29 th September 2006

230 likes | 415 Views

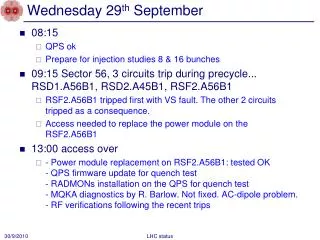

Today´s LNG plants:. Balancing the LNG supply chain, Commercial strategies and user approaches. 29 th September 2006. Index. Energy market evolution Europe: ensuring competitive, secure and sustainable NG The Spanish case Balancing the LNG supply chain Best Use of LNG terminals

29 th September 2006

E N D

Presentation Transcript

Today´s LNG plants: Balancing the LNG supply chain, Commercial strategies and user approaches 29th September 2006

Index • Energy market evolution • Europe: ensuring competitive, secure and sustainable NG • The Spanish case • Balancing the LNG supply chain • Best Use of LNG terminals • European regulation • Mediterranean supply: LNG Hub

Existing LNG Plants/Expansions Probable Greenfield Projects Possible Greenfield Projects Today´s LNG markets and LNG plants • Energy markets have tended towards regionalism and globalisation since 1973. This trend will consolidate. Atlantic Basin: An evolving market with a non-traditional structure S nøh vit Iran USA Alaska Russia Egypt Kenai Sakhalin Abu Dhabi Algeria Das Island Arzew , Skikda Libya Venezuela Brunei - Lumut Marsa - el - Brega Malaysia - Bintulu Trinidad Oman Yemen Atlantic Qatar Indonesia Bontang North Field Arun Indonesia Nigeria Tangguh Indonesia Bonny Angola Australia Gorgon Chile-Bolivia Australia- North West Shelf Pacific American Basin: A market for the 21st Century Pacific Basin: A traditional LNG market dominated by Japan and Korea

Europe: ensuring competitive, secure and sustainable natural gas Over the next 15 years Europe will have to import more than 80% of the gas needs New projects and infraestructures LNG will play increasing role Increasing need for seasonal storage

Europe: ensuring competitive, secure and sustainable natural gas The characteristics of the european gas market have to be integrated in the elaboration of an internal and external european policy: It is necessary to speak with one voice in a Global Energy Market The goal is a fully competitive integrated european market: • Cross barrier issues • Interoperability • Improving the regulatory process External Internal

Growing importance of LNG • Obvious parallelism between the natural gas market now, and the oil market in the eighties. • Market drivers: cutting of LNG costs???, raising of non-contracted capacity and liberalisation. LNG processing & transport costs LNG market evolution (2000-2010) Contracted capacity and over-capacity in LNG 40%

Comparing the evolution of LNG with oil markets 1950-72 1973-79 Early 1980s 1986-89 Early 1990s-today Administered markets Growth of spot trading Spot prices benchmark for all trades Oil derivatives grow Derivative markets mature – industry dis-integration and realignment • Comparing the evolution of the oil market with LNG shows that this type of evolution of the LNG market could occur • As the LNG market becomes fully arbitraged, efficient spot markets in LNG , shipping and regas capacity likely to emerge • Critical question is how and how long will market evolution take? Oil • Insignificant spot market – most trade on term contracts • Administered government and private corporation pricing • 19 producers (13 in OPEC) • Production, purchasing, and refining dominated by the “7 sisters” oil majors • Vertically integrated industry • Spot sales only 5% of total sales; many traders enter spot market • Rapid price escalation • Term contracts increasingly linked to prices of spot benchmarks • Nationalization of upstream operations breaks up vertical integration • Sellers’ market became buyers’ market • Additional non-OPEC production reduces preeminence of OPEC • Spot trading over 30% of total sales • 1983 – WTI futures listed on NYMEX • OTC derivatives illegal in U.S. until 1987 • Increased price volatility • 1986 crude price collapse • “Netback pricing” by Saudis • Forward and futures markets grow in importance • Oil majors reduce costs • 1987 – Chase completes first matched commodity swap • Intermediary trades dwarf underlying physical markets • Increased liquidity and derivatives competition • Major oil companies restructure activities – role of refining and marketing reviewed LNG • (1962-2002) • (2002-?) • (2002-?)

