Download

1 / 39

390 likes | 498 Views

This research explores the impact of changing credit conditions on housing market bubbles in the US and UK. The study delves into the complexities of detecting bubbles in asset prices, with a focus on house prices, and highlights the connection between credit availability and house price fluctuations. By using econometric models and simulations, the authors provide insights into the dynamics of house price movements and the role of credit standards. The paper also discusses the challenges of identifying bubbles based on fundamental factors versus speculative influences in the housing market.

E N D

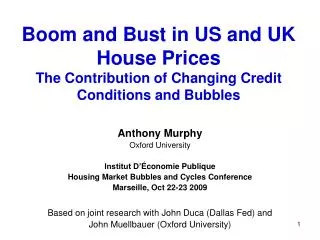

Boom and Bust in US and UK House PricesThe Contribution of Changing Credit Conditions and Bubbles Anthony Murphy Oxford University Institut D’Économie Publique Housing Market Bubbles and Cycles Conference Marseille, Oct 22-23 2009 Based on joint research with John Duca (Dallas Fed) and John Muellbauer (Oxford University)

Outline • Bubbles and changing credit conditions • Explaining US house prices • Inverted demand house price equations • House price to rent equations • Future US house prices – a simulation • Credit conditions and UK house prices • Concluding remarks

Bubbles • It is difficult to detect bubbles in asset prices using formal econometric tests. • The tests have low power and are based on a range of auxiliary assumptions. • For example, Gurkaynak (J. Econ Perspectives 2008) suggests that bubble tests of equity prices …“do not do a good job of differentiating between mis-specified fundamentals and bubbles…. It is a matter of taste and personal preference that makes the econometrician choose between bubble and fundamentals-based explanations of stock price behaviour.”

Bubbles (Cont’d) • I believe the same caveats apply to detecting house price bubbles – persistent deviations of house prices from “fundamentals” - where we have even less data and less agreement on fundamentals. • In the US and the UK, many house price bubble episodes appear to be generated by changes in credit conditions, which were either long term changes or widely perceived to be long term changes at the time (e.g. the subprime revolution).

In a Nutshell • Standard econometric house price models for the US (and, to a lesser extent, the UK) do not work well in sample ….so not very useful for policy analysis or simulation. • Why? • Econometric answer – mainly structural break, due to classic omitted variable bias. • Economic answer – models do not take account of changing credit conditions / standards.

In a Nutshell (Cont’d) • Easier credit drives up the house price to income and house price to rent ratios, ceteris paribus. • Proxy mortgage credit conditions for the US using the cyclically adjusted trend in the loan to value ratio (LTV) for first time buyers. Source: American Housing Survey. • The adjusted LTV data are consistent with standard accounts of lax credit conditions and the growth in sub-prime lending etc.

Aside: The US Housing Bust(A Scary Bedtime Story for Central Bankers) • Financial innovations in securitization and changes in procedures by rating agencies, inter alia, resulted in the sub-prime revolution. • Loans were extended to borrowers with poor credit histories, previously denied loans. • Many of the loans were for adjustable rate mortgages which particularly benefited from the lowest interest rates for decades in 2001–2003. • The house-price rises, set in train by these credit-supply and interest-rate changes, fooled many people into thinking that such rises would be sustained. • Fundamentals changed in 2003 as interest rates returned to more “normal” levels, and high rates of building expanded the housing stock, while house prices became increasingly overvalued. • As the extent of bad loans gradually became clear, the fundamentals changed again, as the supply of credit for all types of mortgages contracted.

In a Nutshell (Cont’d) • Two basic (theoretical) approaches to modelling house prices – the inverted housing demand and house price to rent approaches. • Our LTV based measure of credit conditions work well in both econometric models: • LTV highly significant; • Obtain plausible and (more) stable long run equilibrium parameters and adjustment speeds; • Models track well in pseudo out of sample forecasts. • Can use models to examine various interesting scenarios.

What Do We Want To Explain? US House Prices Gains 1999-2006 2006:q4 +45% +34% +26%

What Do We Want To Explain (Cont’d)? Recent US House Prices Falls 2008:q4 +23% +11% + 6% Source: Freddie Mac, Bureau of Economic Analysis, Federal Reserve Board.

Econ 101 – What Determines House Prices?Two Models. • The most basic theory of what determines house prices is just a story of supply and demand, where the supply - the stock of houses - is given in the short run. • Then house prices depend on the stock of housing and the factors driving demand. • This is our inverted housing demand model. • In the US, where rental markets are well-developed and rents are generally market determined, the most popular model of house prices is the house price to rent model.

