Download

1 / 10

100 likes | 128 Views

Learn about adjustments recorded on a work sheet to update general ledger accounts at the end of a fiscal period. Examples include supplies and prepaid insurance. Understand the purpose of adjustments and how they bring accounts up to date.

E N D

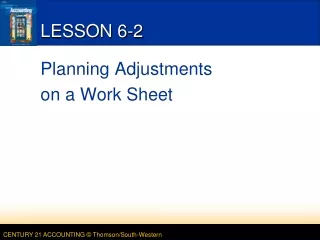

LESSON 6-2 Planning Adjustments on a Work Sheet

Adjustments • Def – changes recorded on a work sheet to update general ledger accounts at the end of a fiscal period. • Examples: Supplies & Prepaid Insurance • Purpose – to bring accounts up to date because assets have been “used” to earn revenue • Once used assets become expenses – Supplies Expense & Insurance Expense • GAAP – Matching Revenue with Expenses LESSON 6-2

3 SUPPLIES ADJUSTMENT ON A WORK SHEET page 158 2 1 1. Write the debit amount. 2. Write the credit amount. 3. Label the two parts of this adjustment. LESSON 6-2

3 PREPAID INSURANCE ADJUSTMENT ON A WORK SHEET page 159 2 1 1. Write the debit amount. 2. Write the credit amount. 3. Label the two parts of this adjustment. LESSON 6-2

1 2 3 PROVING THE ADJUSTMENTS COLUMNS OF A WORK SHEET page 160 1. Rule a single line. 2. Add both the Adjustments Debit and Credit columns. Write each column’s total. 3. Rule double lines. LESSON 6-2

1 LESSON 6-2

6 10000 102500 120000 10000 31000 110000 (a) 71500 (b) 10000 20000 5000 500000 20000 5000 500000 3 62500 4 62500 356500 356500 21300 21300 (b) 10000 10000 2800 30000 7 2800 30000 (a) 71500 5 71500 11000 11000 8 9 1 2 496400 10000 15000 496400 10000 15000 881500 881500 81500 81500 146600 356500 734900 525000 Net Income 209900 209900 356500 356500 734900 734900 LESSON 6-2

COMPLETING A WORK SHEET page 160 C STEPS: 1. Write the heading. 2. Record the trial balance. 3. Record the supplies adjustment. 4. Record the prepaid insurance adjustment. 5. Prove the Adjustments columns. 6. Extend all balance sheet account balances. 7. Extend all income statement account balances. 8. Calculate and record the net income (or net loss). 9. Total and rule the Income Statement and Balance Sheet columns. LESSON 6-2

TERMS adjustments HELPFUL HINTS Amount of net income or net loss – MUST = Always add the amount of net income or net loss to the appropriate column so final totals = Net Income – capital is greater than expenses Net Loss – expenses are greater than capital TERM REVIEW & HELPFUL HINTS page 161 LESSON 6-2