Download

1 / 25

250 likes | 426 Views

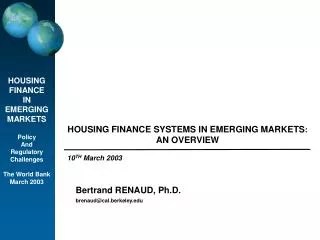

HOUSING FINANCE SYSTEMS IN EMERGING MARKETS : AN OVERVIEW. HOUSING FINANCE IN EMERGING MARKETS Policy And Regulatory Challenges The World Bank March 2003. 10 TH March 2003. Bertrand RENAUD, Ph.D. brenaud@cal.berkeley.edu. Agenda.

E N D

HOUSING FINANCE SYSTEMS IN EMERGING MARKETS:AN OVERVIEW HOUSING FINANCE IN EMERGING MARKETS Policy And Regulatory Challenges The World Bank March 2003 10TH March 2003 Bertrand RENAUD, Ph.D. brenaud@cal.berkeley.edu

Agenda • World trends are now producing a massive latent demand for housing finance • Today, housing finance systems in emerging economies are often very small • Strategies to develop mortgage finance systems are an integral part of overall financial development • The core functions of mortgage finance systems are universal. System expansion depends on lowering the costs of these core functions. • There is no universally applicable model of a mortgage finance system. Each national system results form macroeconomic conditions, overall banking regulations, the size of the banking system, taxation, subsidy programs and the structure of housing markets. These factors shape the path between bank-based and capital-market based mortgage loan delivery channels.

Urbanization creates a strong latent demand for mortgage finance International experience shows that a well functioning mortgage market will provide very large external benefits to the national economy: • - construction sector employment • - efficient real estate development • - easier labor mobility • - capital market development • - more efficient resources allocation • - lowered macroeconomic volatility

The UK had the only population to be more than 50% urban in 1900 “The invention of the amortized loan is of such importance [ … ] that it should rank with the invention of the steam engine in changing the face of Britain.” A.A. Nevitt, Housing, Taxation and Subsidies, 1966

The world is crossing the 50% urban threshold and passed the 6 billion mark Over 50% Less than 50% Least urbanized

Agenda • World trends are now producing a massive latent demand for housing finance • Today, housing finance systems in emerging economies are often very small • Strategies to develop mortgage finance systems are an integral part of overall financial development • The core functions of mortgage finance systems are universal. System expansion depends on lowering the costs of these core functions. • There is no universally applicable model of a mortgage finance system. Each national system results form macroeconomic conditions, overall banking regulations, the size of the banking system, taxation, subsidy programs and the structure of housing markets. These factors shape the path between bank-based and capital-market based mortgage loan delivery channels.

Housing finance depth: Ratios of outstanding mortgage loans to GDP (not scaled) 2. Middle East, 1999-2001 1. Latin America, circa 1998 4. Western Europe, 2001 3. East & Southeast Asia, circa 1998 US 1998: 53% EU-15, 2001 : 39%

Why are housing finance systems so often small ? • First and foremost, macroeconomic stability is a prerequisite. Macroeconomic volatility affects disproportionately all forms of long-term finance, of which mortgage finance is the most important. • Second, finance is a derivative of the real sector. One must understand how local housing markets operate and ask four questions: • What is the share of informal or extra-legal housing supply? • How affordable is housing? What is the price-to-income ratio level? • What is the total cost of mortgage borrowing: loan rate + transaction taxes and fees? • What is the structure of subsidies and what are their main channels? • Third, high transaction taxes and fees can suppress mortgage demand • Fourth, small overall financial systems are very common in emerging economies. Unfortunately, in finance small is seldom efficient. In 1999, 120 financial systems, i.e. two out of three countries had an M2 (stock of money) under US $10 billion. These systems served 800 million people. Note: these points are more fully developed in the detailed presentation provided in your conference binders

AS A RESULT: Cities are build the way they are financed (B. Renaud, 1987) • COMMERCIAL LENDING: • Diversified supply of housing units, • Production completed in short amount of time • Professional developers & organized R.E. industry • STATE FINANCING: • Standardized, monotonous, low value units (high resource cost, low use value for the occupants) • Inefficient industrial housing systems • Elimination of the real estate and financial services professions leading to critical skills constraints • INFORMAL FINANCING: • The visible outcome of policy and institutional failures • Slow incremental housing based on retained savings • “Self-development” by owners using small craftsmen 80% have access to formal finance MEXICO: Impact of past chronic macroeconomic instability 54% informal housing Access to housing finance services can vary widely according to macroeconomic conditions, banking systems, and the development of real estate markets

Agenda • World trends are now producing a massive latent demand for housing finance • Today, housing finance systems in emerging economies are often very small • Strategies to develop mortgage finance systems are an integral part of overall financial development • The core functions of mortgage finance systems are universal. System expansion depends on lowering the costs of these core functions. • There is no universally applicable model of a mortgage finance system. Each national system results form macroeconomic conditions, overall banking regulations, the size of the banking system, taxation, subsidy programs and the structure of housing markets. These factors shape the path between bank-based and capital-market based mortgage loan delivery channels.

