Download

1 / 30

300 likes | 426 Views

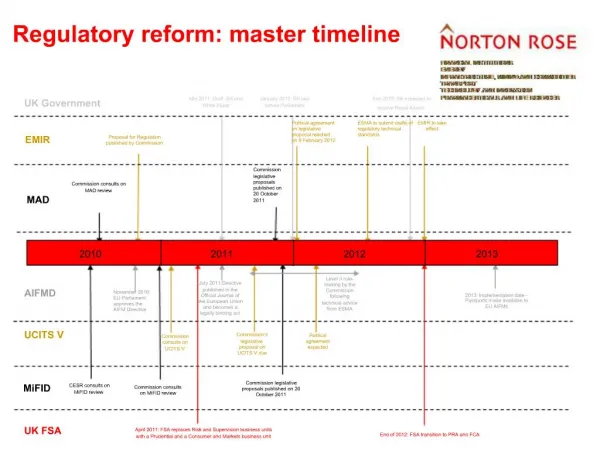

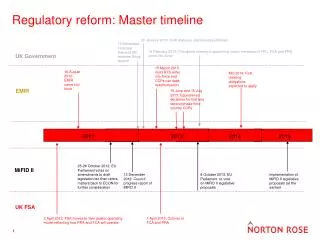

Regulatory Reform following the crisis. Too big to regulate?. Nations cannot – the US aside perhaps – regulate the banks. If the UK tried alone and a major bank said OK, we leave the UK, the consequences for the UK would be severe.

E N D

Too big to regulate? • Nations cannot – the US aside perhaps – regulate the banks. • If the UK tried alone and a major bank said OK, we leave the UK, the consequences for the UK would be severe. • Regulation either has to be international as with the Basel series of standards, or by an authority even bigger than the banks (the EU?) laying down the law.

Basel III • Basel I and Basel II set out rules and guidelines for banks to follow, e.g. Capital ratios. • These were theoretically voluntarily, but most banks really have to follow them. • But Basel II was inadequate to the task and hence we now have Basel III

Basel III Basel III provides for • higher minimum capital requirements, • better risk capture (i.e. to do a better job in evaluating the risk of assets such as mortgage backed securities, • a stricter definition of eligible capital elements with a particular focus on common shares • greater transparency. • The Basel III rules will be transposed into national or European law

Basel III • By 1 January 2015, the minimum capital requirements for common equity Tier 1 and total Tier 1 capital will gradually be raised up to a level of 4.5% and 6.0% of their risk bearing assets, respectively. • Note in some countries such as Sweden these requirements are much tougher. • Tier 1 capital is the core measure of a bank’sfinancial position. It is composed of core capital (e.g. common stock and reserves) • tier 2 capital is composed of less core capital

Tier 2 Capital: examples: • A revaluation reserve is a reserve created when a company has an asset revalued (e.g. Land bought 20 years ago, revalued at today’s price). • Provision for anticipated future losses which have not yet occurred.

Different to the reserve ratios you have met before. • These capital requirements are totally different from the reserve requirements a central bank requires commercial banks must hold of cash and deposits with the central bank with respect to its lending.

Basel III also specifies • Systemically important financial institutions should have additional loss absorbing capacity • i.e. financial institutions which if they go bust will have substantial repercussions on the financial system must have higher reserves. • Work is currently underway on how to define institutions that are ‘systemically important’, and the appropriate capital surcharges, etc to limit systemic problems.

Revising economics • In the crisis risks in market returns were not mainly exogenous, coming e.g. from the stochastic variation in the real economy. • They came from financial risk itself. The financial structures that were thought to assess, absorb and neutralise risk – they did not.

Revising economics • Key factors in creating this risk were opaque financial structures, particular vulnerability to contagion and domino effects, and pro-cyclicality in financial markets. • The role of distortions in economic incentives is fairly well known even within neo-classical economics. • But herd behaviour as a driver of pro-cyclical patterns in financial markets still needs a thorough explanation and integration into economic theories.

Two possible explanations for ‘herd behaviour’: • the significance of a market player’s evaluation of his or her performance relative to the rest of the market. Market participants do not form their own opinions, but follow the general mood prevailing among market participants. Everybody seeks to follow general sentiment, hoping to anticipate turning points in sentiment. • Global markets are in fact less atomistic (many small players, none with influence) than thought. Hence one or two key players can have substantial influence. For example, derivatives activity in the US banking system is dominated by a small group of large institutions. And the market for credit ratings is dominated by three firms. Similar, copycat, behaviour is much more likely than would be the case with atomistic markets (i.e. Many players).

New Directions • In general work is underway to incorporate into economics new ideas and approaches including insights from physics and biology which do not necessarily rely only on the notions of equilibrium, universal rationality and efficiency which underlies much of economics. • Could this be the beginning of the economics revolution many are anticipating in the light of the crisis?

Back to regulation: Macro-prudential oversight • As we have seen, major risks can emerge from within the financial system itself. Endogenous risks – risks that emerge from within the financial sector – can have many causes. • They may arise, for example, because large parts of the system rely on the same sources of funding, or because they have similar exposures – to rising financial imbalances, to currency mismatches and to widespread mis-pricing of risk.

