Ethics

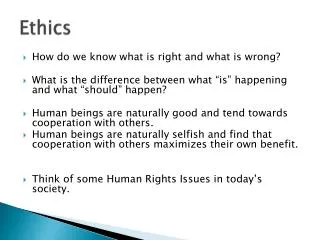

Ethics . Professional responsibility Making ethical and effective decisions. Key factors . Knowing the rules (applicable professional code of conduct) Following the rules (using decision-making framework). Standards . Circular 230 applies to all who practice before the IRS.

Ethics

E N D

Presentation Transcript

Ethics • Professional responsibility • Making ethical and effective decisions

Key factors • Knowing the rules (applicable professional code of conduct) • Following the rules (using decision-making framework)

Standards • Circular 230 applies to all who practice before the IRS. • State licensing authorities adopt rules of conduct. • Professions publish guidance. • Internal Revenue Code includes penalty provisions.

Circular 230 • Subpart A: Authority to Practice • Subpart B: Duties and Restrictions Relating to Practice before the IRS • Subpart C: Sanctions for Violations • Subpart D: Disciplinary Proceedings • Subpart E: General Provisions

Changes • Revisions effective 9/26/2007. • Prior rules still apply to returns filed before changes effective. • Some proposed changes were not finalized because of legislative changes.

Authority to practice • Attorney or CPA licensed and in good standing under state law • Actuary enrolled by Joint Board for the Enrollment of Actuaries • Individuals who have passed an examination or otherwise qualified as an enrolled agent or an enrolled retirement plan agent

Limited authority (must prove relationship) • Member of taxpayer’s immediate family • Employment relationship with taxpayer • Regular full-time employee of sole proprietor • General partner or regular full-time employee of partnership • Officer or regular full-time employee of corporation (includes affiliated corporations) • Regular full-time employee of trust, receivership, guardianship, or estate • Officer or regular employee of government unit

Limited authority for unenrolled return preparers • Anyone for representation outside the U.S. • An unenrolled preparer for representation before revenue agents, customer service representatives, or similar IRS employees during an examination of the return he or she prepared and signed as preparer. • An unenrolled preparer cannot represent taxpayers before appeals officers, revenue officers, or counsel.

Definition of practice • Preparing a tax return, replying to an information request, and appearing as a witness are not practice before the IRS. • Practice includes • Communicating with the IRS for a taxpayer regarding the taxpayer’s rights, privileges, or liabilities under federal tax laws • Representing a taxpayer at conferences, hearings, or meetings • Preparing and filing taxpayer documents

Third-party designee • Authorized on original return • Resolve return-processing issues • Valid for only 1 year from original due date of return • Includes amended return during same time period

Representation • Requires power of attorney • Representative must sign to accept authority • Recorded on IRS’s CAF (but keep a signed copy) • IRS generally copies representative on notices sent to taxpayer • IRS communication through POA required for collection issues

CPE requirements • Circular 230 requires attorneys, CPAs to maintain state license. • EAs and ERPAs must earn 16 hours of CPE, including 2 hours of ethics, each year; must earn 72 hours during a 3-year enrollment period. • Topics must enhance professional knowledge of federal tax-related matters, including taxation, accounting, tax preparation software, and ethics.

Supplying records • Promptly submit requested records to the IRS unless there is good-faith belief (on reasonable grounds) that the information is privileged. • Regions Financial Corporation v. United States.

Due diligence/accuracy • Preparing, approving, and filing tax returns and other documents • Determining correctness of statements regarding any matter administered by the IRS • Verification is not required, but implications may not be ignored.

Allowable fees • Fee may not be unconscionable • Contingent fee allowed only in limited circumstances • See Notice 2008-43

Return of client records • Upon request, a practitioner must return to a client “any and all records of the client that are necessary for the client to comply with his or her Federal tax obligations.” • Copies of the records may be retained. • There is no requirement to supply the practitioner’s work product to the client if fees are unpaid.

Conflict of interest • Representation of one client will be directly adverse to another client. • Significant risk that representation will be materially limited by duties to • Another client • A former client • A third person • A personal interest

Dual representation • Reasonable belief that representation of one client will not adversely affect relationship with other client • Potential positive and negative factors fully disclosed to both clients • Both clients consent in writing (waiver)

Potential conflicts • Divorced or separated spouses • Entity and owners • New client and former client • Practitioner’s own interest

Absolute prohibitions • Endorsing or otherwise negotiating any check issued to a client by the government in respect of a federal tax liability • Practice of law by individuals who are members of the bar

Best practices • Communicate clearly with the client regarding the terms of the engagement. • Establish facts, determine relevance, evaluate reasonableness, relate applicable law, and reach conclusion supported by law and facts. • Advise the client about import. • Act fairly and with integrity.

Submissions to IRS A practitioner may not advise a client to: • Take a frivolous position • Submit anything that contains or omits information with intentional disregard of a rule or regulation, unless it includes a good-faith challenge to the rule or regulation • Submit anything to delay or impede administration of federal tax law

Reliance on client • A practitioner generally may rely on information furnished by a client, without independent verification. • However, a practitioner must make reasonable inquiries if that information appears to be incorrect, inconsistent, or incomplete.

