Download

1 / 17

170 likes | 285 Views

"Learn how driving without auto insurance can lead to legal consequences, financial responsibility, and high premiums. Discover simple ways to lower insurance costs. Shop around, increase deductibles, eliminate unnecessary coverage, and maintain a clean driving record."

E N D

Driving without insurance is a risky proposition. Although it might save you money in the short run, the potential long-term consequences make these savings not worth the risk. For one, you could face serious legal repercussions for driving without insurance. But legal woes are probably the least of your worries. If you are uninsured and are in an accident that is your fault, you will be financially responsible for paying for the damages and injuries of the parties involved. Unless you’re independently wealthy, that means one minor fender bender could jeopardize your assets and put you on the brink of bankruptcy. Driving without insurance is dangerous and expensive.

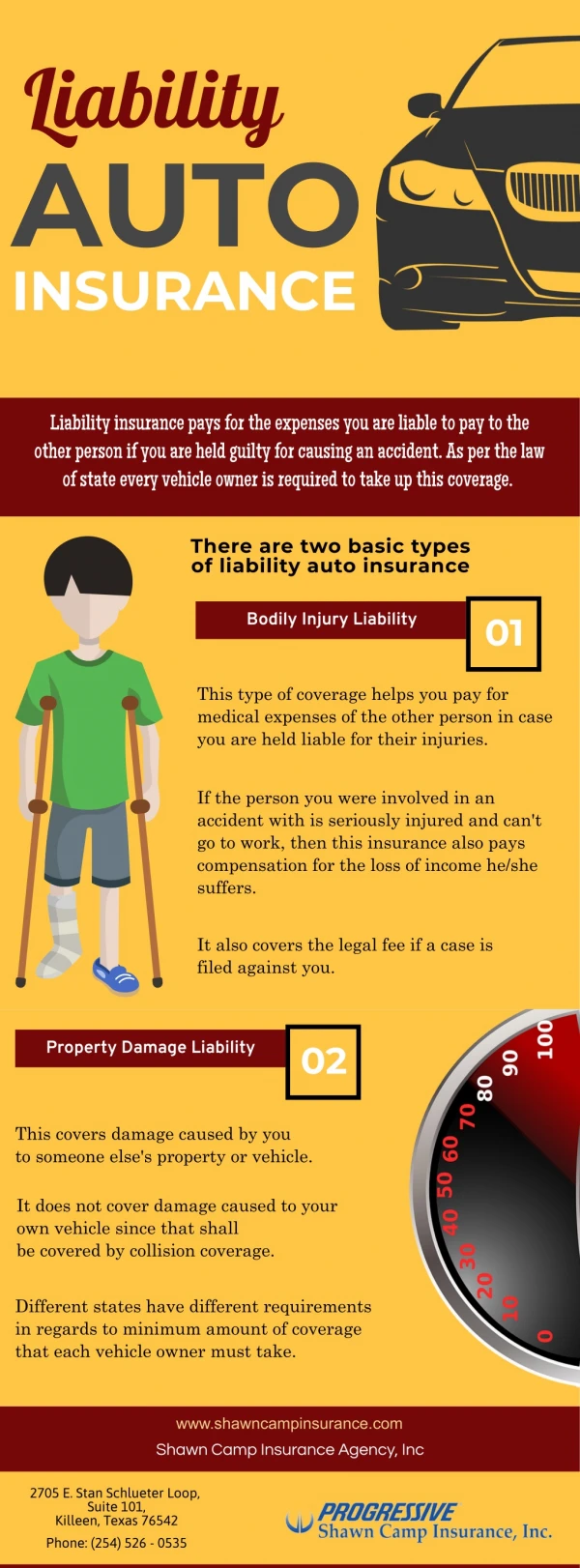

Legal Issues Most states require that you carry minimum levels of liability coverage. If you are caught driving without the mandatory levels of insurance, you could face an array of unpleasant consequences. In some states, your vehicle tags may be revoked and the car impounded. Other states charge uninsured drivers heavy fines, usually ranging from $150-$500. You might also have your license revoked for a certain period of time if you fail to provide proof of insurance.

