Download

1 / 6

60 likes | 82 Views

Learn how to detect and prevent cash theft in your company through auditing procedures and establishing internal controls. Discover audit techniques to uncover fraudulent activities and safeguard your finances effectively.

E N D

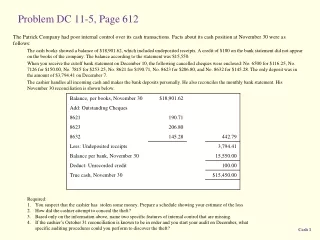

Problem DC 11-5, Page 612 Required: You suspect that the cashier has stolen some money. Prepare a schedule showing your estimate of the loss How did the cashier attempt to conceal the theft? Based only on the information above, name two specific features of internal control that are missing. If the cashier’s October 31 reconciliation is known to be in order and you start your audit on December, what specific auditing procedures could you perform to discover the theft? The Patrick Company had poor internal control over its cash transactions. Facts about its cash position at November 30 were as follows: The cash books showed a balance of $18,901.62, which included undeposited receipts. A credit of $100 on the bank statement did not appear on the books of the company. The balance according to the statement was $15,550. When you receive the cutoff bank statement on December 10, the following cancelled cheques were enclosed: No. 6500 for $116.25, No. 7126 for $150.00, No. 7815 for $253.25, No. 8621 for $190.71, No. 8623 for $206.80, and No. 8632 for $145.28. The only deposit was in the amount of $3,794.41 on December 7. The cashier handles all incoming cash and makes the bank deposits personally. He also reconciles the monthly bank statement. His November 30 reconciliation is shown below.

The minimum amount of the theft is $719.50 if the cash reported as “undeposited receipts” ($3,794.41) was actually on hand, represented November receipts, and was deposited intact in December. If the $3,794.41 was not available to deposit or represented December receipts, the maximum loss could be $4,513.91 (719.50 + 3,794.41) for November. Such a shortage (minimum or maximum) for November and the attempt to conceal the shortage would alert the auditors to examine the bank reconciliations throughout the year for other concealed shortages. b. He attempted to conceal his theft by: 1. Not listing all outstanding cheques. 2. Miscalculating the outstanding cheques shown on the reconciliation. 3. Subtracting an item from the bank balance that should be added to book balance. c. No one other than the cashier is responsible for tracing cash receipts to the deposits in the bank. The cashier is also responsible for preparing the bank reconciliation.

The following auditing procedures on December 5 would uncover the theft if the October 31 reconciliation is known to be correct: 1. Compare cheques returned since October 31 with cheques outstanding at that time and with cheque register for November in order to ascertain outstanding cheques. 2. Trace cash on hand at October 31 as well as receipts during November to deposits in bank, ascertaining undeposited cash at November 30. 3. Count cash on hand on December 5, and by adding deposits since November 30 and subtracting receipts since November 30 to develop cash on hand at November 30. 4. Compare adjusted cash on hand developed in count (Step 3) with undeposited cash ascertained in tracing (Step 2).

Problem 17-22, Page 541 The following are fraud and other irregularities that might be found in the client’s year-end cash balance. (Assume the balance sheet date is June 30.) • A cheque was omitted from the outstanding cheque list on the June 30 bank reconciliation. It cleared the bank July 7. • A cheque was omitted from the outstanding cheque list on the bank reconciliation. It cleared the bank September 6. • Cash receipts collected on accounts receivable from July 2 to July 5 were included as June 29 and June 30 cash receipts. • A loan from the bank on June 26 was credited directly to the client’s bank account. The loan was not entered in the books as of June 30. • A cheque that was dated June 26 and disbursed in June was not recorded in the cash disbursements journal, but it was included as an outstanding cheque on June 30. • A bank transfer recorded in the accounting records on July 2 was included as a deposit in transit on June 30. • The outstanding cheques on the June 30 bank reconciliation were underfooted by $2000. REQUIRED • Assuming that each of these misstatements was intentional, state the most likely motivation of the person responsible. • What control could be instituted for each intentional misstatement to reduce the likelihood of errors. • List an audit procedure that could be used to discover each misstatement.