Download

1 / 2

20 likes | 42 Views

auditing services in dubai With effect from October 1, 2017, Federal Decree Law No. (7) of 2017 (Excise Law) imposed excise duty on all commodities mentioned in Cabinet Decision No. 38 of 2017 (Decision 38). Decision 38 presently imposes the following excise taxes on "excise goods":<br>

E N D

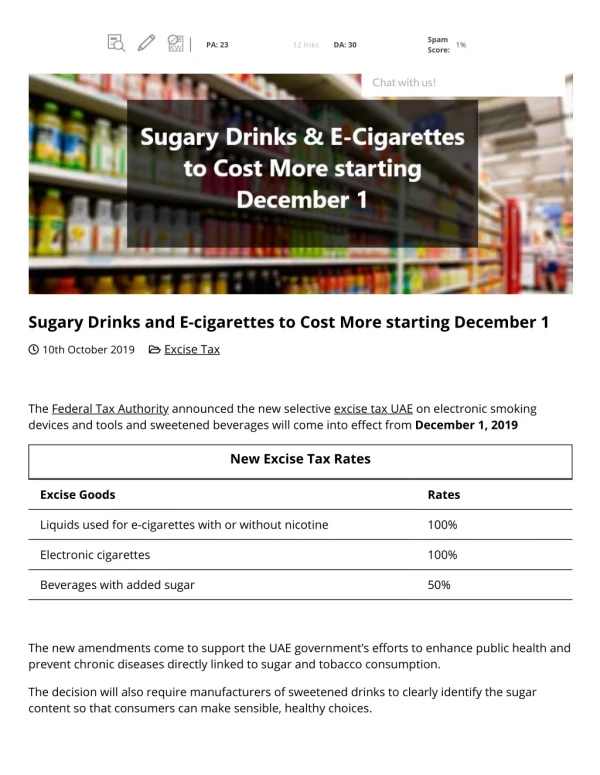

EXCISE TAX IN THE UAE - UPDATES auditing services in dubai With effect from October 1, 2017, Federal Decree Law No. (7) of 2017 (Excise Law) imposed excise duty on all commodities mentioned in Cabinet Decision No. 38 of 2017 (Decision 38). Decision 38 presently imposes the following excise taxes on "excise goods": 100% tobacco and tobacco goods 50% for carbonated beverages 100% pure energy drinks The Federal Tax Authority (FTA) of the United Arab Emirates (UAE) recently announced Cabinet Decision No. 52 of 2019 on Excise Goods, Excise Tax Rates, and Methods of Calculating the Excise Price. The same will apply as of December 1, 2019. According to the Cabinet Decision, an excise tax would be applied on sweetened drinks, liquids used in electronic smoking devices and equipment, and electronic smoking devices. and tools. The excise tax will be applied to new products. Whether or not they contain nicotine or tobacco, liquids are used in electronic smoking devices and instruments. The rate of the excise tax is 100%. sweetened drinks: Excise tax applies to any product that contains a source of sugar or sweetener and is manufactured as a ready-to-drink beverage or concentrates, powders, gel, extracts, or any other similar product that can be converted into a sweetened drink. The excise tax rate is 50%. Sweetened beverages exempt from Excise Tax Ready-to-drink beverages containing at least 75% milk or a milk replacement Handling of Foods for Particular Medical Purposes ingested for special dietary needs (baby formula, follow-up formula, or baby food) Beverages containing alcohol What Businesses Must Do The Federal Decree-Law No. 7 of 2017 on Excise Tax requires businesses/individuals engaged in any of the following activities to register for tax; Auditing company Importing excise products; manufacturing excise goods; releasing items from an excise Tax designated zone; stockpiling excise goods, in some situations; and warehouse keeping in some cases. As a result, importers, manufacturers, stockpilers, warehouse keepers, and others who deal in electronic smoking devices, liquids used in devices, and sweetened drinks must register for excise duty as soon as feasible. Failure to register within the stipulated time frame may result in fines and other complications. When a company qualifies as a stockpiler

In the UAE, a company might contemplate becoming a stockpiler.if the following requirements are met: The company had excise products in free circulation in the UAE that were meant to be sold in the course of business, and the excise tax on those goods had not been paid, remitted, alleviated, or deferred; and the company had 'excess' excise goods. If a company meets the aforementioned criteria, they must pay Excise Tax on "excess" excise items retained as of December 1, 2019. Many of UBL AUDIT s clients benefit from professional VAT consultancy services for Excise Tax implementation and post-implementation support.