Download

1 / 23

230 likes | 376 Views

Overall assessment of the regulatory reform. Sergio Lugaresi, Public Affairs. Milan, 13 December, 2012. AGENDA. The debate Conflict of interests Impact assessment Overall assessment The future of the banking industry. 2. The Debate.

E N D

Overall assessment of the regulatory reform Sergio Lugaresi, Public Affairs Milan, 13 December, 2012

AGENDA • The debate • Conflict of interests • Impact assessment • Overall assessment • The future of the banking industry 2

The Debate • The “bank” critique (Jacques De Larosiere). Excessive capital requirements and the introduction of liquidity ratios and a leverage ratio will increase banking costs and reduce bank profitability. This will bust migration of certain financial activities into the unregulated shadow banking system and encourage banks to seek for higher returns taking more risk and reduce activities with modest margins such as lending to small and medium-sized enterprises. At the end the financial system will be not more stable but economic growth will suffer. The European economy, which is more bank dependent, will suffer the most. Effective regulation requires, instead, competent and efficient on-the-ground supervision. • The “academic” critique (Frank Allen, John Cochrane, Charles Goodhart, Eugene Fama, Markus Brunnermeier, Martin Hellwig, William Sharpe, Anjan Thakor). Basel III is far from sufficient. According to this view higher capital requirements will not increase funding costs: higher cost of equity will be compensated by lower cost of debt (Modigliani-Miller theorem). The substitution may be not perfect because of the tax bias in favour of debt. This bias should be removed. 3

Against the bank critique: Capital Requirements and Lending Decisions • The notion that increased capital requirements force banks to reduce lending activities is not necessarily true. • Higher capital requirements can be achieved through asset liquidation, de-risking , substitution of debt for equity (recapitalisation) or asset expansion. • Higher requirements can also be met by asset expansion: in this case the volume of loans does not change, while additional equity is raised and new assets acquired. The new assets acquired by the banks may simply be cash or other marketable securities, as it is often the case with non financial firms. Non financial firms in fact hold a relatively high percentage of their total assets in cash and marketable securities (~15-20%), without the concern that holding such securities is costly or unrelated to their core business. • A better capitalized bank is likely to make more appropriate lending decisions, which are less subject to incentives for taking excessive risk. 4

Against the bank critique: Capital Requirements and Return on Equity (ROE) • The notion that higher capital requirements would imply a lower ROE is not necessarily true. • Since ROE does not adjust for risk, it is not necessarily a measure of increased value, but is more likely the result of risk taking strategies; • The increase in capital provides downside protection that reduces shareholders’ risk. Shareholders will require a lower expected return to be wiling to invest in a better capitalized bank. Since the reduction in the required return for equity will offset the reduction in risk, value to shareholders remains unchanged. 5

Against the bank critique: Capital Requirements and the Cost of Capital • The cost of capital does not increase in case of higher capital requirements. • If a bank increases its equity relative to its debt, it reduces the riskiness of its equity because risks are spread over a wider base; • Investors in bank’s debt and equity do understand that the securities issued by a better capitalized bank are less risky, hence they price them appropriately. 6

Against the academic critique: Taxes • “Tax distortions [fiscal deductibility of interest and dividends on debt] have caused leverage to be substantially higher than it would have been under a neutral tax system” (IMF 2009) • It is very unlikely that authorities will be able to amend the tax code to address for the “tax bias” issue, at least in the forthcoming future. A coordination process across jurisdictions is even less likely. 7

Against the academic critique: Capital Requirements and Lending Decisions • The reduction in access to credit by riskier borrowers can have negative impact on innovation, productivity improvements, employment and the economic growth rate. Riskier borrowers, such as small businesses, have little or no alternative sources of funds other than from banks. • It is true that not every small business turns out to be a Google, however access to credit can be a crucial constraint on innovation and growth in small business sector. The issue is of particular relevance in Europe. 8

