Download

1 / 12

120 likes | 280 Views

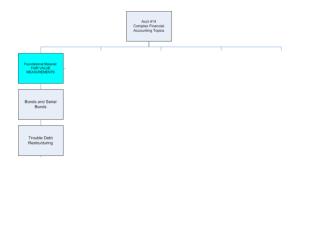

Loan Impairments & Troubled Debts. Sequence of Events. Debtor & creditor enter a debt arrangement. Creditor. Debtor. Loan Origination. Debtor encounters difficulty. Estimate Loss. Poor Debt Management. This is a loan impairment. Loan Impairment. Creditor realizes

E N D

Loan Impairments & Troubled Debts Sequence of Events

Debtor & creditor enter a debt arrangement Creditor Debtor Loan Origination Debtor encounters difficulty Estimate Loss Poor Debt Management This is a loan impairment Loan Impairment Creditor realizes difficulty & estimates loss Estimate Effect Insolvency (Unable to Service Debt) Later, the debtor becomes insolvent Modification of Terms Creditor & debtor agree to a modification of terms

Creditor Debtor Loan Origination Estimate Loss Poor Debt Management Loan Impairment Estimate Effect Insolvency (Unable to Service Debt) Modification of Terms Bankruptcy Economic Recovery With altered agreement, maybe the debtor will make it & maybe not ?

Assets/Equity used to settle debt Debt Terms Modified Concessions Granted to Debtor • Troubled debt restructure provides for concession to debtor by creditor: • Transfer of assets or equity shares to settle all or part of debt • Modification of terms of debt

Concessions Granted to Debtor Assets/Equity used to settle debt Debt Terms Modified Creditor Debtor Loss equal to difference between carrying value of receivable and fair market value of compensation received. When assets or equity are used to settle debt, there are effects on debtor and creditor Creditors record ordinary loss (or charge allowance account) for difference between carrying value of debt and fair market value of asset received.

Concessions Granted to Debtor Assets/Equity used to settle debt Debt Terms Modified Creditor Debtor Gain on debt restructure equal to difference between book value of debt and FMV of compensation given. Loss equal to difference between carrying value of receivable and fair market value of compensation received. Book gain or loss on difference between book value and FMV of assets given. No gain or loss for securities Debtors will recognize a gain. Value of assets surrendered in satisfaction of debt will be less than carrying value of debt. That is nature of concession Debtors must first update their books to reflect the fair value of assets surrendered

Concessions Granted to Debtor Debt Terms Modified Book value of debt < restructured cash flows? YES NO Low interest rate 0% interest Another concession often granted to debtors involves renegotiation of amounts due to creditor. The modification of debt terms results in a restructure of future cash flows. Debtor recognizes gain on difference between book value of debt and restructured cash flows. No interest expense. No gain is recognized by debtor. Debtor finds implicit rate that equates cash flows with book value of debt. Can result in low or zero rate of interest on debt.

Concessions Granted to Debtor Assets/Equity used to settle debt Debt Terms Modified Book value of debt < restructured cash flows? Creditor Debtor YES NO Loss equal to difference between carrying value of receivable and fair market value of compensation received. Gain on debt restructure is equal to difference between book value of debt and FMV of compensation given. No gain is recognized. Debtor finds implicit rate that equates cash flows with book value of debt and recognizes interest expense. Debtor recognizes gain on difference between book value of debt and restructured cash flows. No interest expense. First book gain or loss on difference between book value and FMV of assets given. No gain or loss for securities Accounting for Troubled Debt Restructuring Prepared by Jeff Harkins, edited by T Gordon

Creditor Accounting • Modification of terms is indication of impairment of debt • Creditor will follow basic rules for debt impairment (FAS114 & FAS118) • Only difference from non-troubled debt situation: • The creditor will disclose any commitments to loan a “troubled debtor” additional funds

Are assets or an ownership interest transferred from debtor to creditor in settlement of debt? When the debt is settled, debtor and creditor accounting is basically parallel. No For a modification of terms, the creditor will generally recognize a LARGER loss (in comparison to gain recorded by debtor) because the creditor uses the original “historic” interest rate implicit in the loan. Is entity the creditor? Yes Discount cash flows to be received under modified terms using original interest rate Difference between carrying value of receivable and present value is ordinary loss for creditor

Are assets or an ownership interest transferred from debtor to creditor in settlement of debt? No Is entity the creditor? Yes Discount cash flows to be received under modified terms using original interest rate Difference between carrying value of receivable and present value is ordinary loss for creditor Is the debt settled In full?? Record ordinary gain or loss on asset. Difference between fair value of asset or equity interest and amount due on debt is a gain for debtor and ordinary loss for creditor Yes Yes No Record ordinary gain or loss on asset. Difference between fair value of asset or equity interest and amount due on debt is ordinary gain for debtor and ordinary loss for creditor No The difference between carrying value of debt and total future cash flows is recorded as an ordinary gain for debtor. No interest expense will be recorded in future years. Are cash flows to be made under the modified terms greater than the carrying value of the debt after transfer of asset or equity interest? No No gain is recorded by debtor. Find interest rate to equate cash flows to carrying value of debt. Use this interest rate to amortize restructured debt over its term Yes Troubled Debt Restructuring After FAS 145