Download

1 / 17

170 likes | 584 Views

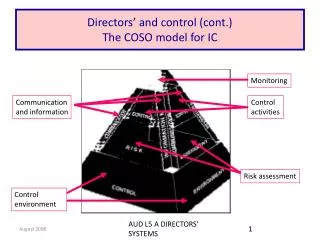

Directors’ and control (cont.) The COSO model for IC. Monitoring. Communication and information. Control activities. Risk assessment. Control environment. Directors’ and control (cont.) The COSO 2 model for IC. DOCUMENTS COMPUTER controls ARITHMETIC REVIEW RECONCILIATION COUNTS

E N D

Directors’ and control (cont.)The COSO model for IC Monitoring Communication and information Control activities Risk assessment Control environment AUD L5 A DIRECTORS' SYSTEMS

Directors’ and control (cont.)The COSO 2 model for IC AUD L5 A DIRECTORS' SYSTEMS

DOCUMENTS COMPUTER controls ARITHMETIC REVIEW RECONCILIATION COUNTS EXTERNAL information ACCESS Authorisation Recording Custody 'CARDCARE' 'ARC' Control Activities (Procedures) AUD L9a IC 1 INCOME CYCLE Introduction

‘Walk through’ tests • Can the ‘audit trail’ be followed (both ways)? • FS Assertion ETB NL Prime books Source documents • Source documents Prime books NL ETB Assertion FS AUD L6b/c SYSTEMS DOCUMENTATION

‘Walk through’ tests (cont.) • Do all recorded ‘control activities' (procedures) exist? • Examples of controls being: • An authorisation of a sale, • A check of a casting, • A reconciliation of a control a/c… AUD L6b/c SYSTEMS DOCUMENTATION

Recording systems • Narrative notes • Flowcharts • ICQ’s • Internal control questionnaires • Controls based • ICE’s / ICEQ’s • Internal control evaluation (questions) • Risk based AUD L6b/c SYSTEMS DOCUMENTATION

ICQ’s • A series of questions asking if expected IC’s exist • Written so that answers indicate • if YES = a strong control • if NO = a weak control • All controls would be included • An ICQ would usually be drawn up for each income and asset cycle • The major cycles are sales, purchases, wages, cash, inventory, non-current assets AUD L6b/c SYSTEMS DOCUMENTATION

ICQ’s (cont.) • All appropriate internal controls should be included in an ICQ • Each answer (yes or no) must be considered individually as (in terms of likely material misstatement) - • some controls are not as important as others • some may be irrelevant AUD L6b/c SYSTEMS DOCUMENTATION

ICE’s • Rather than considering all expected IC’s, the ICE is based on the likelihood of error or fraud in each cycle • ‘Key (or control) questions’ are established • Each key question has a supporting bank of detailed questions • Some ICE’s are written so that answers indicate - • if YES = strong control • if NO = weak control AUD L6b/c SYSTEMS DOCUMENTATION

ICE’s • An ICE too would usually be drawn up for each income and asset cycle • Example (Sales cycle) • Objective:Are all sales invoices recorded? • A key question in the sales cycle • Supporting question: Are invoices sequentially numbered? AUD L6b/c SYSTEMS DOCUMENTATION

Flowcharts • Organisation charts • Audit trail / information flowcharts • Document (and control) flowcharts • Systems (computer) flowcharts AUD L6b/c SYSTEMS DOCUMENTATION

Flow charts for auditors - general rules • No standardisation in auditing profession • Main general rules • FLOWLINE DIRECTION • Non-standard SYMBOLS should be explained • GHOSTED SYMBOLS ( ) • NARRATIVE COMMENTARY • MOVEMENT is that of TIME (and SPACE) AUD L6b/c SYSTEMS DOCUMENTATION

One dimensional flow charts • 1D charts move in time • Ideal for systems based on algorithmic logic (computers) and simple auditing charts AUD L6b/c SYSTEMS DOCUMENTATION

Two dimensional flow charts • 2D charts move in time &space • Ideal for auditors, where IC evaluation is important • Each ‘function’ (ordering, sales, goods in…) is laterally placed and internal controls identified AUD L6b/c SYSTEMS DOCUMENTATION

Two dimensional flow charts Time OrderingSalesWarehouseAccounts… AUD L6b/c SYSTEMS DOCUMENTATION

What Does Generally Accepted Accounting Principles - GAAP Mean?The common set of accounting principles, standards and procedures that companies use to compile their financial statements. GAAP are a combination of authoritative standards (set by policy boards) and simply the commonly accepted ways of recording and reporting accounting information.

What Does Generally Accepted Auditing Standards - GAAS Mean?A set of systematic guidelines used by auditors when conducting audits on companies' finances, ensuring the accuracy, consistency and verifiability of auditors' actions and reports.