Download

1 / 15

150 likes | 421 Views

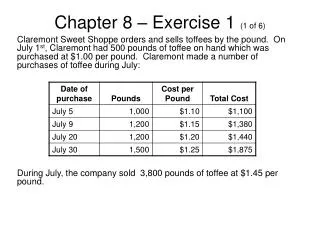

Chapter 8 – Exercise 1 (1 of 6). Claremont Sweet Shoppe orders and sells toffees by the pound. On July 1 st , Claremont had 500 pounds of toffee on hand which was purchased at $1.00 per pound. Claremont made a number of purchases of toffee during July:.

E N D

Chapter 8 – Exercise 1 (1 of 6) Claremont Sweet Shoppe orders and sells toffees by the pound. On July 1st, Claremont had 500 pounds of toffee on hand which was purchased at $1.00 per pound. Claremont made a number of purchases of toffee during July: During July, the company sold 3,800 pounds of toffee at $1.45 per pound.

Chapter 8 – Exercise 1 (2 of 6) Part A: Compute the number of pounds of toffee on hand on July 31st, and the cost of goods available for sale for the month of July. SOLUTION: Take info from previous slide, and copy it out. Beginning Inventry Purchases Jul 5 1,000 1,100 Jul 9 1,200 1,380 Jul 20 1,200 1,440 Jul 30 1,500 1,875 4,900 5,795 Goods available for sales 5,400 6,295 Less: Pounds sold 3,800 End Inventory 1,600

Chapter 8 – Exercise 1 (3 of 6) Part B: Assume that the company uses the weighted-average inventory method. Compute its ending inventory on July 31st, the cost of goods sold during July, and the company’s gross profit during July. SOLUTION: Weighted average unit cost Weight average = goods available for sale / # units available for sale = 6,295 / 5,400 = 1.1657 is the average all year long Ending inventory = 1600 @1.1657 = 1,865 Cost of goods sold = 3,800 @ 1.1657 = 4,430 Note: 1,865 + 4,430 = 6295 (goods available for sale) Sales(3,800 @ 1.45) 5,510 Goods available for sale (Part A) 6,295 Less: ending invetnroy 1,865 Cost of goods sold 44………..

Chapter 8 – Exercise 1 (4 of 6) Part C: Assume that the company uses FIFO. Compute its ending inventory on July 31st, the cost of goods sold during July, and the company’s gross profit during July. SOLUTION: Calculation of ending inventory (1,600 poounds) from july 30 purchases (1,50 @1.25) 1,875 from July 20 purchases(100 @1.2) 120 1,995 Sales(3,800 @1.45) 5,510 Goods available for sale (Part A) 6,285 Less ending inv. 1995 Cost of goods sold 4,300 Gross Profit 1,210

Chapter 8 – Exercise 1 (5 of 6) Part D: Assume that the company uses LIFO. Compute its ending inventory on July 31st, the cost of goods sold during July, and the company’s gross profit during July. Prices are rising in this example. If prices were rising, then it would be higher result SOLUTION: Calculation of ending inventory (1,600 piounds) from beginning ingentry (500 @ 1.00) 500 from July 5 purchase (1,000 @ 1.1) 1,100 from July 9 purcahse (100 @ 1.15) 115 1,715 Sales (3,800 @ 1.45) 5,510 Goods available for sale (part A) 6,295 Less: ending inventory 1,715 Costof goods sold 4,580 Gross Profit 930

Chapter 8 – Exercise 1 (6 of 6) Part E: On July 31st, the current purchase price for toffee dropped to $0.99 per pound. Compute the ending inventory amount that should be reported on the balance sheet on July 31st. SOLUTION: Lower of cost and market rule Calculation of ending inventory (1600 pounds @ 0.99 per pound) = 1,584

Chapter 8 – Exercise 2 (1 of 4) Nassau Navigational Supplies Inc had $104,000, $92,000, and $78,000 of inventory, and accounts payable of $43,000, $38,000, and $29,000 on December 31, 20A, 20B and 20C respectively. Nassau purchased $815,000 of inventory during 20B and $699,000 of inventory during 20C. Nassau reported net income of $319,000 for 20B and $327,000 for 20C. Part A: Compute Nassau’s cost of goods sold for the years ended December 31, 20B and 20C. SOLUTION:

Chapter 8 – Exercise 2 (2 of 4) Part B: Compute Nassau’s inventory turnover ratio for 20B and 20C. What does this ratio measure? Comment on the change, if any, in the ratio between 20B and 20C. SOLUTION:

Chapter 8 – Exercise 2 (3 of 4) Part C: Using only the information provided above, compute Nassau’s net cash flows from operating activities for the year ended December 31, 20B and 20C. SOLUTION:

Chapter 8 – Exercise 2 (4 of 4) Part D: Assume that Nassau made a computational error that understated its ending inventory by $5,000 at December 31, 20B. Compute the corrected amounts of cost of goods sold and net income for 20B and 20C. Determine the effect on retained earnings at December 31, 20C. SOLUTION:

Chapter 8 – Exercise 3 (A) Prepare the journal entries for each of the following transactions. Assume that the company uses a periodic inventory system and records freight charges in a separate account. Part A Sold merchandise for cash of $125,000. Periodic system -> doesn’t keep track. Record through purchases account If it were perpetual, we’d have an additional entry to debit cost of goods sold and credit inventory account for the amount of the historical cost of goods

Chapter 8 – Exercise 3 (B) Part B Refunded $12,000 to customers for merchandise returned.

Chapter 8 – Exercise 3 (C) Part C Purchased $15,000 of merchandise from Abaco Vending on credit, terms 2/10, n/30.

Chapter 8 – Exercise 3 (D) Part D Paid $500 freight bill on merchandise purchased.

Chapter 8 – Exercise 3 (E) Part E Paid Abaco Vending before the discount period has expired. Our year end cost of goods sold will be reduced by 300 dollars

![[Exercise Name]](https://cdn2.slideserve.com/4369850/exercise-name-dt.jpg)