ADJUSTING ENTRIES RECORDED FROM A WORK SHEET

190 likes | 450 Views

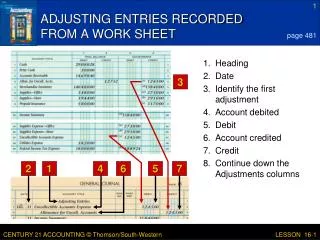

2. 1. 4. 6. 5. 7. ADJUSTING ENTRIES RECORDED FROM A WORK SHEET. page 481. 1. Heading. 2. Date. 3. 3. Identify the first adjustment. 4. Account debited. 5. Debit. 6. Account credited. 7. Credit. 8. Continue down the Adjustments columns.

ADJUSTING ENTRIES RECORDED FROM A WORK SHEET

E N D

Presentation Transcript

2 1 4 6 5 7 ADJUSTING ENTRIES RECORDED FROM A WORK SHEET page 481 1. Heading 2. Date 3 3. Identify the first adjustment 4. Account debited 5. Debit 6. Account credited 7. Credit 8. Continue down the Adjustments columns LESSON 16-1

ADJUSTING ENTRY FOR ALLOWANCE FOR UNCOLLECTIBLE ACCOUNTS page 482 LESSON 16-1

ADJUSTING ENTRY FOR MERCHANDISE INVENTORY page 482 LESSON 16-1

ADJUSTING ENTRY FOR SUPPLIES—OFFICE page 483 LESSON 16-1

ADJUSTING ENTRY FOR SUPPLIES—STORE page 483 LESSON 16-1

ADJUSTING ENTRY FOR PREPAID INSURANCE page 484 LESSON 16-1

ADJUSTING ENTRY FOR DEPRECIATION—OFFICE EQUIPMENT page 484 LESSON 16-1

ADJUSTING ENTRY FOR DEPRECIATION—STORE EQUIPMENT page 485 LESSON 16-1

ADJUSTING ENTRY FOR FEDERAL INCOME TAXES page 485 LESSON 16-1

THE INCOME SUMMARY ACCOUNT page 487 LESSON 16-2

3 3 CLOSING ENTRY FOR ACCOUNTS WITH CREDIT BALANCES page 488 1 2 4 1. Heading 3. Debits to close 2. Date 4. Credit to Income Summary LESSON 16-2

3 3 CLOSING ENTRY FOR INCOME STATEMENT ACCOUNTS WITH DEBIT BALANCES page 489 1. Date 2. Account debited 3. Credits to close 4. Debit amount 1 2 4 LESSON 16-2

Purchases Bal. 209,960.00 Closing 209,960.00 (New Bal. zero) Income Summary Adj. (mdse. inv.) 15,840.00 Closing (credit amounts) 500,253.10 Closing (debit accounts) 404,099.15 (New Bal. 80,313.95) SUMMARY OF CLOSING ENTRY FOR INCOME STATEMENT ACCOUNTS WITH DEBIT BALANCES page 490 LESSON 16-2

CLOSING ENTRY TO RECORD NET INCOME page 491 1 2 3 1. Date 2. Debit Income Summary 3. Credit Retained Earnings LESSON 16-2

CLOSING ENTRY FOR DIVIDENDS page 491 1 2 3 1. Date 2. Debit Retained Earnings 3. Credit Dividends LESSON 16-2

COMPLETED CLOSING ENTRIES FOR A CORPORATION RECORDED IN A JOURNAL page 492 LESSON 16-2

3 2 4 5 7 POST-CLOSING TRIAL BALANCE page 496 1. Heading 1 2. Accounts that have balances 3. Debit balances 4. Credit balances 5. Word Totals 6. Totals 7. Double lines 6 LESSON 16-3

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 497 1. Source documents are checked, and transactions are analyzed. 1 2 2. Transactions are recorded in journals. 3. Journal entries are posted to the accounts payable ledger, the accounts receivable ledger, and the general ledger. 3 4 5 4. Schedules of accounts payable and account receivable are prepared from the subsidiary ledgers. 5. A work sheet is prepared from the general ledger. (continued on next slide) LESSON 16-3

6. Financial statements are prepared. ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 497 7. Adjusting and closing entries are journalized from the work sheet. 9 8. Adjusting and closing entries are posted to the general ledger. 9. A post-closing trial balance of the general ledger is prepared. 8 7 6 (continued from previous slide) LESSON 16-3