Download

1 / 13

130 likes | 266 Views

“ Financial Possibilities of a Client – Electronic Payments and Financial Services ”. 20.10.2010 Assist. Prof. Kemal Kozarić , Ph.D. Cash Management in the CBBH. The process of management of KM cash is one of the most risky operations of the central bank

E N D

“Financial Possibilities of a Client – Electronic Payments and Financial Services” 20.10.2010 Assist. Prof. Kemal Kozarić, Ph.D.

Cash Management in the CBBH • The process of management of KM cash is one of the most risky operations of the central bank • The objective is to regularly supply economy with KM cash which is the legal tender in BH • The Central Bank has a monopoly on the process of production of KM cash, its putting into circulation, withdrawal and destruction (articles 39, 43 and 44 of the CBBH Law) • Putting and withdrawing KM cash in/from circulation is performed by the central bank through commercial banks which hold their reserve accounts opened in the CBBH books • The mentioned activities are done in accordance with the currency board as the applicable arrangement of monetary policy in BH

Cash Management Risk • Reputational risks in cash management: • Interruption in supply of economy with KM cash • Inadequate level of protection of KM banknotes during printing which makes possible the production of “good quality” counterfeits • The quality of counterfeits made so far is at a very low level • Slow, i.e. insufficiently fast withdrawal of banknotes unfit for circulation which affects the decrease of the quality of currency in circulation • App. 30% of banknotes received by the CBBH from commercial banks is classified as unfit for circulation

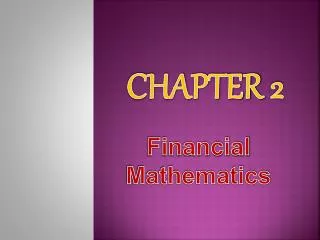

Trend of the Currency in Circulation for 2008, 2009 and 2010 (in KM millions)

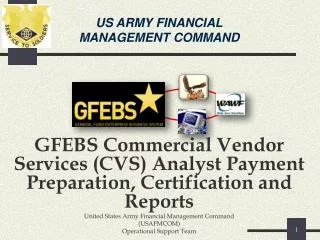

Share of the Value of some Denominations of Banknotes in Circulation 31.12.2009

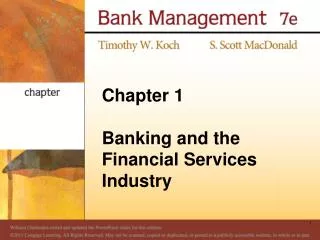

Trend of the Quantity of Counterfeits in the Period 2004 - 2009

Continuous Work on the Increase of Security • Protection from counterfeits : • Three levels of known security features • Education of staff in vaults and at bank windows • Education of people working in places with high frequency of cash payments (post offices, shopping centres...) • Education of citizens – information campaigns of the CBBH, web site of the CBBH (interactive animations with security features of all banknotes) • Promotion of non-cash payments – card operations and e-banking • Security of cash transport: • Insisting on raising the level of standards in the protection of cash transports and implementation of these standards • To introduce the best quality technologies– satellite surveillance, cryptoprotection ... • To use the possibilites of electronic inter-bank money market platform

Non-cash Payments: • Card operations • 26 banks offer these services • 1.75 million of issued cards (31.12.2009), increase of 140,000 cards compared to the end of 2008. • The highest number of debit cards (VISA and MAESTRO) • 2009: 1,355 ATMs, 16,259 POSs, while in 2008 there were 901 ATMsand 15,968 POSs • KM 4.9 billion realized in 2009, increase of 24% compared to the previous year • 74% ATMs : 26% POSs • POS: 49% cash 51% payment of goods and services (around KM 1.3 billion) • In 2009 the number of issued cards increased by 142,002 compared to 2008.

Non-cash payments: • Card operations • The average value of transaction is around KM 141 • The annual average value of transaction in 2009 amounted to KM 2,779 KM • On ATMsand POSs abroad, KM 210 million was realized by means of cards from BH (payment of goods and services KM 116 million, the remaining part applies to cash) • On ATMsand POSs in BH, KM 697 million was realized by means of cards from other countries (payment of goods and services KM 138 million, the remaining part applies to cash) • The data show a low level of penetration of this service on the market – most of transactions come down to collecting cash

Risks of Non-cash Payments • Counterfeiting of cards; • “Scanning” of cards and stealing of PINs • Inadequate education of users – subject to mistakes in performing transactions and subject to fraud and misuse • Poor average standard of citizens has a negative effect on the penetretation of services • The problem of poor transparency of commercial banks when presenting costs of services • Clients avoid such services with good reasons – lack of information and banks not offering sufficent user education

Advantages of Non-cash Payments • Your money is with you 24-7 • Easier keeping of money • Easier use in foreign countries (no need for conversions and exchanges in exchange offices) • Increased safety– more difficult to counterfeit, cards and tokens can be blocked in case they are stolen • Indirectly increases the duration of cash in circulation