Against the academic critique: subtle effects of capital requirements • The seminal works of Gorton and Winton (1995) and Diamond and Rajan (2000) highlight some of the costs and subtle effects of capital requirements in models where • either there is a trade-off between the chance of bank failure and the lemons cost (i.e. the premium for asymmetric information) of capital, • or the bank’s asset side and liability side are intimately tied together. • “These effects emerge only when the capital requirements are seen in the context of the functions the bank performs rather than in isolation” (Diamond-Rajan 2000). These functions are to issue an information insensitive form of debt (checkable demand deposits) as a liability and to originate a unique form of debt (relationship loans) as an asset (Gorton-Winton 1995). 9

What is the real issue? • The starting point of the debate should have been “So why do banks fight so hard against capital requirements. That is, why is equity financing so much more costly than debt financing?” rather than “Do the M-M theorem hold?”. • This would have led to a common understanding of “the conflict of interests between bank shareholders and creditors, and due to the existence of [implicit] government guarantees, the […] conflict between shareholders and taxpayers” 10

The conflict of interests (1) • The fact that payment obligations on debt are fixed, regardless the bank’s asset performance, creates incentives for shareholders, and for managers acting on behalf of shareholders, to take risks according to the principle “heads, I win, tails, the creditor loses”. • “Under these strategies, increases in default probabilities, which hurt the creditors, are traded for increases in returns in the event where everything goes well, which benefit only shareholders”. 11

The conflict of interests (2) • This problem is exacerbated by: • asymmetric information, since in banking it is on average more difficult than in other sectors to understand the degree of risk of the business activities; • the existence of government guarantees, which greatly reduce the need for the creditors to worry about the bank’ strategy choices and default prospects. 12

The conflict of interests (3) • The conflict of interest could also be between managers and shareholders. • The so called “free cash flow” problem is based on the assumption that managers are able to withhold cash from shareholders to engage in wasteful investments. • “Free cash flow” is cash flow in excess of that required to fund profitable projects. The argument is that payout to shareholders reduce the resources under managers’ control, thereby reducing managers’ power. • Hence, managers have incentives to use the free cash flow even in non profitable investments rather than to let them being distributed as dividends. • A free cash flow problem leads to an excessive firm’s growth financed via debt. As a consequence of the incentive to growth via debt issuance, debt is perceived as more beneficial (hence less expensive) than equity. 13

The conflict of interests (4) • Instead of discussing the practical relevance of the M-M theorem, industry and authorities could have discussed these conflicts of interests and in case how fix them. • This would have shift the focus from capital requirements to corporate governance. To fix it would have included removing moral hazard through an appropriate bank resolution mechanism able to impose losses on bank creditors and to strengthening supervisors, which are the agents of bank creditors and taxpayers. 14

Impact assessment: IIF • In June 2010 the International institute of Finance (IIF) published its preliminary impact assessment (IIF 2010). • The logic of the model was straightforward: higher capital ratios and liquidity ratios raise costs which banks shift on lending rates to the private sector; higher lending rates reduce bank credit, which in turn, lowers GDP and employment. • The results devastating: the regulatory reform would subtract 0.6 percentage points from G3 (USA, Euro Area, Japan) GDP growth over the 2011-15 period with a loss of almost 10 million jobs. • The Euro Area would be hit the hardest. . 15

Impact assessment: MAG • In July, the Macroeconomic Assessment Group established by the Financial Stability Board and the Basel Committee on Banking Supervision published its Interim Impact Assessment (MAG 2010a). • A common set of scenarios served as inputs into almost 90 models developed for policy analysis in central banks and international organisations. • The results were obtained through a two-step approach: first the estimate of the effect of higher capital requirements on lending spreads and lending volumes; in a second stage using these estimates as inputs into standard macroeconomic forecasting models. The models’ results were pooled together to provide a median estimate. • Overall, the MAG’s estimates suggested a modest impact on aggregate output of the transition towards higher capital standards, significantly smaller than industry estimates (e.g., a reduction in GDP of 0.08% compared to 0.6% of the IIF). • The results were broadly confirmed in the Final Report published in December 2010 (MAG 2010b).. 16

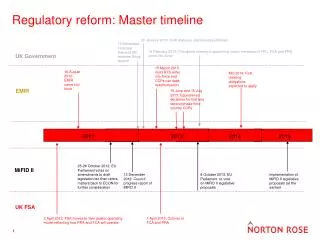

Overall assessment • Overall, the financial reform of international financial regulation carried out under the leadership of the G20 is a mix of innovation (leverage ratio, liquidity ratios, resolution, macro-supervision) and tentative repairs (nationally based prudential supervision, higher capital requirements based on risk weights). • It will be implemented at jurisdictional level in a long time span (up to 2019) under the only constrain of the peer review carried out by the BCBS. 17

Regulators’ vision • Narrow banking. Narrow banking means the separation from other banking activities and ring-fence of national socially relevant bank activities.

