Download

1 / 17

170 likes | 313 Views

The Classical Long-Run Model. Classical Model. A macroeconomic model that explains the long-run behavior of the economy. Classical model was developed by economists in 19th and early 20 th , to explain a key observation about economy.

E N D

Classical Model • A macroeconomic model that explains the long-run behavior of the economy. • Classical model was developed by economists in 19th and early 20th, to explain a key observation about economy. • Over periods of several years or longer, economy performs rather well • In the classical view, economy operates at full employment in the long run.

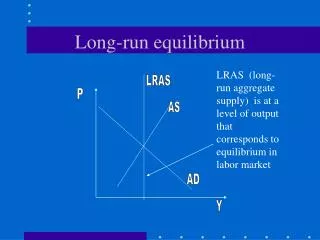

Assumption of the Classical Model Markets clear • Price in every market will adjust until quantity supplied and quantity demanded are equal • Markets might not be clear in the short-run, but if we wait long enough, eventually, the change in price will equate demand with supply.

The Classical Model • We’ll use classical model to answer important questions about economy in the long-run, such as • How does economy achieve full employment? • How much output can we produce? • How does economy operate on its own?

Full Employment Output • In the classical or long-run view, economy reaches its potential output automatically Output reaches its potential, full-employment level on its own, with no need for government to maneuver the economy toward it.

The Role of Spending • What if business firms are unable to sell all output produced by a fully employed labor force? • Economy would not be able to sustain full employment for very long • If we are asserting that potential output is an equilibrium for the economy • Total spending on output has to be equal to total production during the year • Can we be sure of this? • In classical view, the answer is YES

Total Spending in a Very Simple Economy • Imagine a world with just two types of economic units • Households and business firms • In a simple economy with just households and firms in which households spend all of their income • Total spending must be equal to total output • Known as Say’s Law

Total Spending in a Very Simple Economy • Say’s Law named after classical economist Jean Baptiste Say (1767-1832), who popularized the idea • Say’s law states that by producing goods and services • Firms create a total demand for goods and services equal to what they have produced or • Supply creates its own demand

Total Spending in a More Realistic Economy • In the real world • Households don’t spend all their income • Saving & taxes • Households are not the only spenders in the economy • Businesses and government buy some of the final goods and services we produce • In addition to markets for goods and resources, there is also a loanable funds market • Where household’s saving is made available to borrowers in business or government sectors

Some New Macroeconomic Variables • Planned investment spending (IP) IP = I – Δ inventories • Net taxes (T) T = total tax revenue – transfers • Household saving (S) Household sector’s disposable income • Disposable Income = Total Income – Net Taxes S = Disposable Income – C • Total Spending • Total spending = C + IP + G

The Classical Model: A Summary • Began with a critical assumption • All markets clear • In classical model, government needn’t worry about employment. • Economy will achieve full employment on its own. • In classical model, government needn’t worry about total spending. • Economy will generate just enough spending on its own to buy output that a fully employed labor force produces.