Download

1 / 12

120 likes | 237 Views

FOMC Statement: Statutory Dual Mandate: Maximum Employment (5.5% U.R.) (March projection) 2014 = 6.2% 2015 = 5.8% 2. Price Stability (2.0% PCE Inflation) (March projection) 2014 = 1.6% 2015 = 1.8%. Fed Actions to lower rates and stimulate economy:

E N D

FOMC Statement: • Statutory Dual Mandate: • Maximum Employment (5.5% U.R.) • (March projection) • 2014 = 6.2% • 2015 = 5.8% • 2. Price Stability (2.0% PCE Inflation) • (March projection) • 2014 = 1.6% • 2015 = 1.8%

Fed Actions to lower rates and stimulate economy: • 1. Purchase $25 billion/month agency MBS • Purchase $30 billion/month longer-term Treasury notes • Reinvest principal payments of agency debt and MBS • Roll over maturing Treasury securities • Keep fed funds rate at 0-0.25% until: • Labor market improves • 2-yr DP/P expectations > 2.5%

The New Monetary Policy Tools Conventional monetary policy has reached its limit - (0-0.25 federal funds rate) Broader use of Fed’s balance sheet to achieve objectives New policies are intended to influence financial conditions • Purchase longer-term Treasuries (lower long-term interest rates, term spreads). • Purchase private assets (agency MBS, consumer ABS): offset credit shock, lower credit spreads, increase credit availability • Working in conjunction with expansionary fiscal policy. • Monitor credit conditions to gauge success • But no explicit targets Quantitative easing of a different sort • Policies will inject large amounts of reserves • But goal is not the level of reserves No single measure to summarize Fed actions • Watch the H.4.1 • Makes communications challenging • Policy commitment language Governance issues • All decisions made by FOMC • Even though 13(3) programs under authority of Board

Monetary policy options to prevent deflation and increase inflation expectations • Quantitative easing: print money to buy long-term government debt • Buy private-sector debt • Change expectations by announcing it will keep short-term rates low • for a long time • 4. Raise its long-run inflation target • (encourage borrowing, discourage cash hoarding) • 5. Reduce the interest rate paid on excess reserves. • 6. Move from inflation targeting (rate of change) to price level targeting

Fed’s Exit Strategy From Accommodative Policies Inflationary Scenario: Economic recovery => banks find profitable lending opportunities => reserves => credit => money supply => aggregate demand => inflation Countervailing Policy Measures/Tools That Tighten Monetary Policy • Improving private credit conditions => decrease use of Fed’s short-term lending facilities. • Maturing Fed-held securities will reduce reserves. • Raise interest rate paid on bank reserves – currently 0.25% - held at Fed to reduce incentive of banks to lend out reserves. This reserve/deposit interest rate effectively places a floor under short-term market interest rates. Four options to reduce bank reserves, raise short-term interest rates and limit credit/money growth: • Arrange large-scale reverse repurchase agreements, RRPs, with financial market participants. RRPs involve the sale by the Fed of securities from its portfolio with an agreement to buy the securities back at a slightly higher price at a later date. • Treasury could sell bills and deposit the proceeds with the Federal Reserve (Supplementary Financing Program). • Offer term deposits (CDs) to banks so reserves would not be available for federal funds market. • Sell long-term securities into the open market.

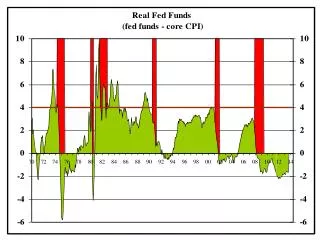

Taylor Rule, NAIRU and the Phillips Curve Taylor Rule Fed funds rate target = inflation rate + equilibrium real fed funds rate + 1/2 (inflation gap) + 1/2 (output gap) Phillips Curve Theory • Change in inflation influenced by output relative to potential output, and other factors • Potential GDP is a function of the natural rate of unemployment • Natural rate of unemployment - the rate of unemployment where there is no tendency for inflation to change • NAIRU thought to be 5% • Output gap is an indicator of future inflation if unemployment rate < NAIRU => GDP growth > potential GDP =>inflation if unemployment rate > NAIRU => GDP growth < potential GDP =>inflation

Vicious Cycles of the Mortgage Crisis Falling Home Prices Increased Supply of Homes Not self correcting Negative Equity (Home worth less than mortgage) Homeowners “Walk Away” or Involuntary Foreclosures Increase Economic Activity Slows & Unemployment Increases Mortgage Payments Decline Monetary Policy Intervention • Lower fed funds interest rate • New lending facilities • Self-reinforcing spiral • Feedback Loop • Multiplier Effect • Sum of an Infinite Geometric Series Value of MBS Declines Banks Restrict Lending Bank Capital (Loanable Funds) Declines Banks Incur Losses

Chapter 16: Goals of Monetary Policy 1. High Employment Employment Act of 1946, Humphrey–Hawkins Act 1978 “high employment consistent with stable prices”. Full employment (natural rate of unemployment) frictional/structural = 5% • Economic Growth r => I => (Y/L) => DY/Y • Price Stability(Most important goal) StableDP/P => clear price-signal effect => I uncertainty => DY/Y • Interest Rate Stability r stability => I uncertainty => I => DY/Y • Financial Market Stability stability => financial intermediation => efficiency of capital => DY/Y • Foreign Exchange Market Stability (e/$) => U.S. exports less competitive => X => GDP (e/$) => U.S. exports more competitive => X => pricing power => DP/P Goals often in conflict Y => U.R. => wages => DP/P => i => OMP => MB => M1 => DP/P

Econ 330 Chapter 16 HomeworkDue Thursday, April 3 (hand in prior to exam) Chapter 16 Questions & Applied Problems 3, 7, 13, 22, 23, 25