Case (9) :

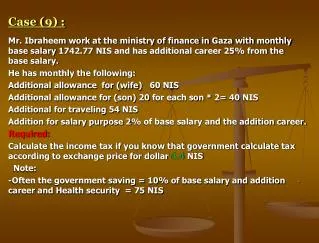

Case (9) : Mr. Ibraheem work at the ministry of finance in Gaza with monthly base salary 1742.77 NIS and has additional career 25% from the base salary. He has monthly the following: Additional allowance for (wife) 60 NIS Additional allowance for (son) 20 for each son * 2= 40 NIS

Case (9) :

E N D

Presentation Transcript

Case (9) : Mr. Ibraheem work at the ministry of finance in Gaza with monthly base salary 1742.77 NIS and has additional career 25% from the base salary. He has monthly the following: Additional allowance for (wife) 60 NIS Additional allowance for (son) 20 for each son * 2= 40 NIS Additional for traveling 54 NIS Addition for salary purpose 2% of base salary and the addition career. Required: Calculate the income tax if you know that government calculate tax according to exchange price for dollar 4.4 NIS Note: • -Often the government saving = 10% of base salary and addition career and Health security =75 NIS

Answer: Base salary 1742.77 Addition career 435.69 ( 1742.77*25% ) Addition allowance (wife) 60 NIS Addition allowance (son) 20 for each son * 2= 40 NIS Addition for salary purpose 2% of base salary and the addition career 2178.46*2% = 43.57 NIS Addition for traveling 54 NIS Total of salary =2376,03 Deduct excluded income according to Palestinian income tax law. - Government saving = (1742.77+435.69) * 10% = 217.84 (article 8 –item 9) Addition for traveling 54 NIS(article 6 –item 6) Health security = 75 NIS(article 8 –item 9) Total of excluded income 346.84 NIS taxable income= 2029.184 NIS Annual income for Ibraheem = 2029.184 * 12 / 4.4 = 5834.188$

Deduct exemption Resident 3000$ Wife 500$ Sons 1000$ Total of exemptions 4500$ Net taxable income after exemption 1034.14$ Annual income tax =1034.14*8%. =82.73$ Monthly income tax 82.73/12 = 6.89$ *4.4= 30.34 NIS.

Case (10) : The following are information for a taxpayer taken from his self assessment for the ended year 2008: Revenues: - Salary from job during the year =10,000$ - Sales for his own shop= 48,000$ - Net profit from shares =22,000$ (note: it is not the nature of his trade) - Revenue from farming project= 12,000$ - had a share of the patrimony from relative person =11,000$ Expenses: - Cost of goods sold for his own shop =18,000$ - Purchased a REFRIGERATOR for the shop amounted= 3000$ and the depreciation rate 10% annually. - Rent for the shop= 1200$ - The depreciation for the car =2000$ only 50% accepted by tax officer. - Utilities expenses for business (water, electricity, phone)= 500$ - Rent of his house =5000$ - Medical care expenses for his son (documented) =3000$ - Cost of school premium for his sons. (American school)= 1400$ - Living cost for his family =5000$

Personal information: Married and has two sons. Required: 1- total income 2- non taxable income 3- taxable income 4- deductions 5- exemptions 6- net taxable income 7- accrued tax 8- tax value to be paid 9- Not accepted deductions or exemptions (if any)

Answer: income: Salary from job during the year= 10,000$ Sales for his own shop= 48,000$ Net profit from shares= 22,000$ Revenue from farming project= 12,000$ A share of the patrimony= 11,000$ 1- Total of income = 103,000 $ non taxable income: Net profit from shares =22,000$ Revenue from farming project =12,000$ A share of the patrimony =11,000$ 2- non taxable income= 45,000 taxable income: Salary from job during the year =10,000$ Sales for his own shop =48,000$ 3- taxable income= 58,000$ Deductions: * Cost of goods sold for his own shop =18000$ * REFRIGERATOR depreciation = 300$ * Rent for the shop= 1200$ * The depreciation for the car 50%*2000= 1000$ * Utilities =500$ 4- deductions = 21,000$

Exemptions: Resident =3000$ Rent of house= 2000$ Medical care =3000$ Wife 500$ Sons 1000$ 5- exemptions = 9500$ 6- net taxable income = (58000-21,000-9500)= 27500$ 7- accrued tax =3360 10000* 8%= 800 6000*12% =720 11500*16% = 1840 8- tax value to be paid = 3360 $ 9- Not accepted deductions or exemptions = 10400$ 3000$+ 1000$+ 1400$+ 5000$