Download

1 / 8

120 likes | 447 Views

Learn about Net Assets Approach and Balancing Figure Approach to prepare financial statements from incomplete records. Understand Mark Up and Margin concepts in the process.

E N D

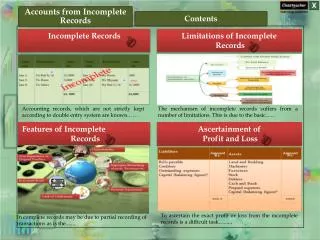

Where the accountant has to create a set of Financial Statements from Incomplete Records • 3 situations giving rise to Incomplete Records • No Accounting records kept at all for the Year in Question (Net Assets approach will be used – Accounting Equation!!) • Some Accounting information is Missing (Balancing Figure Approach will be used – T Account) • Records have been lost due to fire or flood – Accountant to prepare FS from whatever is left

2 Main Approaches • Net Assets Approach (i.e. Accounting Equation Approach) • Balancing Figure Approach (T Account Approach) – This is the method that students should be most familiar with for exam questions

Net Assets Approach • Use of Accounting Equation to Determine figure for Opening/Closing Capital; Drawings; Profit/Loss for the Year • Assets = Capital + Liabilities

The Balancing Figure (Double Entry/T A/c ) Approach • The Balancing figure approach uses ledger accounts to determine the incomplete information as detailed below • Receivables T Account – Credit Sales; Money Received • Payables T Account – Credit Purchases; Money Paid • Cash at Bank T A/C – Drawings, Money Stolen • Cash in Hand T A/c – Cash Sales, Cash Stolen • The process involves setting up a T Account and inserting the information that we have in the question to determine the missing figures

Mark Up & Margin Summary Both Mark Up & Margin involve expressing profit against • “Cost” for Mark Up • “Selling Price” for Margin So a product that sells for €20, costs €16 to produce and makes a profit of €4….the mark up is 25% (€4/€16) and the margin is 20% (€4/€20)

Margin & Mark Up Concepts • A margin is calculated on Selling Price (i.e. Selling Price is 100%) – • A Mark up is calculated on Cost (i.e. Cost is 100%) -

To Find Margin when Mark up is Known and Vice Versa, • Mark Up is Known – How to Find the Margin? • Add One to the Denominator (number beneath the Line) • Margin is Known – How to find the Mark Up? • Subtract One from the Denominator (number beneath the line)