Financial Responsibility Though not every state requires you to carry liability insurance, all states do have at least a financial responsibility law. Those states with financial responsibility laws do not require drivers to have liability coverage with an insurance company, but they do require that all drivers prove that they are financially able to cover their liability in the event of an accident. In these states, any of the following items qualifies as proof of financial responsibility: • Self-insurance certification • Certificates of deposit • Surety bonds

Lapses in Coverage Mean High Premiums If you’re driving without insurance, you will have lapses in coverage on your record. That means that if you ever apply for an auto insurance policy, your prospective insurer will find this out. To insurers, lapses in coverage are red flags for high-risk drivers. Any lapse in coverage, no matter how short, could result in sky-high premiums or your insurance application being denied.

Auto insurance can be a very expensive necessity. A good policy can cost you anywhere from a few hundred to a few thousand dollars a year. This can be quite the strain on your budget if you are overpaying for your auto insurance. To reduce this strain, we’ve compiled ten simple tips to help you lower your auto insurance premiums by as much as 40%. Here’s what you can do:

Shop around. It is always a good idea to compare many different policies when you are shopping for auto insurance. Most experts recommend that you get at least two or three quotes on policies before committing to one. This will help you find the best deal. • Increase your deductibles. As a general rule, the higher your deductibles are, the lower your premiums will be. This is because you are assuming more financial risk with higher deductibles, so the insurance company is able to offer you reduced premiums. However, keep in mind that higher deductibles mean higher out-of-pocket costs if you are in an accident.

Eliminate certain coverage's from your policy. Not all auto insurance coverage's are absolutely necessary. You want to keep coverage's like bodily injury liability and property damage liability, as these are required by law. Coverage's that you might eliminate include collision, comprehensive, medical payments, and uninsured motorist. 4. Drop collision & comprehensive for older cars. If you drive an older car with little to no cash value, collision and comprehensive coverage will do you no good. The insurance company will only reimburse you for damages up to the cash value of the vehicle.

Keep your credit report looking good. Your credit report is one factor that influences your premiums. By paying your bills on time and maintaining a good credit history, you can keep your insurance rates low. 6. Drive less. Most insurers offer low-mileage discounts to policyholders who drive less than a certain number of miles per year. You can use the bus, carpool with friends, or take a plane when driving to another state to save on mileage.

Keep your driving record clean. You will enjoy a significant discount if you do not have any moving violations within a certain period of time. Try to avoid accidents, speeding tickets, etc. by driving defensively at all times. 8. Select a low-profile car. Sports cars and high performance vehicles will cost more to insure because they are a higher theft risk and the drivers of these vehicles are more likely to be reckless. Large vehicles and new cars also cost more to insure. Low-profile cars include relatively small, safe sedans.

Look into safety & security discounts. You may qualify for certain discounts if your car is equipped with the following safety features: air bags, anti-lock brakes, automatic seat belts, tracking systems, car alarms, etc. 10.Ask about other discounts. Insurers offer a plethora of discounts, but you usually have to ask about them first. Ask your agent about discounts for which you might be eligible.

Taking the big plunge will radically alter your life, and your car insurance policy is no exception. Once you get married, you will need to change your coverage so both of your policies are from the same company. If you both already have policies from the same insurer, then you should contact your agent about purchasing a single policy together. After you get these logistical issues squared away, there is good news: getting married almost always saves you money on your car insurance. Statistical data indicate that married people are less of a claims risk than their single counterparts, and, as a married man or woman, you will reap the rewards—lower premiums. In this post, we’ll give you some basic information about marriage and car insurance and explain how to go about merging your policies.

Marriage & Auto Insurance Here is some helpful information about marriage and car insurance: • Car insurance rates usually drop for men (and sometimes women) under the age of 25 when they get married • You can save money and simplify your life by consolidating all of the insurance policies in your new household • As a married couple, you may qualify for several discounts, including the multiple-vehicle and multiple-policy discount

Test your driving knowledge! http://moneycentral.msn.com/ quiz/driving-skills-quiz/home.aspx