Download

1 / 0

0 likes | 234 Views

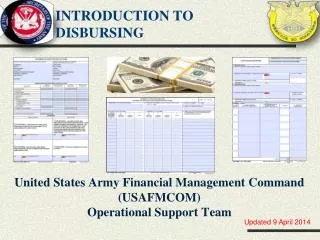

Manual Disbursing Operations. AGENDA. Introduction and References Disbursing Chain of Command and Personnel roles/responsibilities Pecuniary Liability and Cash handling Advance DD 1081 . AGENDA (cont.). Cashier and Disbursing Agent transactions - Disbursements

E N D