Download

1 / 38

390 likes | 641 Views

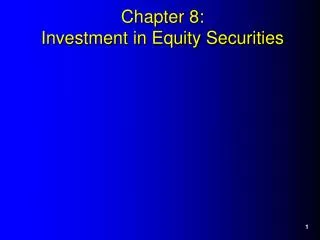

C H A P T E R. 12. Investments in Debt and Equity Securities. Learning Objective 1. Understand why companies invest in other companies. Insufficient cash (relieved by short-term borrowing). 1/1. 6/30. 12/31. Average Cash Needs. Excess cash (used for short- term investments).

E N D

C H A P T E R 12 Investments in Debt and Equity Securities

Learning Objective 1 Understand why companies invest in other companies.

Insufficient cash (relieved by short-term borrowing) 1/1 6/30 12/31 Average Cash Needs Excess cash (used for short- term investments) Actual Cash on Hand A Cash Flow Pattern Companies often need cash flow from sources other than their own operations because the company’s own cash flow might vary greatly over the course of a year.

What Are Some Other Reasons Companies Invest Their Excess Cash? • To earn a return. • Banks give a fixed return. • Investing in stocks or bonds of other companies may earn a higher rate of return (and demand a higher degree of risk). • The ability to ensure a supply of raw materials. • To influence a board of directors. • To diversify their product offerings. • Less expensive than R&D.

Learning Objective 2 Understand the different classifications for securities.

Define the Two Classifications for Securities. Debt Securities Financial instruments issued by a company that carry with them a promise of interest payments and the repayment of principal. Equity Securities (Stock) Shares of ownership in a corporation that can change significantly in value and that provide for a return to investors in the form of dividends.

Classifying Securities Investments Debt Equity

Held-to-Maturity Securities Equity Method Securities Classifying Securities—Matching Equity Method Securities Held-to-Maturity Securities Method used to account for an investment in the stock of another company when significant influence can be imposed (presumed when 20 to 50 percent of the outstanding voting stock is owned). Debt securities purchased by an investor with the intent of holding the securities until they mature.

Trading Securities Available-for-Sale Securities Classifying Securities—Matching Trading Securities Available-for-Sale Securities Debt and equity securities not classified as trading, held-to-maturity, or equity method securities. Debt and equity securities purchased with the intent of selling them should the need for cash arise or to realize short-term gains.

Investments Held-to- Maturity Trading Classifying Securities Debt Equity Available- for-Sale Equity Method

Classifying Securities Investments Debt Equity Held-to- Maturity Available- for-Sale Equity Method Trading

Reporting of Changes in FMV Classification Disclosed at Trading Available- for-Sale Held-to- Maturity Equity Method Classifying Securities— Fill in the Chart Fair value Fair value Amortized cost Cost adjusted for changes in net assets of investee Income statement Stockholders’ equity Not recognized Not recognized

Learning Objective 3 Account for the purchase, recognition of revenue, and sale of trading and available-for-sale securities.

Cost (including broker’s fees) Type Classification 1 Debt Trading $ 3,000 2 Equity Trading 15,500 3 Debt Available-for-sale 10,000 4 Equity Available-for-sale 7,300 Purchase of Securities Caribou Corp. purchased the following securities on January 1, 2003. Record the appropriate entry.

Cost (including broker’s fees) Type Classification 1 Debt Trading $ 3,000 2 Equity Trading 15,500 3 Debt Available-for-sale 10,000 4 Equity Available-for-sale 7,300 Investment in Trading Securities . . . . . . . . . . 18,500 Investment in Available-for-Sale Securities. . 17,300 Cash . . . . . . . . . . . . . . . . . . . . . . 35,800 Purchased debt and equity securities. Purchase of Securities

Security Interest Dividends 1 Debt $270 2 Equity $895 3 Debt 920 4 Equity 560 Cash. . . . . . . . . . . . . . . . . . . . . . . . . 2,645 Interest Revenue. . . . . . . . . . . . . 1,190 Dividend Revenue. . . . . . . . . . . . 1,455 Received interest and dividend revenues. Accounting for Return Earned on an Investment Buffalo Corp. earned the following return on their owned securities. Record the journal entry.

