Download

1 / 60

690 likes | 1.27k Views

Output and the Exchange Rate in the Short Run. Chapter 17 Krugman and Obstfeld 9e ECO41 International Economics Udayan Roy. Long Run and Short Run. Long run theories are useful when all prices of inputs and outputs have enough time to adjust fully to changes in supply and demand.

E N D

Output and the Exchange Rate in the Short Run Chapter 17 Krugman and Obstfeld 9e ECO41 International Economics Udayan Roy

Long Run and Short Run • Long run theories are useful when all prices of inputs and outputs have enough time to adjust fully to changes in supply and demand. • In the short run, some prices of inputs and outputs may not have time to adjust, due to labor contracts, costs of adjustment, or imperfect information about market demand. • This chapter discusses a theory of the short run behavior of a “small” economy with flexible exchange rates under perfect capital mobility

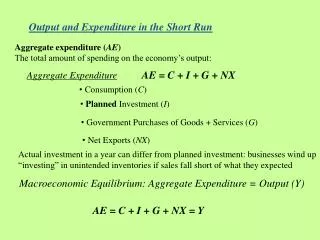

Determinants of Aggregate Demand • Aggregate demand (D) is the aggregate amount of goods and services that people are willing to buy. It consists of the following types of expenditure: • consumption expenditure (C) • investment expenditure (I) • government purchases (G) • net expenditure by foreigners: the current account (CA)

Determinants of Aggregate Demand • Assumption: Consumption expenditure (C) increases when disposable income (Y − T)—which is income (Y) minus taxes (T)—increases • … but by less than the increase in disposable income • Real interest rates may influence the amount of saving and consumption, but we assume that they are relatively unimportant here. • Wealth may also influence consumption, but we assume that it is relatively unimportant here.

Determinants of Aggregate Demand • Assumption: The balance on the current account (CA) increases … • … when the real exchange rate (q) increases • Recall that the real exchange rate is the price of foreign products relative to the price of domestic products: q = EP*/P • … when disposable income decreases • more disposable income (Y-T) means more expenditure on foreign products (imports). Therefore, when Y−T rises, CA falls.

Current account depends on the real exchange rate and disposable income. Consumption depends on disposable income Investment and government purchases, both exogenous Determinants of Aggregate Demand (cont.) • Aggregate demand is therefore expressed as: D = C(Y – T) + I + G + CA(E×P*/P, Y – T) • Or more simply: D = D(E×P*/P, Y – T, I, G)

Aggregate demand as a function of the real exchange rate, disposable income, investment, government purchases Value of output, income from production Short Run Equilibrium for Aggregate Demand and Output

Goods Market Equilibrium: Shifts of the DD Curve Suppose the economy is initially at Point 1. Suppose there is a tax hike (T↑), but output is still at Y1. Then, C will decrease. Let’s say C decreases by $100. This will require CA to increase by $100. But T ↑, by itself, will increase CA by less than $100. DD2 Why? When C falls by $100, the consumption of imported goods would fall by less: say, by $55. So, the tax cut, by itself, would increase CA by only $55. 3 Therefore, to make CA increase by another $45, E must increase. So, the tax hike takes the economy from Point 1 to Point 3. In other words, the tax hike shifts the DD curve upward and to the left.

Goods Market Equilibrium: Shifts of the DD Curve Suppose the economy is initially at Point 2. Suppose I or G increases (I + G↑), but output is still at Y2. Then, CA must decrease. With unchanged Y, this requires a decrease in E. Therefore, if I or G increases and Y is unchanged, then the economy must move from Point 2 to Point 3. In other words, if I or G increases, the DD curve must shift downward or to the right. DD2 3

Goods Market Equilibrium: Shifts of the DD Curve Suppose the economy is initially at Point 2. Suppose P* increases or P decreases (P*/P ↑), but output is still at Y2. Then, CA must stay unchanged. With Y and T unchanged, the only way CA can remain unchanged in spite of P*/P ↑ is if E decreases enough to keep the real exchange rate unchanged. Therefore, if P* increases or P decreases and Y is unchanged, then the economy must move from Point 2 to Point 3. In other words, if P* increases or P decreases , the DD curve must shift downward or to the right. DD2 3

