Download

1 / 39

390 likes | 539 Views

SPENDING AND OUTPUT IN THE SHORT RUN PART II. Chapter 11. PAE and Policy Changes: Fixed Price Model. Recall. PAE = C + I P + G + NX. Assumptions. 1) π e = 0 2) r = i. Types of Policy. Fiscal Policy 1) G 2) T Monetary Policy—M. G---Fixed Price Model.

E N D

SPENDING AND OUTPUT IN THE SHORT RUN PART II Chapter 11

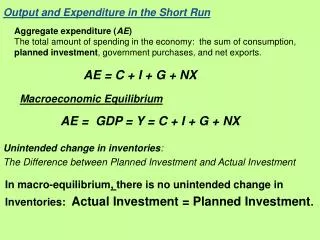

Recall PAE = C + IP + G + NX

Assumptions 1) πe= 0 2) r = i

Types of Policy Fiscal Policy 1) G 2) T Monetary Policy—M

G---Fixed Price Model G upward shift in PAE

G - Fixed Price Model Results ↑ Y & ↑ i

T---Fixed Price Model T (Y – T) C PAE PAE shifts upward

T---Fixed Price Model Results Y & i

M—Fixed Price Model M MS shifts outward i

i movement down IP • Recall r = i

M--Fixed Price Model Results Y & i

OUTPUT GAPS Y*=potential (full-employment) output (Y) = the amount of Y that an economy can produce when using resources at normal rates.

In 2002, Y* was defined as the level of Y when the unemployment rate is around 5.2%.

Monetary or fiscal policy can be used to eliminate a recessionary gap.

An expansionary gap can be eliminated with monetary or fiscal policy. For example, G

Active Fiscal Policy vs. Automatic Stabilizers Active Fiscal Policy—Actions taken on purpose. Laws must be changed. Automatic Stabilizers—provisions in the law that imply automatic increases in government spending or decreases in taxes when real output (income) declines.

Automatic stabilizers smooth out the business cycle by stabilizing (Y - T).

EXAMPLES 1) Income tax—when incomes fall, tax receipts fall; when incomes rise, tax receipts rise. 2) Transfer payments—increase when incomes fall and fall when incomes increase. Example: unemployment compensation.

The automatic stabilizers are important because of the lags in active fiscal policy.

Lags in Active Fiscal Policy 1) Inside lag a) Recognition lag—the time needed to realize that action is needed.—3 months b) Action lag—the time needed to make a change in policy.—1 – 15 months

2) Outside lag—the time needed for a policy change to have an impact on GDP.—1 – 3 months. 3) Total lag—inside lag + outside lag— 5 – 21 months.

Lags in Monetary Policy 1) Inside lag a) Recognition lag—3 months b) Action lag— 0 months 2) Outside lag—1 - 20 months 3) Total lag—3 - 23 months.

Market for Bank Loans • Demand for Bank Loans • Supply of Bank Loans

Market for Bank Loans • In a credit crunch, the supply of bank loans shifts inward. This increases the interest rate on bank loans.

The increase in the interest rate on bank loans reduces both C and IP . • PAE = C + IP + G + NX • The PAE function shifts downward.