Cima F2 Study Material

Advanced Financial Reporting Cima F2 is one of the most popular exam in Cima.<br>You can easily pass the exam by the help of exams4sure.<br>We provides you the best dumps and test engine that help you in your exams days.<br>Our dumps and T.E is a proof that we are a reliable and trusted site. For more information visit us:<br>http://www.exams4sure.com/CIMA/F2-practice-exam-dumps.html<br>

Cima F2 Study Material

E N D

Presentation Transcript

Cima F2 Financial Management F2 extends the scope of the F1 Financial Management exam. It looks at advanced topics in financial accounting - the preparation of full consolidated financial statements and complex issues of principle in accounting standards. Pass Cima F2 Exam By The Help Of.

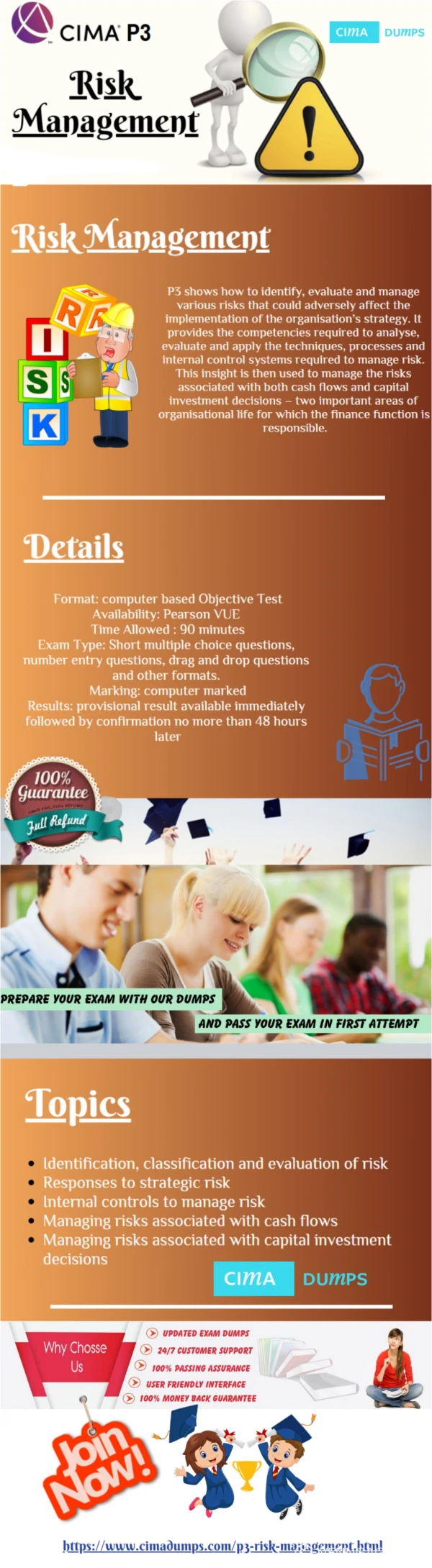

How CIMA benefit your business • Analysis - Understanding the history behind numbers and use it to make business decisions • Strategy – Using the insight from analysis to help formulate business strategy to create wealth and shareholder value. • Risk - The application of analytical skills to observe business processes end end a pair identify and manage risks. • Planning – using accounting techniques to plan and budget. • Communication – knowing what information management needs and explaining the numbers to non-financial managers. Pass Cima F2 Advanced Financial Reporting Exam By The Help Of Exams4Sure Get Complete File From http://www.exams4sure.com/CIMA/F2-practice-exam-dumps.html

Pass exam by the help of Pass Cima F2 Advanced Financial Reporting Exam By The Help Of Exams4Sure Get Complete File From http://www.exams4sure.com/CIMA/F2-practice-exam-dumps.html

The Sign Of Success CIMA F2 Financial Management Questions & Answers Pass Cima F2 Advanced Financial Reporting Exam By The Help Of Exams4Sure Get Complete File From http://www.exams4sure.com/CIMA/F2-practice-exam-dumps.html

