Download

1 / 13

140 likes | 303 Views

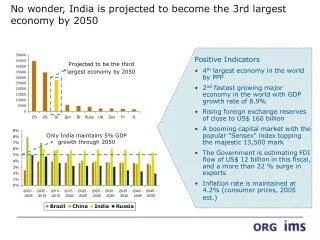

No wonder, India is projected to become the 3rd largest economy by 2050. Positive Indicators 4 th largest economy in the world by PPP 2 nd fastest growing major economy in the world with GDP growth rate of 8.9% Rising foreign exchange reserves of close to US$ 166 billion

E N D

No wonder, India is projected to become the 3rd largest economy by 2050 Positive Indicators • 4th largest economy in the world by PPP • 2nd fastest growing major economy in the world with GDP growth rate of 8.9% • Rising foreign exchange reserves of close to US$ 166 billion • A booming capital market with the popular "Sensex" index topping the majestic 13,500 mark • The Government is estimating FDI flow of US$ 12 billion in this fiscal, and a more than 22 % surge in exports • Inflation rate is maintained at 4.2% (consumer prices, 2005 est.) Projected to be the third largest economy by 2050 Only India maintains 5% GDP growth through 2050 Source: BRICs Potential

All of these make us believe that the pharmaceutical market would also benefit from this rapid growth and reforms, projected to grow at 11-13%* over next 3-5 years… • Population dynamics • Large population base 1.5 Bn by 2050 • Increasing Life expectancy at birth (age in years) currently at 65 and projected to go up to 69 by 2020. • Geriatric population to double over next 15 years • Increasing capacity to spend • Literacy rate at 65-70% and estimated to be close to 95% by 2020. • Huge middle class with vigorous buying capacity - 450 mio • Opening up of reimbursement avenues • Wave of shopping malls, credit uptake • High disease prevalence • Fastest growing diabetes population • AIDS, Oncology and other chronic ailments growing in numbers • Awareness and detection levels are improving • Changing healthcare model • Major pharma and insurance cos now in India • Disease specific insurance plans in place • Medical tourism growing by 20% YoY • Corporatisation of hospitals and pharmacies • Move to more scientific methods of promotion • New distribution channels • Increased healthcare access • Current access ~40-50%; govt. committed to take it to 80% in next 15-20 years • Improving access and growth rates in rural India • Hospital market growing rapidly, ~30-40% QoQ • OTC market grew at more than 7-8% in 2005, projected to grow at 10% over the next few years *Revised IMS Prognosis 2006

At $6 Billion on retail, the industry recorded a value growth of 18%, far higher than previous year Size & Growth Growth Contributors A change in trend,new introductions with 2% have dropped,while price increases contributed 1% with volume growth at 16% Therapy Split Acute therapy dominates the market with a value contribution of over 77%. Chronic segment has also registered a healthy growth of 18% against 19% of acute Indian Vs MNC Indian companies still dominate the market with a share of ~80%, have been capitalizing the pre-IPR advantage Doctors Currently General Practitioners (GPs) dominate the market, however the trend begins to favor physicians and specialists Patient Population Geriatric population is on the rise in the country, but ~ 40% of the population is also below 14 years of age** …and the current trends in the IPM clearly reflect the upbeat mood in the economy Source : Stockist Secondary Audit, Nov 06 MAT, WHO reports**

Healthcare segment in India is at the beginning of the evolution curve at the moment ..with large opportunities • Current healthcare access is at 30%; govt. committed to take it to 80% in next 15-20 years • Healthcare spending in India which is currently at 5.3% of GDP is expected to rise to 8% by 2012 • Majority source of healthcare spending is Private Sources of Healthcare Spending (Public vs. Private %) Source: WHO, IBEF, CII, OPPI

All of these make us believe that the pharmaceutical market would also benefit from this rapid growth and reforms, projected to grow at 11-13%* over next 3-5 years… • Population dynamics • Large population base 1.5 Bn by 2050 • Geriatric population to double over next 15 years • High disease prevalence • Fastest growing diabetes population • AIDS, Oncology and other chronic ailments growing • Increased healthcare access • Current access ~40-50%; govt. committed to take it to 80% in 15-20 years • Improving access and growth rates in rural India • Increasing capacity to spend • Huge middle class with vigorous buying capacity • Opening up of reimbursement avenues • Changing healthcare model • Medical tourism growing by 20% • Corporatisation of hospitals and pharmacies • New distribution channels *Revised IMS Prognosis 2006

