Download

1 / 21

220 likes | 477 Views

Chapter 17: Intercorporate Equity Investments . Relevant circumstances Consolidation Pooling of interests Purchase method New entity approach Pro rata Equity method Fair value method Special Purpose Entity. Reporting on Intercorporate Equity Investments.

E N D

Chapter 17: Intercorporate Equity Investments • Relevant circumstances • Consolidation • Pooling of interests • Purchase method • New entity approach • Pro rata • Equity method • Fair value method • Special Purpose Entity

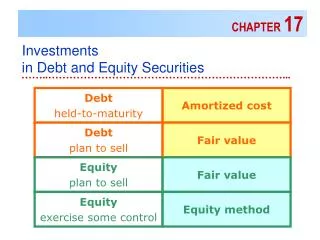

Reporting on Intercorporate Equity Investments • Consolidated reporting as if the two separate legal entities are one accounting entity using either the purchase or pooling method (as appropriate) • Nonconsolidation using the equity method of accounting • Nonconsolidation using the fair (market) value approaches

Finite Uniformity for Intercorporate Investments Ownership of Voting Stock Accounting Method >50% Consolidate per ARB 51 (SFAS No. 94) SFAS No. 141 and 142 20% to 50% Equity Accounting per APB Opinion No. 18 >20% Fair (market) value for both trading securities and available-for-sale securities...

Relevant Circumstances The relevant circumstances that justify differential accounting for intercorporate equity investments depend on the level of influence held by the investor

Three Levels of Control • Majority owned company: owner has effective control • Majority owned company: control is only temporary or the majority owner does not have effective control • Less-than-majority-owned companies: relevant circumstance is whether the investor can exercise significant influence over operating and financial policies

Consolidation • A technique in which two or more entities are reported as if they are one common accounting entity • Also called a business combination

Consolidation Terms • Combined enterprise • Constituent companies • Combinor • Combinee

Consolidation • Central accounting issue is the valuation of the assets and liabilities of the separate entities being combined for reporting purposes • FASB (1976) outlined three possible methods of accounting • pooling of interests accounting • purchase accounting • new entity approach

Divestitures • Sell-off • Spin-off • Split-off • Split-up

Pooling of Interests • Based on the premise that no substantive transaction occurs between the constituent companies • Is argued to be simply the formal unification of two previously separate ownership groups • Desirability of pooling is to avoid certain ramifications of purchase accounting

Purchase Method • Assumption is that the combinor is a parent company that purchases the combinee (subsidiary) and must account for the purchase as it would for the acquisition of any asset • The asset, investment in the combinee company, is recorded by the combinor at the latter’s cost determined as of the date the combination is consummated

New Entity Approach • Regard the combined enterprise as an entirely new entity • Results in the use of current values for the assets and liabilities of all the separate entities as of the date the combination is consummated

Pro Rata Consolidation ( 4th method) • Consolidation of assets and liabilities occurs only to the extent of the stock acquired by the parent • An arbitrary distinction at the 50 % point where control is assumed does not exist

Equity Method • Used whenever the investor has the ability to exercise significant influence over the investee • A one-line consolidation takes place • The investment account simply mirrors the net change in investee book value

Fair Value Method • Market value applies where no significant influence exists and market values are readily determinable for investments of approximately 20 percent or less • Increases or decreases in market value may or may not go through income depending upon management’s intention to sell them in the near term

SFAS No. 94 Asserts, rather than demonstrates, that consolidated reporting (and the fictional accounting entity thus created) is more relevant to investors than are separate entity statements in which the reporting entity is the legal entity

SFAS No. 142 • Goodwill is converted into an intangible asset • with an indefinite life • but it is subject to write-off as an expense if it becomes “impaired.” Tests of impairment must be made on an annual basis. • Impairment test after acquisition compares • (1) the fair market value of the acquisition against • (2) the historical cost of the net assets plus goodwill at an annual measurement date after acquisition. If (1) is greater than (2), no impairment has occurred. However, if (2) is greater than (1), goodwill is impaired and the impaired amount is written off as a loss appearing above income from continuing operations. • Impairment rules are generally going to generate soft numbers (low verifiability)

Special Purpose Entity (SPE) • A joint venture between a sponsoring company and a group of outside investors • SPE is limited by its charter to certain permitted activities. Hence, the term “special purpose” comes from the limited scope of the SPE. • Most common uses an SPE are • financing arrangements, • leasing arrangements, • and sales/transfers of illiquid or poor performing assets

Special Purpose Entity (SPE) • Hundreds of respected U.S. companies have an estimated $2 trillion of debt hidden in off-balance sheet subsidiaries such as SPEs. • In a recent survey, 29 percent of the 141 CFOs responding indicated that some of their company’s debt was not reflected on the balance sheet. 3% reported that more than 50% of the corporate debt was off balance sheet. • 42% of the companies that reported off balance sheet debt indicated that they guarantee or otherwise protect the investment of third parties in the SPEs, precisely the practice that led to Enron’s downfall and a practice that should lead to consolidation even though these companies report not consolidating the SPEs in question.

Enron • Enron’s sold poorly performing assets to LJMs • enabled Enron to move debt off its books and • to show inflated earnings and cash flow from the sale of assets to the SPEs which were controlled and run by Enron employees. • Enron’s “aggressive” accounting and the use of SPEs broke new ground to the extent in which structured finance arrangements can be used to manipulate reported financial

Chapter 17: Intercorporate Equity Investments • Relevant circumstances • Consolidation • Pooling of interests • Purchase method • New entity approach • Pro rata • Equity method • Fair value method • SPE