Cost (including broker’s fees) Type Classification 1 Debt Trading $ 3,000 2 Equity Trading 15,500 3 Debt Available-for-sale 10,000 4 Equity Available-for-sale 7,300 Cash. . . . . . . . . . . . . . . . . . . . . . . . . . . 17,000 Investment in Trading Securities. . . 15,500 Realized Gain on Sale of Securities 1,500 Sold Security 2 for $17,000. Accounting for the Sale of Securities Buffalo Corp. sold Security 2 for $17,000. The historical cost was $15,500.Record the entry.

What Are Realized Gains and Losses? Gains and losses resulting from the sale of securities in an arm’s-length transaction. At the end of the accounting period, any gain or loss on the sale of securities must be included on the income statement.

Learning Objective 4 Account for changes in the value of securities.

What Are Unrealized Gains and Losses? Gains and losses resulting from changes in the value of securities that are still being held.

Unrealized Loss on Trading Securities . . . 200 Market Adjustment, Trading Securities 200 Recorded market adjustment for trading securities. Accounting for Changes in Value — Trading Securities The following market values were recorded for Buffalo Corp.’s portfolio on December 31, 2003.Record the changes in the values of the securities. Historical Cost MarketValue12/31/03 Type 1 Trading $ 3,000 $ 2,800 3 Available-for-sale 10,000 10,500 4 Available-for-sale 7,300 9,250

Market Adjustment, Available-for-Sale Securities. 2,450 Unrealized Increase in Value of Available-for-Sale Securities . . . . 2,450 Recorded market adjustment for available-for-sale securities. Accounting for Changes in Value — Available-for-Sale Historical Cost Market Value 12/31/03 Type 1 Trading $ 3,000 $ 2,800 3 Available-for-sale 10,000 10,500 4 Available-for-sale 7,300 9,250

Historical Cost Market Value 12/31/04 Type Market Adjustment, Trading Securities. . . . 300 Unrealized Gain on Trading Securities . 300 Recorded market adjustment for trading security. Subsequent Changesin Value The following market values were recorded for Buffalo Corp.'s portfolio on December 31, 2004. Record the subsequent change in the trading security. 1 Trading $ 3,000 $ 3,100 3 Available-for-sale 10,000 10,300 4 Available-for-sale 7,300 9,500

Expanded Material Learning Objective 5 Account for held-to-maturity securities.

Example: Initial Purchase of Held-to-Maturity Securities The Moose Company purchased a 5-year, $500,000 bond and received interest payments of 10 percent, payable semiannually. Assume the effective rate is 12 percent.Record the investment. 1. Semiannual interest payments $ 25,000 Present value of interest annuity $184,002 2. Principal of bonds $500,000 Present value of bonds 279,197 3. Present value of investment $463,199

Investment in Held-to-Maturity Securities. . . . . . . . . . . . . . . . . . . . . 463,199 Cash. . . . . . . . . . . . . . . . . . . . . 463,199 Purchased a $500,000 bond as an investment. Example: Initial Purchase of Held-to-Maturity Securities 1. Semiannual interest payments $ 25,000 Present value of interest annuity $184,002 2. Principal of bonds $500,000 Present value of bonds 279,197 3. Present value of investment $463,199

Investment in Held-to-Maturity Security. . . . . . . . . . . . . . . . . . . . . 463,199 Bond Interest Receivable . . . . . . . . 16,667 Cash. . . . . . . . . . . . . . . . . . . . . . 479,866 Purchased a $500,000 bond as an investment and paid four months’ accrued interest. Bonds PurchasedBetween Interest Dates Assume the bond purchased by the Moose Company paid interest on July 1 and January 1 of each year. If the Moose Company purchased the bond on April 31, 2003, how will the purchase be recorded?

Accounting for Amortization of Premiums and Discounts. Define. Straight-Line Amortization A method of systematically writing off a bond discount or premium in equal amounts each period until maturity. Effective-Interest Amortization A method of systematically writing off a bond premium or discount that takes into consideration the time value of money and results in an equal rate of amortization for each period.