Fig. 17-2: The Determination of Output in the Short Run Output is greater than aggregate demand: firms decrease output Aggregate demand is greater than production: firms increase output

Short Run Equilibrium and the Exchange Rate: DD Schedule • How does the value of the foreign currency (E) affect the short run equilibrium of aggregate demand and output? • Domestic and foreign price levels (P and P*) are assumed fixed in the short run. • Therefore, a rise in the nominal exchange rate (E) makes foreign goods more expensive relative to domestic goods. That is, q = E× P*/P increases when E increases. • As a result, CA increases and, therefore, D increases. That is, D increases when E increases. See Fig 17-3. • In equilibrium, Y = D. Therefore, Y increases when E increases. • This gives the DD curve. See Fig 17-4. Y = D(E×P*/P, Y – T, I, G)

Fig. 17-3: Output Effect of a Currency Depreciation with Fixed Output Prices Y = D(E×P*/P, Y – T, I, G)

Fig. 17-4: Deriving the DD Schedule Y = D(E×P*/P, Y – T, I, G)

Shifting the DD Curve • Changes in the exchange rate cause movements along a DD curve. Other changes may cause it to shift: • Changes in G: more government purchases cause higher aggregate demand and output in equilibrium. Output increases for every exchange rate: the DD curve shifts right.

Fig. 17-5: Government Demand and the Position of the DD Schedule An increase in G causes the DD curve to shift to the right. • The same rightward shift of the DD curve happens if: • I increases • T decreases • P*/P increases Y = D(E×P*/P, Y – T, I, G)

Shifting the DD Curve • The DD curve shifts right if: • G increases • T decreases • I increases • P decreases • P* increases • C increases for some unknown reason • CA increases for some unknown reason Y = D(E×P*/P, Y – T, I, G)

Short Run Equilibrium for Assets • We consider two asset markets when considering asset market equilibrium: • Ch 14: Foreign exchange market • interest parity: R = R* + (Ee – E)/E • Ch 15: Money market • real money supply and demand determine equilibrium: Ms/P = L(R, Y)

What makes the value of the euro (E) change? Note the inverse relation between Y and E. This yields another curve linking Y and E: the AA curve. M/P (-) (+) R Y (-) Domestic preference for cash (+) E (+) (-) M*/P* R* (+) Y* (+) Ee (+) Foreign preference for cash

Recap: What makes (E), the value of the foreign currency, change? Note the inverse relation between Y and E. This yields another curve linking Y and E: the AA curve. M/P (-) (+) R Y But E is also affected by changes in M/P, Ee, and L, the preference for cash. (-) Domestic preference for cash (+) E (+) (-) M*/P* R* (+) Y* (+) Ee (+) Foreign preference for cash

Shifting the AA Curve • The AA curve shifts right if: • Ms increases • P decreases • Ee rises • R* rises • L decreases for some unknown reason E E0 E1 Y Y0 Y1

Putting the Pieces Together: the DD and AA Curves • A short run equilibrium means that the exchange rate (E) and output (Y) are such that there is equilibrium in: • the output market: aggregate demand (D) equals aggregate output (Y). • the foreign exchange market: interest parity holds. • the money market: real money supply (MS/P) equals real money demand (L). Y = D(E×P*/P, Y – T, I, G)

Fig. 17-8: Short-Run Equilibrium: The Intersection of DD and AA The short run equilibrium occurs at the intersection of the DD and AA curves The output market is in equilibrium on the DD curve The assetmarkets are in equilibrium on the AA curve

Shifting the AA and DD Curves • The AA curve shifts right if: • Ms increases • P decreases • Ee rises • R* rises • L decreases for some unknown reason • The DD curve shifts right if: • G increases • T decreases • I increases • P decreases • P* increases • C increases for some unknown reason • CA increases for some unknown reason Knowing how some specified change shifts the DD and AA curves will help us predict the consequences of the specified change.