Sanctions Incompetence or disreputable conduct: • Tax crimes • Breach of trust conviction • Some other felonies • Deceiving Treasury or tribunal • Deceiving clients

Sanctions • Willful failure to file • Counseling tax evasion • Misappropriating client’s payment • Bribery or threats to IRS employee • Disbarment or suspension • Abetting ineligible practitioner

Sanctions • Contemptuous conduct • Giving a false opinion knowingly, recklessly, or through gross incompetence • Willfully failing to sign a tax return • Willful unauthorized disclosure or use of tax return information

Penalties 2007 changes to I.R.C. §§ 6694, 6695 • Penalties extended to all tax return preparers (not just income tax return preparers) • Level of authority needed to avoid penalty for preparing tax return that understates liability was heightened • Penalty amounts increased substantially

2008 Extenders Act • Preparer standard for taking an undisclosed position on a tax return is back to “reasonable basis” • “More likely than not” standard retained for listed and reportable transactions

Notice 2008-12 • A paid preparer must sign a return or refund claim after it is completed and before it is presented to the taxpayer for signature. • Notice 2008-12 (summarized on p. 610) lists returns and claims that paid preparers must sign to avoid an I.R.C. § 6695 penalty.

Notice 2008-13 Notice 2008-13 covers: • Types of returns and refund claims subject to preparer penalties • Definition of tax return preparer • Date return is considered prepared • Reasonable belief, reasonable basis, reasonable cause, and good faith

REG-129243-07 • “The Treasury Department and the IRS recognize that the majority of tax return preparers serve the interests of their clients and the tax system by preparing complete and accurate returns.” • “Tax return preparers are critical to ensuring compliance with the federal tax laws.”

Who is preparer? • Signing preparer—the person with primary responsibility for a return’s overall substantive accuracy • Non-signing preparer—a person other than the signing preparer whose advice is directly relevant to the existence, character, or amount of an entry on a return or claim (with respect to events that had occurred at the time the advice was rendered).

Substantial portion • Facts and circumstances determine whether a schedule, entry, or other portion of a return or claim for refund is substantial. • A single tax entry may be substantial. • Consider the item’s size, complexity relative to the taxpayer’s gross income. • Compare the resulting understatement to the total tax liability.

Penalty standard A preparer penalty for an understatement of tax due to an unreasonable position may be imposed if 3 conditions exist: • Preparer knew of the position. • Preparer did not disclose the position. • Preparer did not reasonably believe that the position would more likely than not be sustained on its merits.

2008 Extenders Act • Preparer standard for taking an undisclosed position on a tax return is back to “reasonable basis” • “More likely than not” standard retained for listed and reportable transactions

More-likely-than-not standard for tax position • Analyze facts and authorities and conclude in good faith that the position has a greater-than-50% likelihood of being sustained on its merits. • Use well-reasoned construction of statute if it is the only authority. • Authorities: Code, regulations, cases, rulings, legislative history

Confidence levels • Frivolous • Merely arguable • Reasonable basis (no penalty imposed if position is disclosed) • Realistic possibility of success • Substantial authority (no penalty for taxpayer even if position not disclosed) • More likely than not to succeed

Penalty avoidance • File return that includes required disclosure • If authority is not substantial, give client return that includes disclosure • If authority is substantial, explain different penalty standards to client • If tax shelter, advise client of potential penalty even with disclosure (document)

Firm’s liability • IRS looks at positions when imposing preparer penalties. • Only one person in a firm is primarily responsible for a position (and thus subject to the penalty for that portion of the tax). • An additional penalty may be imposed on a firm if its review procedures were disregarded through willfulness, recklessness, or gross indifference.

Normal practice • Penalty relief provisions take into account whether a preparer’s normal office practice, considered with other facts/circumstances, indicates that the error would rarely occur.

Certified financial planner (CFP) principles • Integrity • Objectivity • Competence • Fairness and reasonableness • Confidentiality • Professionalism • Diligence

CFP rules of conduct Groups of responsibilities: • Relationships with clients • Disclosures to clients • Client information and property • Obligations to clients • Obligations to employers • Obligations to CFP Board

Joe Paterno • Success without honor is an unseasoned dish; it will satisfy your hunger, but it won't taste good.

Making ethical decisions • Taking choices seriously • 7-step decision-making process • 6 Pillars of Character SM • Rationalizing a wrong act • Ethical decision-making • Being the person you want to be

Core principles • We all have the power to decide what we do and what we say. • We are morally responsible for the consequences of our choices.

Recognizing important decisions • Could the decision hurt your reputation, undermine your credibility, or damage important relationships? • Could the decision impede the achievement of any important goal?

Ethical and effective • A decision is ethical when it is consistent with core ethical values. • A decision is effective if it accomplishes something we want to happen or if it advances our purposes.

Critical aspects • Good decisions require discernment: knowledge and judgment. • Good decisions require discipline: the strength of character to do what should be done even when it is costly or uncomfortable.

7 steps 1. Stop and think. 2. Clarify your goals. 3. Determine the facts. 4. Develop options. 5. Consider the consequences. 6. Choose. 7. Monitor and modify.

6 Pillars of CharacterSM • Trustworthiness: Think “true blue” • Respect: Think of the Golden Rule • Responsibility: Think of being solid and reliable like an oak • Fairness: Think of dividing an orange to share fairly with friends • Caring: Think of a heart • Citizenship: Think of regal purple as representing the state