Importance of Conversion Analysis in Forensic Accounting

100 likes | 230 Views

This presentation explores the significance of studying conversion analysis in forensic accounting, focusing on its role in detecting fraud and facilitating confessions. It outlines various sources of information useful for forensic investigations, including government and financial records. The net worth calculation method for estimating undisclosed income is discussed. Additionally, effective interviewing techniques, including types of questions and facilitators that enhance information gathering, are highlighted. The presentation also addresses potential inhibitors that might obstruct successful interviews.

Importance of Conversion Analysis in Forensic Accounting

E N D

Presentation Transcript

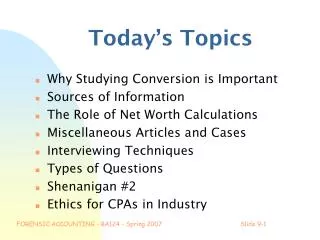

Today’s Topics • Why Studying Conversion is Important • Sources of Information • The Role of Net Worth Calculations • Miscellaneous Articles and Cases • Interviewing Techniques • Types of Questions • Shenanigan #2 • Ethics for CPAs in Industry FORENSIC ACCOUNTING - BA124 – Spring 2007 Slide 9-1

Role of Conversion Analysis • Helps determine the extent of the fraud • Serves as a facilitation for confession FORENSIC ACCOUNTING - BA124 – Spring 2007 Slide 9-2

Sources of Information(Study pages 247-255) • Variety of sources • Federal government sources • State government sources • Local government sources • Financial institution records • Public databases • Internet sources Don’t try to memorize the details of these sources. Know how to use some of them. FORENSIC ACCOUNTING - BA124 – Spring 2007 Slide 9-3

Net Worth Method • For use in estimating “Funds from Unknown Sources” • Calculation: • Assets - Liabilities = Net Worth • NWc - NWP = Net Worth Increase • NWI + Living Expenses = Income • Income - Known Sources = Unknown Sources FORENSIC ACCOUNTING - BA124 – Spring 2007 Slide 9-4

General Interview Guidelines • Be aware of the “crisis cycle” • Remain a people person • Engage rather than challenge • Conduct the interview as close to the event as possible • Plan for the interview • See text for demeanor (p.274) & language (p.274) FORENSIC ACCOUNTING - BA124 – Spring 2007 Slide 9-5

Types of Questions • Introductory • Informational • Assessment • Closing • Self Admission-use carefully FORENSIC ACCOUNTING - BA124 – Spring 2007 Slide 9-6

Interview Facilitators • Expectation fulfillment • Recognition • Altruism • Sympathy • Newness • Catharsis • Sense of meaning • Availability of rewards Don’t try to memorize the details of this list. Know how to use some of them. FORENSIC ACCOUNTING - BA124 – Spring 2007 Slide 9-7

Interview Inhibitors • Time demands • Ego threats • Etiquette • Trauma • Forgetfulness • Time-line confusion • Logic confusion • Unconscious behaviors Unwilling Don’t try to memorize the details of this list. Know how to use some of them. Unable FORENSIC ACCOUNTING - BA124 – Spring 2007 Slide 9-8

Fraud Reporting • WFO Suggestion: • Summary • Chronology • Interview & Procedural Summaries • Admission information • Loss Assessment FORENSIC ACCOUNTING - BA124 – Spring 2007 Slide 9-9

Shenanigan #2-Recording Bogus Revenue • Technique #1: • Lack of economic substance • Technique #2: • Loans recorded as revenue • Technique #3: • Investment income as operating revenue • Technique #4: • Supplier rebates as future revenue • Technique #5: • Post merger deferred revenue FORENSIC ACCOUNTING - BA124 – Spring 2007 Slide 9-10