Download

1 / 3

30 likes | 128 Views

This informative text delves into the financial impact of divestment on an endowment portfolio. It discusses the challenges with divesting from fossil fuel companies and the potential costs involved, including terminating manager relationships and finding new managers. The text also highlights the expected reduction in endowment returns and provides a comparative cost estimate based on similar investment strategies.

E N D

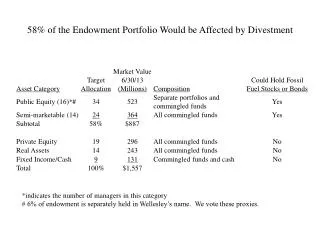

58% of the Endowment Portfolio Would be Affected by Divestment *indicates the number of managers in this category # 6% of endowment is separately held in Wellesley’s name. We vote these proxies.

The Cost of Divesting Separately Held Investments • The endowment holds approximately 0.5% in the largest 200 publicly traded fossil fuel companies in three separately held accounts. These accounts represent 6% of endowment assets. • Restricting the mandates of these managers is not possible, so divestment would require the College to terminate these manager relationships. • Over the last 10 years, these managers have beat their benchmarks by 1.75% a year. Finding new managers who would perform as well and be willing to manage a restricted mandate is highly unlikely. • Assuming that replacement managers earned the benchmark return, the cost of divestment would be:

The Cost of Divesting Separately Held and Commingled Holdings • Investments with managers whose mandates allow ownership of public stocks and bonds represent approximately 58% of the endowment. • Restricting the mandates of these managers is not possible, so divestment would require the College to terminate these manager relationships. • We expect current managers in these asset classes to earn 1.6% more than benchmarks over the next seven years. Finding new managers who would perform as well and would be willing to manage a restricted mandate is highly unlikely. • Assuming that replacement managers earned the benchmark return, the expected return of the endowment would be reduced by 1.6% a year. The dollar cost of divestment would be: • This estimate is in line with the $200 million over 10 year cost estimated by Swarthmore, an institution with a similar investment strategy and endowment.