Cash. . . . . . . . . . . . . . . . . . . . . . . . 600.00 Investment in Held-to-Maturity Securities. . . . . . . . . . . . . . . . . . . . 134.20 Bond Interest Revenue . . . . . . 734.20 Received bond interest and amortized discount. Straight-Line Amortization The Rhinoceros Company purchased a 12 percent, 5-year, $10,000 bond for $8,658 on the issuance date. The interest payments are made semiannually.Using the straight-line method, record the first interest payment received.

Hint: Won’t you need an amortization table? Effective-Interest Amortization The Rhinoceros Company purchased a 12 percent, 5-year, $10,000 bond for $8,658 on the issuance date. The interest payments are made semiannually and the market rate is 16 percent.Using the effective-interest method, record the first interest payment received.

Effective-Interest Amortization Cash Interest Amortized Investment Payment Received Earned Amount Balance (0.16 x 0.5 x Balance) $ 8,658 1 $600 $693 $ 93 8,751 2 600 700 100 8,851 3 600 708 108 8,959 4 600 717 117 9,076 5 600 726 126 9,202 6 600 736 136 9,338 7 600 747 147 9,485 8 600 759 159 9,644 9 600 772 172 9,816 10 600 784 184 10,000

Cash. . . . . . . . . . . . . . . . . . . . . . . . 600 Investment in Held-to-Maturity Securities. . . . . . . . . . . . . . . . . . . . 93 Bond Interest Revenue . . . . . . . 693 Received bond interest and amortized discount. Effective-Interest Amortization The Rhinoceros Company purchased a 12 percent, 5-year, $10,000 bond for $8,658 on the issuance date. The interest payments are made semiannually and the market rate is 16 percent.Using the effective-interest method, record the first interest payment received.

Cash. . . . . . . . . . . . . . . . . . . . . . . . 10,000 Investment in Held-to-Maturity Securities. . . . . . . . . . . . . . . . . 10,000 Received the principal of bond at maturity. Sale or Maturity of Bonds The Rhinoceros Company holds the bond until maturity.Record the entry for the receipt of the bond principal.

Cash. . . . . . . . . . . . . . . . . . . . . . . . 9,900 Gain on Sale of Bond. . . . . . . . 100 Investment in Held-to-Maturity Securities. . . . . . . . . . . . . . . . . . 9,800 Sold bond for $9,900. Sale or Maturity of Bonds What journal entry is required if the Rhinoceros Company sells the bond for $9,900 before maturity when the balance in the bond account is $9,800?

Expanded Material Learning Objective 6 Account for securities using the equity method.

Available-for-Sale Method Investment in Available-for-Sale Securities . . . . . . . . . . . . . . . . . . . . . . . 200 Cash. . . . . . . . . . . . . . . . . . . . . . . . 200 Equity Method Investment in Equity Method Securities 200 Cash. . . . . . . . . . . . . . . . . . . . . . . . 200 Illustrating the Equity Method Brown Tree Co. purchased 100 shares of Koala Corp. common shares at $2 per share, representing a 20 percent ownership in the company. Record Brown Tree’s transactions using both the available-for-sale method and the equity method.

Brown Tree Co. purchased 100 shares of Koala Corp. common shares at $2 per share, representing a 20 percent ownership in the company. Record the $0.80 per share dividend. Available-for-Sale Method Cash . . . . . . . . . . . . . . . . . . . . . . . . . . 80 Dividend Revenue . . . . . . . . . . . . . 80 Equity Method Cash. . . . . . . . . . . . . . . . . . . . . . . . . . . 80 Investment in Equity Method Securities. . . . . . . . . . . . . . . . . . . 80 Illustrating the Equity Method

Available-for-Sale Method No entry. Equity Method Investment in Equity Method Securities. 2,000 Revenue from Investments. . . . . . . . 2,000 Illustrating the Equity Method Brown Tree Co. purchased 100 shares of Koala Corp. common shares at $2 per share, representing a 20 percent ownership in the company. Koala Corp. announces a $10,000 earnings for the year. Record the appropriate entries.