Model 1The Inverted Housing Demand Model • The inverted demand equation is obtained by considering the demand for housing services: where hp = real house price, y = real income, and z = other demand shifters. • Own-price and income elasticities are – and β. • Inverting yields:

Demand Shifters (z’s) in the Inverted Demand House Price Model • Housing is a durable good (with an investment component) expected or ‘permanent’ income and ‘user cost’ should be important drivers. • User cost = after-tax interest rate + property tax rate + depreciation rate - expected rate of house price appreciation (less transactions costs). • Expected capital gains seldom observed so must be proxied by past capital gains or a reduced form model etc.

Bubble ‘Builder’ and ‘Burster’ Dynamics • Housing market not efficient, so systematic mis-pricing (over or under shooting) can persist for quite a while. • There is also a large extrapolative element in expectations. • A series of positive shocks to fundamentals can lead to rising prices and the expectation of further appreciation, leading to greater and greater overvaluation. In due course, the increasing negative pull from fundamentals and increased supply reduce the rate of appreciation. • Lagged house price capital gains or losses are an important determinant of current house prices, termed the ‘bubble-builder’ by Abraham and Hendershott (1996). • The deviation of prices from long-run ‘fundamentals’ is then the ‘bubble-burster’.

Yet More Explanatory Variables! • Demography e.g. the proportion of households in the under-35 age group where many first-time buyers are to be found. • Many mortgage borrowers face limits on their borrowing and may be risk averse nominal interest rates and proxies for downside risk or mortgage default may be important. (Cameron et al., 2006). • Finally, changes in credit conditions matter for house prices (and savings), particularly in the US and UK.

Model 2 The Ratio of House Price to Rents • Ceteris paribus, arbitrage between owner-occupied and rental housing markets implies the house rent-to-price ratio equals the real user cost of housing. • Hence, the log house price-to-rent ratio equals the log of the inverse of real user cost: • Very simple and attractive model…. • But misleading if credit conditions vary etc.

More Realistic Model of House Price / Rent Ratio • Kim (2007) show that in a model with binding (max LTV) credit constraints for marginal home buyer, plus rental agency costs: • ydev = deviation of income from trend • The negative user cost elasticity can be smaller than one.

The Inverted Demand Model - Data • Home Prices: Freddie Mac repeat sales of homes purchased with conforming mortgages. Deflated using PCE index. • Income: Real per capita labor plus transfer income. • Real Mortgage Rate: After tax and depreciation adjusted nominal mortgage rate, minus 16 quarter annualized appreciation (adjusted for home selling costs). • Real Housing Stock: Fed’s Flow of Funds estimate of the replacement cost of housing structures, deflated by housing construction price index. • Monetary Target Regime: Dummy for monetary targets that boosted interest rate volatility (1979 Q4 to 1982 Q3) • Deposit Regulations: Two quarter change in effect of Regulation Q (REGQ) dis-intermediation policy. • Tax Variable:Tax advantage to housing capital gains since 1998 Q1

Inverted Demand Model Results • Our mortgage credit conditions measure is highly significant (both economically and statistically). • Can treat it as exogenous. • Models with credit conditions are more stable. • In pseudo out-of-sample forecasts, models without the credit conditions measure do not track the sub-prime boom and bust. • Models with the credit conditions measure do. • Credit conditions effect identified in the data by (small) earlier relaxations in mortgage credit standards.

VEC (Vector Error Correction) Inverted Demand Results Vectors allow trends in variables but not in the cointegrating relationship. Controls include 0-1 dummies for monetary targeting regime and 1998 capital gains tax relief, depreciation rate on rental properties, and consumer income/interest rate expectations. Statistics from Tables 1 and 2 from the paper.

Real House Prices Tracked Better by Long Run Equilibrium of LTV vs. Non-LTV Models

Long Run Equilibrium House Prices Similar for LTV Models Estimated With & Without 2002-2007

House Price to Rent Model Results • Our findings are qualitatively similar when we model the house price to rent ratio. • Models with our LTV based measure of credit conditions perform better. • One specification of the estimated long run rent and house price to rent equations for the US is: • The estimated speeds of adjustment to the long run equilibrium are very slow, since rents are very sticky.

March 2009 Hostage to Fortune - The Simulated Path of Future US House Prices • If our model is correct, the US house price bust may last quite a long time! • Our March 2009 simulated path of future real US house prices, shown in next figure, assumed that: • The US economy recovers very slowly – no real income growth and unemployment only returning to its long run average in 2014 ; • Mortgage credit condition revert to their end 1999 value; • Actual house prices have not fallen as fast in the past two quarters.

