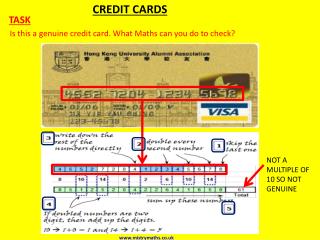

Credit Cards

Credit Cards. Day 1. UTION CAUTION CAUTIO. Credit cards have VERY HIGH interest rates. Avoiding Credit Card Trouble. Use only one credit card. It’s easy to lose track of your debt with more than one. If possible, pay off your balance each month in full.

Credit Cards

E N D

Presentation Transcript

Credit Cards Day 1

UTION CAUTION CAUTIO • Credit cards have VERY HIGH interest rates.

Avoiding Credit Card Trouble Use only one credit card. It’s easy to lose track of your debt with more than one. If possible, pay off your balance each month in full Compare APR and annual fees before you sign up for a credit card. WEBSITE

Avoiding Credit Card Trouble Watch out for “teaser rates.” Low for a bit of time and then very high. Never use credit cards for cash advances, there are higher rates. If you are in a deepening financial hole, consult a financial advisor. www. nfcc.org – National Foundation for Credit Counseling

Loan Payment Formula • PMT = Regular Monthly Payment • P = Starting Loan Principal • APR = annual percentage rate • n = number of payment period per year • Y = Loan term in years

Example 1: • You have a credit card balance of $2300 with an annual interest rate of 21%. You decide to pay off your balance over 1 year. How much will you need to pay each month? Assume you make no further credit card purchases. • Loan Payment Formula

Example 2: • Paul has gotten into credit card trouble. He has a balance of $9500 and just lost his job. His credit card company charges interest of APR = 21%, compounded daily. Suppose the credit card company allows him to suspend his payments until he finds a new job- but continues to charge interest. If it takes him a year to find a new job, how much will he owe when he starts his new job? • Compound Interest Formula

Example 3: • Stephanie lost her job and has had to live off her credit card for 3 months. She has $3,000 charged to her credit card with an APR of 19% compounded monthly. She just signed a 2 year contract with her new job. Since Stephanie knows she will have a job for 2 years. How much will she have to pay each month? • Loan Payment Formula

Example 4: • Todd bought $450 of school books on his credit card thinking he would be able to pay them off at the end of the month in full. But his car broke down right after he got paid and he had to use his money to fix the transmission. Todd’s monthly income varies, but he would like to have his credit card paid off in 3 months. (Assume an 18% APR compounded monthly) • Loan Payment Formula How much will his monthly payment need to be?

b) How much will he pay extra in interest? • c) He knew he would not be able to come up with • that much money each month. How much will his • monthly payments be if he pays off his credit card • in 4 months? 5 months? 6 months? • How much extra will he pay in interest on • each of the calculations above?

Exploration • John has been researching flat screen TVs for months. He located the TV he would like to purchase at Best Buy on sale. The TV is 15% off the original price of $450. He is 3 weeks from a pay check, but by that time the TV will not be on sale and he will have missed March Madness. Assume John has no other charges on his credit card and can make the monthly payment of $50. His card has an APR of 18% and compounds monthly. What should John do? Charge the TV to his credit card to get the sale price or wait to have the full $450? WEBSITE