Download

1 / 15

190 likes | 427 Views

Standard Costs and Variance Analysis. Chapter Ten & Eleven. Standard Costs. Standards are benchmarks or “norms” for measuring performance. Two types of standards are commonly used. Quantity standards specify how much of an input should be used to make a product or provide a service.

E N D

Standard Costs andVariance Analysis Chapter Ten & Eleven

Standard Costs Standards are benchmarks or “norms”for measuring performance. Two typesof standards are commonly used. Quantity standardsspecify how much of aninput should be used tomake a product orprovide a service. Cost (price)standards specify how much should be paid for each unitof the input.

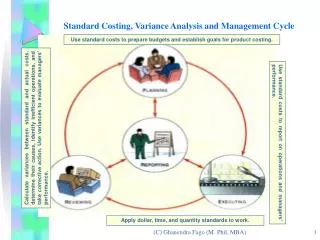

Exh. 10-1 Takecorrective actions Identifyquestions Receive explanations Conduct next period’s operations Analyze variances Variance Analysis Cycle Prepare standard cost performance report Begin

Standard Cost Card – Variable Production Cost A standard cost card for one unit of product might look like this:

Price Variance Quantity Variance Difference betweenactual price and standard price Difference betweenactual quantity andstandard quantity A General Model for Variance Analysis Variance Analysis

Actual Quantity Actual Quantity Standard Quantity × × × Actual Price Standard Price Standard Price Price Variance Quantity Variance A General Model for Variance Analysis (AQ × AP) – (AQ × SP) (AQ × SP) – (SQ × SP) AQ = Actual Quantity SP = Standard Price AP = Actual Price SQ = Standard Quantity

Fixed Overhead Variances Actual Fixed Fixed Fixed Overhead Overhead Overhead Incurred Budget Applied DH × FR SH × FR Budget Variance VolumeVariance FR = Standard Fixed Overhead RateSH = Standard Hours AllowedDH = Denominator Hours

Mix of skill levelsassigned to work tasks. Level of employee motivation. Quality of production supervision. Production Manager Quality of training provided to employees. Responsibility for Labor Variances Production managers areusually held accountablefor labor variancesbecause they caninfluence the:

Variable Overhead Variances –A Closer Look Efficiency Variance Controlled bymanaging theoverhead cost driver.

Budget Variance Fixed Overhead Variances –A Closer Look Results from spendingmore or less thanexpected for fixedoverhead items.

VolumeVariance Results when standard hoursallowed for actual output differsfrom the denominator activity. Unfavorablewhen standard hours< denominator hours Favorablewhen standard hours> denominator hours Volume Variance – A Closer Look

Larger variances, in dollar amount or as a percentage of the standard, are investigated first. Variance Analysis andManagement by Exception How do I knowwhich variances to investigate?