Temporary Changes in Monetary and Fiscal Policy • Monetary policy: policy in which the central bank influences the money supply (MS). • Monetary policy primarily influences asset markets. • Fiscal policy: policy in which governments influence the amount of government purchases (G) and taxes (T). • Fiscal policy primarily influences aggregate demand (D). • Temporary policy changes are expected to be reversed in the near future and thus do not affect expectations about exchange rates in the long run. • Specifically, temporary changes in MS, G, and T do not affect Ee.

Shifting the AA and DD Curves • The AA curve shifts right if: • Ms increases • P decreases • Ee rises • R* rises • L decreases for some unknown reason • The DD curve shifts right if: • G increases • T decreases • I increases • P decreases • P* increases • C increases for some unknown reason • CA increases for some unknown reason

Temporary Changes in Monetary Policy • When there is an increase in the supply of money • The AA shifts up (right). • Both E and Y increase • R decreases • As Ee is unaffected when the change in Ms is temporary, the increase in E leads to a decrease in R; recall R = R* + (Ee – E)/E. E DD E0 Y Y0

Fig. 17-10: Effects of a Temporary Increase in the Money Supply R*↑ and Ee ↑ have the same effect, as does a fall in money demand (L).

Effect of Temporary MS↑ on CA • Goods market equilibrium (DD curve): Y = C(Y – T) + I + G + CA. • An increase in Ms causes Y to increase. • But C(Y – T) increases less than Y does. • Therefore, CA must increase. • That is, an increase in the supply of money, leads to an increase in the current account balance (or, net exports)

Changes in Ee and R* • Any increase in Ee, the expected future value of the foreign currency, or in R*, the foreign interest rate cause the same shifts as expansionary monetary policy: they shift the AA curve rightward and do not affect the DD curve • Therefore, Y↑ and E↑. • As P and P*, being exogenous, are unaffected, E↑ implies q↑

Temporary Changes in Fiscal Policy • An increase in government purchases or a decrease in taxes increases aggregate demand and output. • The DD curve shifts right. • Higher output increases real money demand, and • thereby increases interest rates, • causing an increase in the value of the domestic currency (a fall in E).

Shifting the AA and DD Curves • The AA curve shifts right if: • Ms increases • P decreases • Ee rises • R* rises • L decreases for some unknown reason • The DD curve shifts right if: • G increases • T decreases • I increases • P decreases • P* increases • C increases for some unknown reason • CA increases for some unknown reason

Fig. 17-11: Effects of a Temporary Fiscal Expansion G↑ and/or T ↓ P*↑and I↑ have the same effect, as do shocks that increase C and CA. E↓ implies R↑ because R = R* + Ee/E - 1.

Effect of G↑ and/or T↓ on CA • When G↑ and/or T↓ — this is called expansionary fiscal policy — E↓ and Y↑. • Therefore, CA↓. • Expansionary (contractionary) fiscal policy reduces (increases) net exports.

Fig. 17-12: Maintaining Full Employment After a Temporary Fall in World Demand for Domestic Products Temporary fall in world demand for domestic products reduces output below its normal level Temporary monetary expansion could depreciate the domestic currency Temporary fiscal policy could reverse the fall in aggregate demand and output

Fig. 17-13: Policies to Maintain Full Employment After a Money Demand Increase Temporary monetary policy could increase money supply to match money demand Increase in money demand raises interest rates and appreciates the domestic currency Temporary fiscal policy could increase aggregate demand and output

Effects of an increase in investment • Simply put, the effects of I↑ are exactly the same as those of G↑ • Therefore, we can predict that if G↑ and/or I↑, then E↓, q↓, Y↑, R↑, and CA↓.

Effects of a change in foreign prices • We saw three slides back that P*↑ causes the DD curve to shift right and has no effect on the AA curve • Therefore, E↓ and Y↑. • And, following the same steps as in our discussion of the effects of Ee↑ and R*↑, we can prove that CA↑