Real House Price Simulation Based on House Price-to-Rent Model (LTVs Revert to 1999 Q4 Level in 2008 Q4)

A Run Thru’ Some UK Results • Cameron, Muellbauer & Murphy (2006) Mmodel house prices for 8 regions of Great Britain between 1972 and 2003 with a system of inverted demand, equilibrium correction equations. • The housing stock is an explanatory variable along with regional income, real and nominal interest rates, demographics and other demand shifters, especially credit conditions. • Identify significant direct and indirect (via real and nominal interest rates) effects of more liberal credit conditions.

ABC of Regional House Price Models • At regional level, demand in a region depends on own-price and prices in other regions. • If prices are simultaneously determined, we have to invert system of demand equations. • This is why (log) house price in a region depends on log income/house etc. in own region and in other regions. • US studies of house prices at Metropolitan Area level all use “Lucas islands” paradigm – neglect substitution between nearby locations.

Long Run Effects – Income Per House • The long-run solution is for the real log level of house prices in region r. • The key element in the long-run solution is the log of real personal disposable non-property income per house. • For region r, this is defined as: log(real non-property income) - log(housing stock)-1 - 0.7*log(rate of owner-occupation)-1 in region r. • Modest spill-over from non-owner occupied supply onto the owner-occupied housing market.

All regions are influenced not just by the own region value of income per house but also by the GB value, with weights of ⅓ and ⅔ respectively • The long-run effect of log real income per house on the log real house price is 1.6, in line with previous studies. • The speed of adjustment to long run equilibrium is allowed to vary with Stamp Duty rates.

Figure 7: Equilibrium Correction Terms 0.5 0.4 0.3 0.2 0.1 0.0 -0.1 -0.2 -0.3 Greater London West Midlands North -0.4 • Figure 7 shows one version of an equilibrium correction term including income per house, Greater London catch up, credit and interest rate effects. • The figure suggests that, given interest rates, incomes, population and housing stock, Greater London was only moderately overvalued in 2003, while the West Midlands and the North were substantially undervalued 1975 1980 1985 1990 1995 2000 2005

Long Run Effects of Credit Conditions • Used an index of credit conditions (CCI) which measures credit supply to UK households. • We find a significant CCI levels effect, as well as interaction effects of CCI with both the nominal mortgage rate and the real mortgage rate. • Ceteris paribus, easier credit conditions raises house prices by relaxing downpayment constraints. • In addition, nominal rates matter less and real rates more (so intertemporal effects are more important) when credit availability improves. • Consistent with findings for mortgage demand by Fernandez-Corugedo & Muellbauer (2005) and consumer spending by Aron, Muellbauer & Murphy (2006).

Figure 3: Long Run Effects of Credit Conditions and Interest Rates 0.3 0.2 Credit Conditions CCI (Excd Interactions) 0.1 0.0 Interest Rates (Incld CCI Interaction) -0.1 -0.2 • Figure 3 shows the estimated long-run effect of the credit conditions index (cci) and real and nominal mortgage rates interacted with cci. • Relative to the 1970s, the estimated effects of cci, in terms of its direct, positive effect on real house prices, is roughly canceled out by the effect of the rise in real interest rates. 1975 1980 1985 1990 1995 2000 2005

Some Short Run Effects Short run effects include: • house price and income dynamics as well as • changes in nominal interest rates, • new housing supply, • population structure inter alia.

Model Adequacy and Recent Bubble • Overall the model fits well, although there is some evidence of mild autocorrelation in one equation. • The stability of the model was checked by estimating it on different sub-samples. • In particular, there is no evidence that we over fitted the house price boom at the end of the sample (1997-2003). • Conclusion: No evidence of bubble?

Difficulties in Detecting Bubbles • Does a bubble imply substantial positive residuals (i.e. under-predictions) when forecasting house prices for recent years, given parameter estimates for earlier years? • No, regularities in the dynamic behaviour of house prices may be well captured by a model with extrapolative expectations, so that bubbles can arise without such residuals being found. • A more decisive test? Using plausible scenarios for the drivers of house prices (e.g. long run values) for the next 5 to 10 years, is a major decline likely? • Difficulty - There is a range of uncertainty about long-run values!

Detecting Bubbles and Prospects for UK House Prices • At the time, many regarded the expansion in credit supply in the US from 2000 to 2005 as a permanent shift! We now know that it was unsustainable. • Thus, what may have looked like a permanent shift in US and UK equilibrium house prices now looks like a bubble. • In the UK, credit conditions have worsened substantially since the start of 2008. • Over time, credit conditions will improve somewhat and new housing supply is severely constrained so house prices will recover in the long run, albeit to a lower level than before the current bust,

To Do • Mainly data issues! • Update credit conditions index CCI • New survey of mortgage lenders with extended coverage – sort out discontinuities; • Data not published any longer – need access to data. • Revisions in historical national and regional employment data. • New regional personal income data.