Download

1 / 23

330 likes | 747 Views

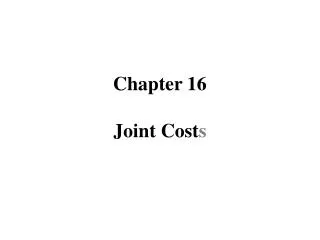

Chapter 16 Joint Cost s. Joint Products. Joint Costs. Final Sale. Separate Processing. Oil. Common Production Process. Joint Input. Final Sale. Gasoline. Separate Processing. Final Sale. Chemicals. Separable Product Costs. Split-Off Point.

E N D

Chapter 16 Joint Costs

Joint Products Joint Costs Final Sale Separate Processing Oil Common Production Process Joint Input Final Sale Gasoline Separate Processing Final Sale Chemicals Separable Product Costs Split-Off Point

Why Allocate Joint Costs? • to compute inventory cost and cost of goods sold • to determine cost reimbursement under contracts • for insurance settlement computations • for rate regulation • for litigation purposes

Joint Cost Allocation Methods • Market-Based – allocate using market-derived data (dollars): • Sales value at split-off • Net Realizable Value (NRV) • Constant Gross-Margin percentage NRV • Physical Measures – allocate using tangible attributes of the products, such as pounds, gallons, barrels, etc

An Example • Farmer’s Dairy purchases raw milk from individual farms and processes it until the split-off point, when two products – cream and liquid skim – emerge. These two products are sold to an independent company, which markets and distributes them to supermarkets • In May 2009, Farmer’s Dairy processes 110,000 gallons of raw milk. During processing, 10,000 gallons are lost due to evaporation, yielding 25,000 gallons of cream and 75,000 gallons of liquid skim. • Summary data follows:

Sales Value at Splitoff Method • Uses the sales value of the entire production of the accounting period to calculate the amount of allocation • Ignores inventories

Physical-Measure Method • Allocates joint costs to joint products on the basis of the relative weight, volume, or other physical measure at the split-off point of total production of the products • Let’s use number of gallons produced as the measure to allocate joint costs

Further Processing – Additional Data • Assume the same data as the base case except that both cream and liquid skim can be processed further • Cream is processed into Buttercream: 25,000 gallons of cream are further processed into 20,000 gallons of buttercream at additional processing costs of $280,000. Buttercream sells for $25 per gallon • Liquid Skim is processed into Condensed Milk: 75,000 gallons of liquid skim are further processed to yield 50,000 gallons of condensed milk at additional processing costs of $520,000. Condensed milk sells for $22 per gallon • Sales during May were 12,000 gallons of buttercream and 45,000 gallons of condensed milk.

Net Realizable Value (NRV) Method • Allocates joint costs to joint products on the basis of the relative NRV of total production of the joint products • NRV = Final Sales Value – Separable Costs

Constant Gross Margin NRV Method • Allocates joint costs to joint products in a way that forces the overall gross-margin percentage to be identical for the individual products • It is also based on total production • Joint Costs are calculated as a residual amount

Sell-or-Process Further Decisions • In Sell-or-Process Further decisions, joint costs are irrelevant since they are “sunk” costs at the decision point • Decision should be based on whether the incremental revenue due to further processing is greater/less than the separable costs for the same

Joint Products - Practice The wood spirits company produces two products, turpentine and methanol, by a joint process. Joint costs are $120,000 per batch of output. Each batch totals 10,000 gallons, 25% methanol and 75% turpentine. At split-off, methanol sells for $21/gallon and turpentine sells for $14/ gallon.

Joint Products - Practice (continued) The company has discovered an new process by which the methanol can be made into a pleasant-tasting beverage. The selling price for this beverage would be $40 per gallon. The additional processing would cost $12 per gallon s and the company would have to pay excise taxes of 20% on the selling price. Should the company undertake further processing?