Strategy and Master Budget

Strategy and Master Budget. Chapter 8 Objectives: Describe the role of budget in planning, controlling, and performance evaluation Discuss the importance of strategy and its role in budgeting and identify factors common to successful budgets Outline the budgeting process.

Strategy and Master Budget

E N D

Presentation Transcript

Strategy and Master Budget Chapter 8 Objectives: Describe the role of budget in planning, controlling, and performance evaluation Discuss the importance of strategy and its role in budgeting and identify factors common to successful budgets Outline the budgeting process

Role of Budget • A budget is an organization’s operation plan for a specified period • It identifies the resources and commitments required to fulfill the organization’s goals for the period. • Budget is… • a plan of operations. • a basis for allocating resources. • a communication and authorization device. • a device for motivating and guiding implementation. • a guideline for operations and gauge for controlling operations. • a basis for performance evaluation.

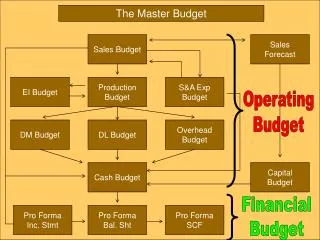

Long-Term Objectives Capital Budgeting Long-Range Plan Short-Run Objectives Feedback Master Budgets Controls Operations Budget Relationship Strategic Goals

Master Budget • A master budget is a comprehensive budget for a specific period • It consists of many interrelated operating and financial budgets • A sales budget often is regarded as the cornerstone of the entire budget • The starting point in preparing a sales budget is sales forecasts

Sales Budget • A sales budget shows expected sales in units at their expected selling prices • A firm prepares the sales budget for a period based on the forecasted sales level, production capacity for the budget period, and long-term plan and short-term goal of the firm • A sales budget is the cornerstone of budget preparation because a firm can complete the plan for other activities only after it identifies the expected sales level

Sale Forecast Sales Budget Kerry Industrial Products Company Sales Budget For the First Quarter Ended June 30, 2007 AprilMayJuneQuarter Sales in units 20,000 25,000 35,000 80,000 Selling price per unit x $30 x $30 x $30 x $30 Total sales $600,000 $750,000 $1,050,000 $2,400,000

Production Budget • A firm prepares a production budget after determining the number of units that it expects to sell • A production budget is a plan for acquiring the resources needed to carry out the manufacturing operations to satisfy the expected sales and maintain the desired ending inventory • The total number of units to be produced depends on the budgeted sales, the desired units of finished goods ending inventory, and the units of finished goods beginning inventory.

Determining the budgeted units of production: Budgeted Budgeted Desired Beginning Production Sales Ending Inventory (in units) (in units) Inventory (in units) (in units) = + – Production Budget Kerry expects to have 5,000 units on hand on April 1 and wants to have 30% of the following month’s projected unit sales on hand at the end of each month.

Production Budget 30% of June’s budgeted sales July sales are budgeted at 40,000 units,

Total direct Desired direct Total direct Direct materialsmaterials materials materials beginningneeded in ending inventory purchase for inventoryproduction the period + = + Direct Material Budget • The information in the production budget becomes the basis for preparing several manufacturing-related budgets • A direct materials usage budget shows the direct materials required for production and their budgeted cost

Direct Material Budget Each unit produced requires 3 pounds of alloy at a cost of $2.45 per pound. Kerry expects to manufacture 36,000 units in July. On April 1, 7,000 pounds of alloy were in inventory. Budgeted unit production in April is 22,500. At 3 pounds per unit direct material needs are 67,500 pounds. Desired ending inventory is 10 % of the next period’s production needs. In May production needs will be 28,000 units, so 28,000 × 3 pounds = 84,000 × 10% = 8,400 pounds. Determine the total cost of direct material purchase pf April. See Exhibit 8.8

Direct Labor Budget • To prepare the direct labor budget, a company would use its production budget • The direct labor budget enables the personnel department to plan for hiring and repositioning of employees • A good labor budget helps the firm to avoid emergency hiring, prevent labor shortages, and reduce or eliminate the need to lay off workers • Firms usually prepare labor budget for each type of labors. For example, for each skill requirement.

22,500 × .2 × $12.00 = $54,000 22,500 × .5 × $8.00 = $90,000 Direct Labor Budget Each unit of output requires .5 hours of semi-skilled labor at an average cost of $8.00 per hour, and .2 hours of skilled labor at an average cost of $12.00 per hour.

Factory Overhead Budget • A factory overhead budget often includes all production costs other than direct materials and direct labor • Unlike direct materials and direct labor, manufacturing overhead costs include costs that vary in direct proportion with the units manufactured as well as costs that vary with either the kind of facilities the firm has or the way in which the firm carries out it operations

Labor Budget Factory Overhead Budget The variable overhead rate is $4.40 per direct labor hour. Fixed factory overhead is $44,300 during April and May, and $54,300 in June. Production Budget Also see Exhibit 8.10

Cost of Goods Manufactured Budget • The cost of goods manufactured production cost and the cost of goods sold budget reports the total budgeted cost of units sold for a period • Upon completion of the cost of goods manufactured and sold budget for a period, two items in this budget appear in other budgets for the same period • The income statement budget uses the cost of goods sold to determine the gross margin of the period, and the balance sheets includes the finished goods ending inventory it total assets

Selling and General Administrative Expense Budget • A selling and general administrative expense budget delineates plans for all non-manufacturing expenses • This budget serves as a guideline for selling and administrative activities during the budget period • Many selling and general administrative expenditures are discretionary

Cash Budget • A cash budget depicts effects of all budgeted activities on cash • By preparing a cash budget, management can: • take steps to ensure having sufficient cash on hand to carry out the planned activities • allow sufficient time to arrange for additional financing that may be needed during the budget period (and thus avoid high costs of emergency borrowing) • plan for investments of excess cash on hand to earn the highest possible return • A cash budget includes all items that affect cash flows and pulls data from almost all parts of the master budget • A cash budget generally includes three major sections: • Cash available • Cash disbursements • Financing

Cash Budget: Receipts • Management at Kerry expects 70% of all sales to be for cash and credit card sales, of which 40% are credit card sales that result in a 3% processing fee. • Of the company’s accounts receivable 80% are paid in the month following the month of sale, and 60% of these are paid within the discount period (2% discount allowed). • Of the remaining accounts receivable, 15% are collected in the second month following the month of sale, and 5% of accounts receivable eventually prove uncollectible. • Sales during March were $450,000.

Cash Budget $420,000 × 40% × 97% = $162,960 $450,000 × 30% × 80% × 40% = $43,200 $450,000 × 30% × 80% × 60% x 98% = $63,504 $400,000 × 30% × 15% = $18,000

Budget Income Statement • The budgeted income statement estimates the expected operating income from the budgeted operations • A budgeted income statement allows management a glimpse of the likely operating result upon completion of the budgeted operation • Once the budget income statement has been approved, it becomes the benchmark against which the performance of the period is evaluated

Budget Balance Sheet • The last step in a budget preparation cycle usually is to prepare the budget balance sheet • The starting point in preparing the budget balance sheet is the expected financial positions at the end of the current operating period--the beginning balances of the budget period