The Spanish case: main players Traders: BP GAS ESPAÑA, S.A. CEPSA GAS COMERCIALIZADORA,S.A. COMERCIALIZACIÓN DE ENERGÍA NATURAL, S.A. ELECTRABEL ESPAÑA, S.A. ENDESA ENERGÍA, S.A. ENI ESPAÑA COMERIALIZADORA DE GAS, S.A. GAS NATURAL COMERCIALIZADORA, S.A. GAS NATURAL SERVICIOS SDG, S.A. GAZ DE FRANCE COMERCIALIZADORA, S.A. IBERDROLA GAS, S.A. INCOGAS,S.A. NATURGAS COMERCIALIZADORA, S.A. REPSOL COMERCIALIZADORA DE GAS, S.A. RWE TRADING GMBH SHELL ESPAÑA, S.A. UNIÓN FENOSA COMERCIAL, S.L. UNIÓN FENOSA GAS COMERCIALIZADORA, S.A. Technical System Operator(TSO): Enagas, S.A. Transmission Operators: Enagas, S.A. BBG, S.L. REGANOSA Saggas, S.A. Gasoducto Al Andalus, S.A. Gasoducto de Extremadura, S.A. Sociedad de Gas Euskadi, S.A. Distributors

The Spanish case: Terminal costs and regulated tariffs How do users pay terminal services ? Regasification tollis calculated on a monthly basis using the formula set out below Pr =Tfr * Qr + Tvr * CrPr: monthly regasification toll charge.Qr: daily volume of flow of natural gas to be billed in kWh/day or its equivalent in LNG.Cr: kWh of natural gas regasified or supplied as LNG in tankers in the billing period.

The Spanish case: berthing slots • The agents must prepare scheduling for the gas they estimate to put in, take out, store, supply or consume in a given period. • Annual, monthly, weekly and daily scheduling shall be drawn up. • The “Network Code” sets out the minimum content of each of the schedules, the procedures and dates for their notification and the procedures for action to be taken if they are not fulfilled.

The Spanish case: SL-ATR process (TPA Logistic System) Booked Capacity Reserve of Capacity Daily ProvisionalBalance Nomination/renomination Viability answer Scheduling Re-Sharing Meassurement/asignation Definitive Balance TPA Billing

Balancing the LNG supply chain Regasification facilities are key part of the LNG chain • Tolling • Merchant plants Liquefaction Shipping Regasific. Trading Supply. Customer Transport by pipeline Distrib. Marketing.

Balancing the LNG supply chain: scheduling Tight programs Take or Pay Clauses Tank Topping Demurrages Upstream and Midstream LNG Terminal Multishipper model Nomination LNG stock

LNG terminals: efficient utilization Berthing services Slots management, vetting LNG Storage Quality, cost, maximum residence Regasification Peaking/baseload, sendout restrictions Other services Trucking loading, nitrogen blending

Best use of LNG terminals: multi shippers issues How should arrival windows be allocated ? Who pays for demurrages? How should terminal storage capacity be managed? Could the parties share tankers?

Best use of LNG terminals: unused capacity Use or lose it mechanism Interruptible capacity Secondary capacity mechanism Ex ship sales

Best use of LNG terminals: storage capacity Maximum storage allowed Failure to meet sendout commitments Sharing mechanisms Storage overrun charges

Best use of LNG terminals: new capacity Overcapacity vs bottleneck Not in my backyard syndrome Mandatory planning Economics

European regulation User´s view Level playingfield Regional approach balancing competition, efficiency and security of supply Standards

Mediterranean supply LNG HUB PIPEGAS HUB • LNG AS KEY SUPPLY IN SPAIN • LNG AS NEW SUPPLY IN NORTH EUROPE

Mediterranean supply: LNG Hub Due to the LNG important share in the supply matrix, Hub price would be strongly influenced by global LNG markets Supplier Hub Client Brent related Brent related Price ??? Henry Hub NBP Brent