Indian Pharmaceutical Industry • Globally Indian Pharma Industry ranks 4th in volume and 14th in value • Highly fragmented with 5,000+ units • Only 289 companies tracked (ORG – IMS) with sales of USD 4.1 bn in 2003 • 28 MNCs account for ~ 22% (USD 961 mio) of Pharma market • Prices controlled but gradually de-regulated from 347 in 1979 to 74 at present • World class manufacturing facilities : over 70 US FDA approved facilities – largest number outside of USA over 350 APIs manufactured from basic stage exports of APIs USD 700 million • Emergence of world class CRO facilities

The Indian Market has grown at a CAGR of 7.6% and is projected to reach ~US$8 billion by 2010 • Retail pharmaceutical sales • US$ billion CAGR = 9-11% • 7.7-8.5 CAGR = 7.6% • 4.6 • 4.2 • 3.7 • 3.4 • 3.5 • 2000 • 2001 • 2002 • 2003 • 2004 • 2010 estimated size Source: IMS; McKinsey analysis

Market Has Three Key Segments and is Dominated by Branded Generics • Segment • Description • Examples • Market segments • OTC • Non prescription, self-medication products sold directly to consumers with high emphasis on safety • Can be sold through non-chemist outlets such as kirana stores etc • Usually involves high advertising costs • Crocin, • Benadryl • Per cent • 100% = US$ 4.6 billion • OTC • 8-10 • Generic- • generics • 7-8 • Generic- • generics • Prescription only products but sold under the generic/ chemical name • Usually sold at high discount to the branded version • Sold through push by chemists who get much higher margins on unbranded products • Ranitidine • Amoxycillin • Ethicals • (Rx) • Branded generics • 82-85 • 2004 • Branded generics • Prescription only products sold under brand names • Sales force of pharmacos generate demand through detailing/ other promos to doctors • Ciplox (Ciprofolxacin) • Cardace (Ramipril) Source: IMS retail audit, web searches

Four Forces are Shaping the Indian Pharma Market • Market tiering and increase in share of specialty TAs • Undifferentiated mass market dominated by AI and GI moving towards a 4 tier market • Increase in relative share of specialty TAs driven by greater prevalence of chronic diseases • Growing competition from MNCs • IP changes • Current competitive landscape is dominated by local players with only 4 MNCs in top 15 • However, key market trends favour MNCs – as a result incumbents are increasing focus while absentees are evaluating entry • Market in transition: product patent bill passed in March ’05 after decades of process patents only • Patent infrastructure gearing up substantially to drive compliance 1 4 2 • Fundamental shifts in Indian pharmaceutical market 3 • Pricing • Historically low prices due to intense competition, government control and self pay market • Possible to command higher prices through differentiated products and superior marketing skills • Uncertainty around price control although number of drugs under DPCO has steadily declined

National Pharmaceuticals Policy 2006 • To ensure availability of good quality medicines at reasonable prices • To improve access particularly to the poor • To increase investment in manufacturing • To promote greater research & development by providing incentives • To enable domestic companies to become internationally competitive • To increase exports • To develop India as the preferred global destination for Pharmaceutical R&D and manufacturing

National Pharmaceuticals Policy 2006 • Over the past 25 years price control has been reduced from 400 to only 74 drugs. • New Policy recommends basket of 354 National List of Essential Medicines to be used for Price Control criteria, in addition to current 74 • Industry opposed to increase in price control - Industry suggests price monitoring v/s. cost based price control

The Country will Reap Enormous Benefits through R&D Growth in the Pharmaceutical Industry • Build India Inc. as a brand • Prove India’s ability to participate in the knowledge intensive industry • Make India a hub for global research • Benefit the economy & industry • Create good health for all • Create high-value jobs in research, manufacturing, and sales and marketing • Increase inflow of export earnings and FDI • Create a vibrant and internationally recognised industry • Increase access to medicine for the mass population • Provide access to superior products and India-specific treatments developed by MNCs and local companies

… India poised to be among the Top 10 players in the Global Pharmaceutical market by 2010 INDIA An Emerging Knowledge Superpower