Present changes in housing finance are part of broader financial trends • Changing role of the State • Fiscal restraint for greater macroeconomic stability • Economic and political decentralization • Privatization to leverage scarce public resources • More common non-state provision of “public” services • Need to restructure subsidies and achieve better social policies • Greater demand for transparency and accountability • Structural changes in the financial sector • Many forces are leading to a breakdown in inter-industry and inter- country barriers including: financial innovation, technology, regulation and taxation • Explicit focus of regulation and supervision on risk management • Convergence toward international standards in: accounting (IAS), banking (Basel II), insurance, securities market (IOSCO), valuation (IVSC) • Renewed concern about governance

Major changes in financial markets since the 1980s have created a new environment POST WW-2 DIRECTED-CREDIT POLICIES Leading government role in financial system: • Ceilings on interest rates on bank deposits • High reserve requirement on banks • Government directed bank credit • Micromanaging banks, little autonomy • Restrictions on entry, especially foreigners • Restrictions on capital flows Specialized housing finance circuits FINANCIAL LIBERALIZATION since 1980s Relaxation of financial constraints : • Elimination of interest rate controls • Lowering of bank reserve requirements • Reduced interferences with bank management decisions (focus on risks) • Privatization of nationalized banks • Foreign bank competition • Facilitation of capital inflows Boundaries are breaking down - Full integration with overall financial system - High rate of innovation + market deepening - The aim: systems more resilient to shocks

Innovations in the financial services industry are also reconfiguring housing finance

Agenda • World trends are now producing a massive latent demand for housing finance • Today, housing finance systems in emerging economies are often very small • Strategies to develop mortgage finance systems are an integral part of overall financial development • The core functions of mortgage finance systems are universal. System expansion depends on lowering the costs of these core functions. • There is no universally applicable model of a mortgage finance system. Each national system results form macroeconomic conditions, overall banking regulations, the size of the banking system, taxation, subsidy programs and the structure of housing markets. These factors shape the path between bank-based and capital-market based mortgage loan delivery channels.

THERE ARE THREE CORE FUNCTIONS TO ANY MORTGAGE SYSTEM • MORTGAGE ORIGINATIONis the process through which mortgage debt is created. It is comparable to the underwriting function for other loans and capital market securities. • MORTGAGE HOLDINGrefers to the activity of institutions and other investors who own or hold mortgage debt. When the mortgage originator and the mortgage holder differ, it is necessary to transfer mortgage ownership. The high risk, high information costs, and small size of individual mortgages complicate the mortgage transfer process. • MORTGAGE SERVICINGrefers to a series of activities, including: • collecting the monthly payments from the borrowers and transmitting the funds to the holders, • confirming that the borrower maintains property insurance and pays property taxes, and • carrying out the foreclosure process in cases of default. • These three functions are increasingly subject to large economies of scale Credit risk Liquidity risk Interest rate risk Prepayment risk THE MORTGAGE HOLDING FUNCTION IS THE STRATEGIC FUNCTION IN ANY MORTGAGE SYSTEM.

The allocation of the core financial risks explains the dynamics of a mortgage system • CREDIT RISK can create costly loan origination and servicing issues • LIQUIDITY RISK is the most immediate operational risk • INTEREST RATE RISK is potentially very high, and typically exceeds default risk • PREPAYMENT RISK is a concern that arises frequently for investors in mortgage-related securities Higher risks = higher loan rates = lesser loan demand • Legal, institutional and regulatory environments often increase the financial risks • of mortgage loans in emerging markets. • Organized government debt markets are a major positive externality to manage • liquidity risk. • The rise of institutional investors is the most powerful positive externality for the • Management of interest rate risk and the development of mortgage finance systems Note: these points are also more fully developed in the detailed presentation provided in your conference binders

The “all-in” cost of funding a mortgage loan is a measure of total system efficiency • Cost of mortgage functions • Origination • Holding • Servicing PRIVATE FUNDING COSTS • Government costs: • - Explicit (budget) • - Implicit (tax expenditures) • - Contingent cost of guarantees • - Quasi-subsides from state banks • Administration of the mortgage system PUBLIC COSTS • The “all-in” cost can be seen as the opportunity cost of supplying • mortgage finance for a given mortgage industry structure. • The goal of public policies is to support the emergence of market instruments and institutions that will lower one or more components of the all-in cost of mortgage funding.

