Download

1 / 8

80 likes | 97 Views

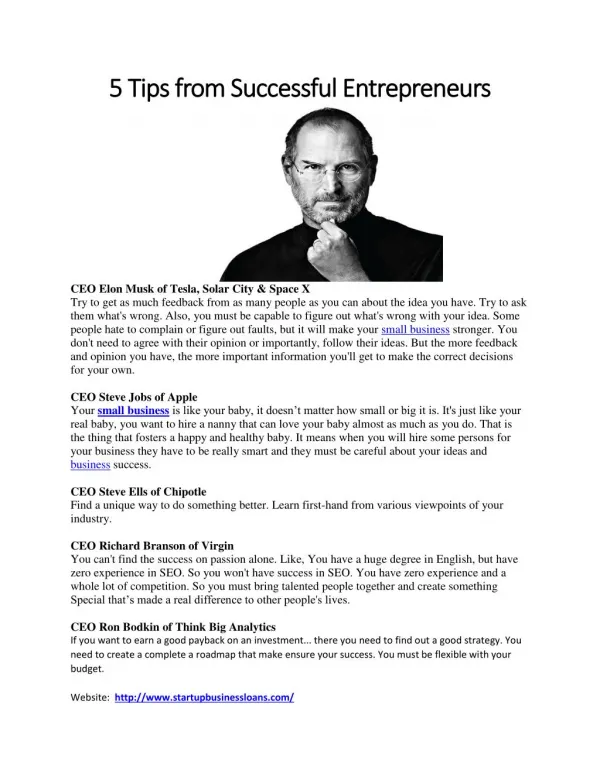

Andre Chambers Las Vegas is a seasoned consultant, investor, and entrepreneur with a background in gambling, tech, and finance. Andru00e9 Chambers Las Vegas offers five tips for first-time entrepreneurs that could save you time and money.<br>

E N D

Andre Chambers Las Vegas Andre Chambers Las Vegas, Nevada, has 20 years of experience in consumer electronics and retail, healthcare, and real estate.

Andre Chambers Las Vegas 5 Tips For First Time Entrepreneurs 1. Have crazy confidence in your product or service. 2. Make your own good luck. 3. Focus on your product or service, not running the business. 4. Operate on a shoestring. 5. Stop talking, and just listen.

1. Have crazy confidence in your product or service. When my company JAMF started in 2002 and focused on Apple users -- we now help more than 5,000 businesses and schools manage their iPhones, iPads and Mac computers -- Microsoft’s Windows was still the dominant desktop computing platform. Apple was a niche product for artists, musicians and teachers. Many people thought we were nuts for targeting such a narrow market. They said we had to add Windows support to be successful. But we believed in our strategy. So, be like us: Don’t be afraid to defy conventional wisdom.

2. Make your own good luck. I was studying music at the University of Wisconsin-Eau Claire around 2000 and working at a sandwich shop. When the eatery closed, I took a job at the university, providing tech support for professors’ Macs. (I had fooled around with Macs in high school and was minoring in computer science.) Then, my boss got transferred to another department and I took over his job. I got an idea for an automated software tool that could make the task of managing Macs easier, and thought I could make a business out of it.

3. Focus on your product or service, not running the busin First-time entrepreneurs often struggle with the dual responsibilities of building the product and operating the business. But the more you can focus on the first and outsource or postpone the second, the better. You can easily find people capable of, say, keeping your books. Only you know best how to build value for your offerings. Customers won't be attracted to you because you run your business well, but because of your great product.

4. Operate on a shoestring. When it’s time to hire employees, making payroll will become the No. 1 thing you lose sleep over. Your employees have families to support, mortgages to pay. They entrust you with their livelihood. So, put off hiring until you’re absolutely certain that that move is necessary to maintain and grow the business. Then, set a goal of six months’ payroll in the bank. Do whatever it takes -- make sales, rent cheap office space, keep expenses to a bare minimum -- to reach it.

5. Stop talking, and just listen. A rookie mistake that new entrepreneurs often make is yapping to customer prospects about how great their solution is before giving those customers a chance to talk about the problems they need solved. So, truly listen to and empathize with your customers. You'll stand a much better chance of making the sale and building a long-term relationship.