The European Systemic Risk Board • For these reasons, we need a new framework of macroprudential supervision e.g. The new Financial Stability Oversight Council in the US and the ESRB, the European Systemic Risk Board: http://www.esrb.europa.eu/home/html/index.en.html

The ESRB (founded in December 2010) • “shall contribute to the smooth functioning of the internal market and thereby ensure a sustainable contribution of the financial sector to economic growth.”

The ESRB will do this by: • identifying and prioritising systemic risks; • issuing warnings where such systemic risks are deemed to be significant and, where appropriate, make those warnings public; • issuing recommendations for remedial action in response to the risks identified and, where appropriate, making those recommendations public. • In this way it is trying to anticipate future problems in the financial system, much more than was previously the case. • In doing this it will co-operate with other European and international agencies (e.g. The IMF and the newly created Financial Stability Board, FSB).

The FSB • The FSB has been established to coordinate at the international level the work of national financial authorities and international standard setting bodies and to develop and promote the implementation of effective regulatory, supervisory and other financial sector policies • It was established in April 2009 as the successor to the Financial Stability Forum (FSF). • Following the crisis, as announced in the G20 Leaders Summit of April 2009, an expanded FSF was re-established as the Financial Stability Board with a broadened mandate to promote financial stability.

The FSB’s mandate • Assess vulnerabilities affecting the financial system and identify and oversee action needed to address them; • promote co-ordination and information exchange among authorities responsible for financial stability; • monitor and advise on market developments and their implications for regulatory policy; • manage contingency planning for cross-border crisis management, particularly with respect to systemically important firms; and • collaborate with the IMF to conduct Early Warning Exercises.

Apart from the ESRB: • Three pan-European micro-prudential supervisory authorities have been • the European Banking Authority (EBA), • the European Securities Markets Authority (ESMA) • the European Insurance and Occupational Pensions Authority (EIOPA). • Regulation is back in fashion

Foresight • The foresight activities of these bodies are important and supervision needs to keep pace with a changing environment • The world is continually changing and the authorities will need new regulatory instruments to keep pace with the impact of new technologies – including high frequency trading, algorithmic trading and the new universal trading platforms • that is today, but then there is tomorrow.

In the shadows • But there is a risk that in regulating part of the financial system, agents are pushed into other parts – the shadow banking sector, which is less regulated. • The activities in the shadow banking sector and the over-the-counter business have contributed tremendously to the creation of uncertainties and opaque transmission channels for risks. • Therefore, a central goal for any future regulatory action should the improvement of market transparency.

The crisis has shown that the exclusive focus on banks has proven insufficient as contagion has also occurred across different types of financial intermediaries, such as insurance companies and money market funds. • Therefore, looking forward it will be crucial that the cross border cooperation between authorities be further strengthened. In this respect the work of the newly created European Supervisory Authorities will be key.

In the UK • Prudential Regulation Authority • The Government is creating a new Prudential Regulation Authority (PRA) as a subsidiary of the Bank of England (the Bank) to conduct prudential regulation of sectors such as deposit-takers, insurers and investment banks. • The PRA will be chaired by the Governor of the Bank (of England).

And....... • In addition to the PRA, there will be a new Consumer Protection and Markets Authority (CPMA), separate from the Bank, to regulate the conduct of all financial firms, including those prudentially regulated by the PRA.

And................ • Financial Policy Committee • A Financial Policy Committee (FPC) in the Bank, which will be placed in charge of macroprudential regulation. • It will have responsibility to look across the economy at macroeconomic and financial issues that may threaten stability and will be given tools to address the risks it identifies. • It will have the power to require the new PRA to implement its decisions by taking regulatory action with respect to all firms.

The Financial Stability Report • http://www.bankofengland.co.uk/publications/fsr/index.htm • The Financial Stability Reportis published half-yearly by Bank staff under the guidance of the Bank’s Financial Stability Executive Board. • It aims to identify the major risks to UK financial stability and to stimulate debate on policies needed to manage and prepare for these risks.

Thus the response to the crisis • The beginnings of a revolution in economic theory which help us understand the financial system and its links with the real economy. • Greater regulation of the banks at national and international levels with stronger capital requirements • A particular focus on large institutions who pose a particularly severe problem of systemic risk • An emphasis on foresight • All accompanied by the creating of a whole host of new institutions at national and international level.

Will it work? • Yes • For a time, but eventually the memory will fade. Politicians and bankers, journalists and academics (some) will forget the lessons of 2008, just as we forgot those of 2009. • Then, say in another 30 years time crisis will hit us again.

Financial crises are not new • During the early Roman Empire substantial revenues allowed the state was able to undertake a substantial public works. • A new emperor, Tiberius, cut back on the building program and hoarded large sums of cash. • This led to a financial crisis in 33 A.D. A severe shortage of money. and the reduction of state expenditures led to a sharp downturn in economic activity. • Zero interest rates once more saved the day, with the state making large loans in order to provide liquidity

The Glass–Steagall Act • The Banking Act of 1933 established introduced banking reforms in the US, which in part were introduced to control speculation. • The Depository Institutions Deregulation and Monetary Control Act of 1980 repealed part of lass Steagel • The Gramm-Leach-Bliley Act of 1999 repealed provisions that prohibited a bank from owning other financial companies. • This effectively removed the separation that previously existed between Wall Street investment banks and deposit banks. • This was a factor in the severity of the crisis