Agenda • World trends are now producing a massive latent demand for housing finance • Today, housing finance systems in emerging economies are often very small • Strategies to develop mortgage finance systems are an integral part of overall financial development • The core functions of mortgage finance systems are universal. System expansion depends on lowering the costs of these core functions. • There is no universally applicable model of a mortgage finance system. Each national system results form macroeconomic conditions, overall banking regulations, the size of the banking system, taxation, subsidy programs and the structure of housing markets. These factors shape the path between bank-based and capital-market based mortgage loan delivery channels.

Financial markets typically evolve from BANKING-BASED to CAPITAL MARKET-BASED SYSTEMS Source: King and Levine, 1997

The Pre-1980s, directed-credit environments favored special housing finance circuits • The historical origins of mortgage lending were local, mutual institutions emerging in developing financial systems: British terminating building societies, permanent • building societies, US Savings & Loans, German Bausparkassen, Crédit différé, etc… “Special circuits” policies prevailed under the Post WW-II directed credit environment. WHY? The high all-in cost of mortgage lending by depository institutions made this line of business unattractive to commercial banks, so governments encouraged specialized lenders through a combination of restrictions and privileges: • must maintain high percentage of loan portfolio • in residential mortgage loans RESTRICTIONS - special tax benefits - lower capital requirements - can follow a short-funding strategy PRIVILEGES Non-diversified loan portfolios + short-funding strategy + avoidance of competition + low-level of innovation = fragility under macroeconomic volatility PROBLEMS The new financial environment has triggered many charter conversions

Today DEPOSITORY “PORTFOLIO LENDERS” remain the foundation • Retail deposits: lowest rate in the system • Vertical integration of all mortgage functions: no • cost of transferring mortgages • Informational advantages in credit evaluation for cross-lending with lowered information asymmetry Advantages • Financial costs of hedging interest risks under short-funding • Regulatory costs (capital ratios, liquidities, reserves) • and supervisory standards) • Deposit insurance ? Disadvantages • lack of economies of scale in origination and servicing • (Domestic impact of the IT revolution in information • Processing and retrieving) Private commercial banks in emerging economies are natural starting points to develop the housing finance system with their low-cost deposits, expertise in lending, access to retail customers. Access to capital markets permits both these retail banks and finance companies to expand their mortgage finance lines of business.

CAPITAL-MARKET BASED mortgage finance is a major structural change for the better Major opportunities exist with the rise of institutional investors in emerging economies: - pension reforms - insurance reforms - securities market reforms - development of mutual funds The growth of these potential mortgage-debt holders is usually quite significant But there are problems to solve with the sale of existing residential mortgages: - information asymmetry on credit risk - new unseasoned mortgages may default a few years later - mortgage loans are small relative to investor portfolio scale so that they cannot be individually evaluated The three main ways to address the information asymmetry problem: - development of underwriting standards - reputation of the retail level mortgage originator - credit guarantees • Different solutions exist to minimize and share risks based on: • banking regulation, taxation + finance industry legacies + role of government + private innovations • the feasible evolution of the all-in cost of mortgage finance

A great variety of mortgage market processes can be observed around the world Hold in portfolio Depository institution originates loans Issue mortgage bonds Sell whole loans To investor Investor Sell loans Secondary market institution or conduit Sell MBS to investors Pool loans into Mortgage backed securities Non-Depository institution originates loans Sell bonds to investors Issue mortgage bonds backed by loans • VARIETY OF LOAN ORIGINATORS: • A remarkable variety of loan originators can be observed today • reflecting the diversity of national systems • with significantly different all-in costs and degrees of overall efficiency • EXPANDING INVESTOR BASE: • Public pension funds • Private pension funds • Life insurance companies • Mutual funds • Commercial banks • Specialized lenders

New housing finance policies need to be consistent with other financial reforms Macro-economic demand management Fixed-income Securities Markets Major focus on pension and insurance reforms Retail Banking: Consumer Finance + Cross-Lending -New subsidy designs - Market-focused regulations - Restructured state institutions