Appropriateness of detailed rules to foster international harmonisation of supervision? • Unsynchronised phase-in: some jurisdictions have decided to anticipate some rules, namely the new minimum capital ratios, with respect to the agreed timetable (e.g. Austria, then the EU); while Japan has already published the final rule, the US is lagging behind in the overall adoption of Basel 3 and the EU may postpone the entry date because of disagreement between Council and Parliament. • Inhomogeneous implementation: the transposition of the international Agreement into each single jurisdiction provides the opportunity for “fine tuning”: (“gold plating”, i.e. shaping the rules in way that favours national banks). • Accounting rules: despite efforts by international authorities to foster convergence in accounting rules between the US and the rest of the world and to define new financial rules in order to overcome existing differences, differences in accounting rules, in their national implementation, in the accounting practices and in their relations with regulatory rules remain a major source of supervisory practices. 19

Could have been different? • International authorities could have taken a more radical approach de-powering Basel pillar 1 (minimum capital ratios based on risk assessment), introducing simpler rules like a leverage ratio and rebalancing the international agreement in favour of pillar 2 (supervision), including macro-prudential supervision, through emphasis on independence, information and powers. • However, this would have been a radical departure from Basel 2, on which many of the BCBS members had worked in the past. • The approach chosen makes the new international agreement even more complex and detailed than Basel 2. • Loopholes and opportunities for regulatory arbitrage have likely not been reduced. • Shadow banking will likely increase. • Where will the next financial crisis originate? 20

The future of the banking industry • The future of the financial industry will be shaped by three exogenous developments: globalisation, regulation and technology. • Ring fencing and jurisdictional discretions in the implementation of the Basel Accords are unavoidable. What we can aim at is to improve coordination through the principle of “comply or explain”, extensive peer reviews and mutual recognition. • Regulators’ vision: narrow banking. • A technological trend already visible is the collective intelligence, i.e. connecting people and computers through devices that make easier and uninterrupted to access the Internet and increased computer storage capacity. While the divides between West and East and between developed and developing countries will dissolve, linguistic and cultural clusters of collective intelligence will continue to compete in the world market • The global and the technological developments will shape a financial industry that will be global in markets (although with more oversight) but more regional in players. 21

References • Admati,, Anat R. – De Marzo, Peter M. – Hellwig, Martin F. – Pfeiderer, Paul, “Fallacies, Irrelevant facts, and Myths in the Discussion of Capital Regulation: Why bank Equity is Not Expensive“, Stanford GBS Research Paper, No. 2063, September 2010. • International Institute of Finance (IIF), The Cumulative Impact on the Global Economy of Changes in the Financial Regulatory Framework, Washington DC, September 2011. 22

Next • Th. 11 Oct. h 10.30-12.15, aula 3 1. Introduction. Cross-border banking and regulation • Wed. 17 Oct. dalle 14.30 alle 16.15, aula seminari 2. Prudential Regulation: Lessons from the Crisis • Fri. 26 Oct. h 10.30-12.15 aula 3 3. From Basel 2 to Basel 3 • Thu. 8 Nov. h 10.30-12.15 aula 3 4. Moral hazard • Thu. 15 Nov. h 10.30-12.15 aula 3 5. Crisis Management and Resolution • Thu. 22 Nov. h 10.30-12.15 aula 3 6. Shadow Banking • Thu. 29 Nov. h 10.30-12.15 aula 3 7. • Thu. 6 Dec. h 10.30-12.15 aula 3 8. Rules and supervision • Thu.13 Dec. h 14.30-16.30 aula 20 9. Overall assessment of the regulatory reform • Mon.17 Dec. 10.30-12.15 aula 3 10. The Euro debt crisis and the Banking Union 23