Why Choose Us • Quality and Value • 100% Guarantee to Pass Exam • Answers Verified by Experts • Based on Real Exam Scenarios • 3500+ Exams Dumps • 24/7 Customer Support on Mail and Live Chat • 100% Lowest Price Guarantee Pass Cima F2 Advanced Financial Reporting Exam By The Help Of Exams4Sure Get Complete File From http://www.exams4sure.com/CIMA/F2-practice-exam-dumps.html

Question No 1: When can WACC be used as a discount rate? The WACC is often used as a discount rate when using net present value or internal rate of return calculations. However, this is only appropriate if the following conditions are met: (1) The capital structure is constant. If the capital structure changes, the weightings in the WACC will also change. (2) The new investment does not carry a different business risk profile to the existing entity's operations. (3) The new investment is marginal to the entity. If we are only looking at a small investment then we would not expect any of ke, kd or the WACC to change materially. If the investment is substantial it will usually cause these values to change.

Question No 2: Formula - given in the assessment WACC? k0=ke(Ve/(Ve+Vd))+kd(Vd(Ve+Vd))

Question No 3: Procedure for calculating the WACC? Step 1 Calculate weights for each source of capital. Step 2 Estimate the cost of each source of capital. Step 3 Multiply the proportion of the total of each source of capital by the cost of that source of capital. Step 4 Sum the results of step 3 to give the weighted average cost of capital.

Question No 4: Weighted Average Cost of Capital (WACC)? The weighted average cost of capital (WACC) is the average cost of the entity's finance (equity, bonds, bank loans, and preference shares) weighted according to the proportion each element bears to the total pool of funds.

Question No 5: kd for redeemable bonds? The kd for redeemable bonds is given by the IRR of the relevant cash flows. The relevant cash flows would be (assuming that there is no one year delay in the tax saving): Year Cash flow 0 Market value of the bond (or nominal value if being issued or is trading at par) (P0) 1 to n Annual interest payments net of tax i(1 - T) n Redemption value of the bond RV There are four steps to ensuring an accurate computation: (1) Identify the cash flows. Note that the interest payments should be included net of tax when calculating the cost of debt for bonds from the viewpoint of the issuer, whereas tax is not deducted when calculating the return to the investor. (2) Estimate the IRR. (3) Calculate two NPVs (preferably one -ve and one +ve). (4) Calculate the IRR.

Question No 6: Kd for bank borrowings? The cost of debt for bank borrowings is simply kd = r (1 - T) where: r = annual interest rate in percentage terms T = corporate tax rate

Question No 7: The cost of debt - kd Features? (1) Debt is tax deductible and hence interest payments are made net of tax. (2) Debt is always quoted in $100 nominal units or blocks. (3) Interest paid on the debt is stated as a percentage of nominal value. This is known as the coupon rate. It is not the same as the cost of debt. The amount of interest payable on the debt is fixed. The interest is calculated as the coupon rate multiplied by the nominal value of the debt. (4) Debt is normally redeemable at par (nominal value) or at a premium or discount. (5) Interest can be either fixed or floating (variable) on borrowings, but bonds normally pay fixed rate interest.

Question No 8: The cost of debt - kd? The cost of debt is the rate of return that debt providers require on the funds that they provide. The value of debt is assumed to be the present value of its future cash flows.

Question No 9: The dividend valuation model with constant growth? ke =(d1/P0)+g or ke =(d0(1+g)/P0)+g where g = a constant rate of growth in dividends d1 = dividend to be paid in one year's time d0 = current dividend

Question No 10: Cum div and ex div share prices? The ex dividend ('ex div') value of a share is the value just after a dividend has been paid. Occasionally in questions, you may be given a share price just before the payment of a dividend (a 'cum div' price). In this case, the value of the upcoming dividend should be deducted from the cum div price to give the ex div price. For example, if a dividend of 20 cents is due to be paid on a share which has a cum div value of $3.45, the ex div share price to be entered into the DVM formula is $3.45 - $0.20 = $3.25.

Get your money back if you fail in exam • 100% Exam Passing Guarantee With Money Back Assurance To Get Complete File Click Here