Download

1 / 11

110 likes | 264 Views

Retirement Compensation Arrangement (RCA). What is an RCA?. Retirement Compensation Arrangements were developed by the Department of Finance for organizations and companies that wanted to provide basic or enhanced retirement benefits to Key Employees.

E N D

What is an RCA? Retirement Compensation Arrangements were developed by the Department of Finance for organizations and companies that wanted to provide basic or enhanced retirement benefits to Key Employees. Corporations will provide funding or other promises to a trust set up to hold the assets of the RCA for the benefit of the Key Employee.

An RCA usually includes a written agreement outlining the obligations of the company to fund the agreement. As well there may be a written agreement between the company and the Key Employee stipulating certain obligations of the employee to the company. At the retirement of the Key Employee the RCA Trust will be obligated to provide a Pension Income to the Key Employee from the trust assets. Trust Beneficiaries would be the employee, while living, and the spouse and/or children of the employee for benefits due after death. The company may also be a beneficiary in order to recover unused benefits.

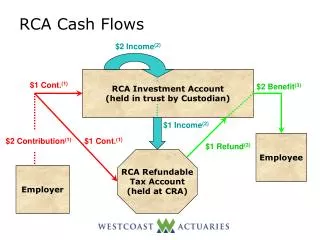

How does an RCA Work? 1. The Corporation makes deposits to the RCA for a specified period of time. 2. A Refundable Tax is payable on all deposits to the RCA at a rate of 50% of the deposit. 3. Any income earned by the RCA is also subject to the 50% Refundable Tax. 4. When the RCA pays out Pension income to the Trust Beneficiaries, it applies for a Tax Refund from the Refundable Tax Account. The refund is 50% of the Pension income paid. 5. Withdrawals from the RCA assets plus Refunds from the Refundable Tax Account constitute the Pension income to the Beneficiaries.

Types of RCA's 1.Non Funded RCA's: The corporation may decide not to fund the RCA but rather simply make a promise to pay in the future. Since no deposits are made and no income can be earned, no refundable tax is payable. All pension payments paid to the retired employee may be deductible to the corporation as a retirement benefit. However, all income from the RCA to the Beneficiaries is dependant on the company being solvent, willing and able to provide the future income from corporate cash flow.

2. RCA's with Letters of Credit (LOC): To provide a level of protection to the beneficiaries of the trust the company may establish a letter of credit with a bank to guarantee the future income to the beneficiaries should the company be unable to do so. In this case, any fee for the letter of credit is subject to refundable tax. The total RCA deposit would be deemed to be equal to twice the fee payable for the letter of credit and 50% of this will be payable as Refundable Tax.

3. Managed Funds RCA: The corporation may decide to fund the RCA by making deposits to a fund which invests in a variety of income earning vehicles. All deposits and income will be subject to 50% refundable tax.Under the regulations for RCA's there is no special treatment for dividends or capital gains. 100% of the income to the RCA is subject to refundable tax without reference to capital gains inclusion rates or dividend tax credits.

4. Insured RCA: With an insured RCA the corporation takes advantage of the tax sheltering provided by a Special Life Insured Program. Deposits are made to the Special Life Insured Program owned by the trust and any income earned within the plan is not subject to taxation until withdrawals are made or the program is collapsed. In this situation the Life Insurance Death Benefit and the Life Insurance Cash Values are part of the RCA and are subject to personal tax in the hands of the beneficiaries when paid out to them.

5. Split Dollar Insured RCA: While wishing to use the tax sheltering benefits of a Special Life Insured Program in an RCA, the corporation may have a need for Key Person or Buy Sell Life Insurance on it's own. In this case the Insurance Program can be separated and the two components of the plan, the Death Benefit and the Cash Equity can be owned in different places.

Usually the corporation will own and pay for the Death Benefit part of the Life Plan while the RCA will own and pay for the Cash Equity part of the Life Plan. In this case the RCA benefits from the tax shelter in the Life plan and the company obtains a tax free death benefit on the death of the Key Person. If the company is a privately held company a tax free Capital Dividend Account credit may result allowing dividends to be paid to shareholders free of tax .

Questions or Comments? Please feel free to contact us at : info@insuranceconcepts.ca Thank You