Download

1 / 10

100 likes | 217 Views

This discussion explores whether current stock prices are a result of irrational behavior or grounded in fundamentals. By examining historical returns, expected dividends, and price-to-earnings ratios, we analyze how market valuations relate to future growth rates and returns. Notably, the disparity between actual P/E ratios and historical averages raises questions on market overvaluation. Key implications for consumption, savings, and investment are considered, along with potential consequences of declining stock returns. Investors may need to reassess strategies in light of market realities.

E N D

Are Stock Prices Driven by Irrational Exuberance? • A. Caveats: I speak for myself. • B. Purpose: To provide one explanation for the Chairman’s comments on the market’s value.

C. Historical Perspective • 1. Average real annual returns = 7.6%. • 2. Average real bond returns = 2.0%. • 3. 30% annual fluctuations in stock prices are not uncommon. • 4. Stock returns may be poor for long periods. • a) The market lost 50% of its value in 1972-1973. • b) Bonds outperformed stocks from 1967-1982.

D. What Determines the Price Of Stocks? • 1. Expected dividends and prices in the future. • 2. The definition of return is • a) Assume constant dividend growth. (We don’t need this.) • b) Assume constant stock returns. (We don’t need this.) • c) Assume that the present value of a stock very far in the future is very small. Then:

D. What Determines the Price Of Stocks? • 4. Higher prices today are associated with a higher growth rate of dividends or lower stock returns in the future. • 5. This requires no economic theory. It comes from the definition of return.

E. Do historical levels of dividend growth & stock returns justify current prices? • (Let’s use earnings instead of dividends.) • 1. Historical average dividend growth and stock returns imply a P/E ratio of 17.4. • 2. The August 1997 P/E ratio was 23.25; the market is 34% overvalued.

F. What levels of dividend growth or stock returns justify the current P/E ratio of 23? • 1. Dividend growth could rise from 1.75% to 3.2%. • 2. Stock returns could fall from 7.6% to 6.2%.

G. How big are these changes in dividend growth and returns? • 1. Dividends would double every 22 years instead of every 40 year. • Is this realistic? • 2. Wealth would be 50% higher after 30 years with the higher stock returns. • This affects consumption, savings and investment.

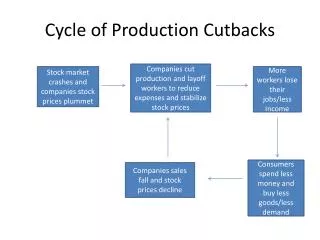

H. What are the consequences of the decline in stock returns to 6.2%? • 1. People become much less wealthy, consumption declines significantly. • 2. Savings for college or retirement have to go way up. • 3. Firms will invest much less. • 4. A stock market crash may interfere with the Federal Reserve’s pursuit of price stability and a pro-growth environment. • I. What can or should be done about it? • 1. Not clear. Investors may bear some or most of the consequences of their own mistakes.