on Correlation function

Surrogate data: discriminating statistic Q The dynamic is chaotic? Q = Correlation dimension Q = Lyapunov exponent Q = Forecasting error Are there differencies in the RP structures? Q = RQA measures

Electricity spot prices: Recurrence Plots EUR/KMh t =13, dE =10, e=10 NOK/MWh t=15, dE=10, e=40

Recurrence Plots: Surrogate linearly correlated NOK/MWh t=15, dE=10, e=40 EUR/KMh t =13, dE =10, e=10

Use of RQA for measuring volatility in electricity spot prices

Volatility Higher %determinism and %laminarity mean that the states of the system stay closer in time for longer periods forming diagonal or vertical segments in RP. Hypothesis: higher %determinism or %laminarity implies smaller volatility There are three main types of volatility: • Realized volatility, also called hystorical volatility determined by past observation. Standard deviation of the change in value of a financial instrument with a specific time horizon . • Model volatility: a virtual variable in a theoretical model such as GARCH or stochastic volatility. • Implied volatility: a volatility forecast computed from market prices of derivatives such as options, based on a model of underlying process (such as log-normal random-walk).

Volatility Inverse of standard deviation and %determinism (top) and %laminarity (bottom) for EUR/MWh Inverse of standard deviation and %determinism (top) and %laminarity (bottom) for NOK/MWh 720 point window (one month), data are shifted 720 points

Volatility: NOK/MWh Nonlinear metrics of the Nord Pool spot prices time series in NOK/MWh: Values are computed from a 720 point window (one month), data are shifted 720 points. RQA parameters: t =15, dE=10, distance cutoff: max. distance between points/10, line definition: 100 points (~4 days). Vertical lines correspond to the following dates: 1st January 1993, 1st January 1996, 29th December 1997 and 1st July 1999 (see historical background).

Volatility: EUR/MWh RQA measures of EUR/MWh: Values are computed from a 720 point window (one month), shifted of 720 points. RQA parameters: t =13, dE=10, distance cutoff: max. distance between points/10, line definition: 100 points (~4 days). Vertical lines correspond to the following dates: 1st October 2000, 5th October 2005 (see historical background).

Conclusions Correlation (exchange rates) • A method to assess the correlation between time series was developed based on %recurrence. • Series in EUR zone (BEF, FIM, DEM, ESP, FRF, ITL, NLG) were highly correlated (R~0.9) in 1996 but also JPY-CAD-GPB. • HFDF96 time series are more correlated than stable distribution random time series. Surrogate (Electricity spot prices) • Using RQA it is possible to distinguish between spot electricity prices and linearly correlated noise. Volatility (Electricity spot price) • %determinism & %laminarity could provide a new measure of volatility in financial time series.

Volatility: r2 • NOK/MWh %Det-1/Std r2=0.4740 %Lam-1/Std r2=0.5809 %Lam-%Det r2=0.8804 • EUR/MWh %Det-1/Std r2=0.4683 %Lam-1/Std r2=0.4512 %Lam-%Det r2=0.8870 %Det-1/Std, %Lam-1/Std not very linearly correlated

Recurrence Quantification Analysis (RQA) The concept of recurrence plot (RP) was introduced by Eckmann et al. (1987) as follows: Let be the reconstructed delayed vector. Then, it is possible to define the distance matrix D as If this Euclidean distance falls within a defined radius, r, the two vectors are considered to be recurrent and graphically this can be indicated by a dot. Finnish Markka-US dollar (HFDF96) Malaysian Ringgit-US dollar (HFDF96) Swiss Franc-US dollar (HFDF96) http://homepages.luc.edu/~cwebber/

Introduction: Recurrence Quantification Analysis (RQA) • To extend the original concept and made it more quantitative Zbilut and Webber (1992) developed a methodology called Recurrence Quantification Analysis. They defined several variables to quantify recurrence plots: • %recurrence: percentage of colored pixels in the RP. Quantifies the amount of cyclic behaviour. • %determinism: Percentage of recurrent points which form lines parallel • to the main diagonal. In the case of a deterministic system, these parallel lines • are an indication of the trajectories being close in phase space for time scales • that are equal to the length of these lines. • %laminarity: measures the percentage of vertical lines which indicate the occurrence of laminar states i.e., periods of tranquility or slowly drifting dynamics. • entropy: Shanon entropy of line segments distributions. Quantifies the richness of deterministic structure. • trend: measure of the recurrence points away from the central diagonal. It is a measure of non stationarity. • trap time: The average length of all vertical lines, indicating an average time the system is “trapped" into a laminar state as defined above • 1/linemax: reciprocal of the longest diagonal line segment, related to largest positive local Lyapunov exponent (Trulla et al., 1996)

Recurrence Plots: Surrogate Temporally uncorrelated NOK/MWh t=15, dE=10, e=40 EUR/KMh t =13, dE =10, e=10

Use of RQA for measuring volatility in electricity spot prices 720 point window (one month), data are shifted 720 points NOK/MWh EUR/MWh Finland W Denmark Norway E Denmark Sweden Kontek