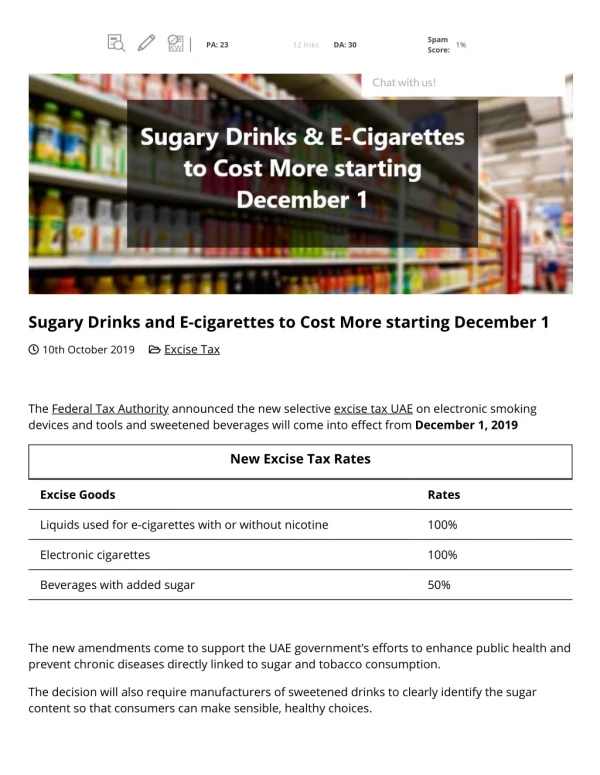

Excise Tax 102

Excise Tax 102. Energy & Environmental Taxes January 21, 2011. Frank Boland Chief, CC:PSI:7. BA, TCU; JD, SMU IRS since 1977 Branch chief of excise tax branch in IRS Counsel since 2003 Principal author or reviewer of most of fuel tax guidance since 1988 (202) 622-3130

Excise Tax 102

E N D

Presentation Transcript

Excise Tax 102 Energy & Environmental Taxes January 21, 2011

Frank BolandChief, CC:PSI:7 BA, TCU; JD, SMU IRS since 1977 Branch chief of excise tax branch in IRS Counsel since 2003 Principal author or reviewer of most of fuel tax guidance since 1988 (202) 622-3130 Frank.K.Boland@IRSCounsel.treas.gov

Deborah Karet Gordon • Senior Manager, KPMG Washington National Tax • (202) 533-5965 • dkaret@kpmg.com • Formerly-- • IRS Chief Counsel Office • Clerk, United States Tax Court • J.D. State University of New York; LLM New York University

Word of Caution • This is the Big Picture overview • There are different rules for different taxes • Federal excise tax law has a lot of exceptions to the general rules…and special rules for special cases on top of that • Many terms are terms of art

Today’s Agenda • Overview of Excise Taxes and Procedural Rules • Energy Taxes • Environmental Taxes

Retailers Alternative fuels Inland waterway trans. Tractors, trucks, trailers Manufacturers Gas guzzler cars Tires Taxable fuel Coal Vaccines Sport fishing equip. Bows & arrows Medical devices OverviewRetailers & Mfg TaxesIRC Chapters 31 & 32

OverviewRetailers & Mfg Taxes (cont’d) • 26 CFR 48.0-2 • Definitions and attachment of tax • 26 CFR part 40 • Procedural rules: time for filing Form 720; deposits • IRC 6416(a) & (b) • Conditions to allowance • Certain uses & resales treated as overpayments

OverviewFacilities & Services TaxesIRC Chapter 33 • Amounts paid for: • Local-only telephone service • Transportation of persons or property by air • Collected tax • Taxpayer is person paying for service; tax is collected & paid over by person receiving payment; IRC 6672 penalty applies to the collector • 26 CFR part 40; IRC 6415

OverviewEnvironmental TaxesIRC Chapter 38 • Oil spill • IRC 4611 • Form 720 and Form 6627 • Ozone-depleting chemicals • IRC 4681 • Form 720 and Form 6627

Transportation by water IRC 4471 Form 720 Highway use IRC 4481 Form 2290 Wagering IRC 4401, 4411 Forms 730, 11-C Tanning IRC 5000B Form 720 Branded prescription drug fee 9008 of ACA OverviewCertain Other Taxes and Fees

OverviewExcise Taxes Outside of PSI:7 • Foreign insurance (4371) • Obligations not in registered form (4701) • Firearms (4181) • Harbor Maintenance (4461) • Charities, employee plans, REITs • Alcohol, tobacco (subtitle E)

OverviewWhere Does the $ Go? • Truck and most fuel taxes • Highway Trust Fund • Air transportation taxes (including av gas and jet fuel) • Airport and Airway Trust Fund • General fund and other trust funds • IRC uses “trust fund” in 2 different ways • Funds held by the U.S. • Collected taxes held “in trust” by the collector

OverviewGeneral Procedural Rules • Rules in subtitle F that refer to “this title” or “internal revenue taxes” apply to excise taxes • So…usual assessment, collection, limitations, & enforcement rules apply • But…the deficiency procedures don’t apply so taxpayers can’t petition Tax Court on excise tax assessment • Instead, excise tax disputes are generally refund litigation in U.S. District Court or Claims Court • Excise taxes are divisible under Flora

OverviewSpecial Procedural Rules • Retailers & mfg, facilities & services, environmental taxes… • 26 CFR part 40 • Form 720 filed quarterly • Semi-monthly deposits by EFT • 95% of actual net liability, or • 1/6 of look-back quarter • Special September rules • Alternative method for Chapter 33 taxes

Energy Taxes • Taxable fuel • Alternative fuels • Renewable fuel incentives

Taxable FuelIRC 4081 & 4101 • Gasoline, diesel fuel, and kerosene • Generally, tax on: • Removal from a terminal at rack, or • Non-bulk entry into U.S. • Exemption from those taxable events for dyed diesel fuel & dyed kerosene • IRS registration requirements • 26 CFR 48.4101-1

Taxable FuelGasoline • Gasoline means finished gasoline and gasoline blendstocks • Finished gasoline: Products commonly or commercially known or sold as gasoline suitable for use as a fuel in a motor vehicle • Gasoline blendstocks are products listed in 26 CFR 48.4081-1(c)(3)

Taxable FuelGasoline Blendstocks • Includes butane, natural gasoline, straight-run gasoline, straight-run naphtha, toluene • Excludes any product that cannot, w/o further processing, be used in production of finished gasoline • Above-the-rack rules that apply to gasoline apply to gasoline blendstocks • Special rules below the rack (26 CFR 48.4081-4)

Taxable Fuel Hot Topics • Does entity deal in “taxable fuel”? • Is the taxable fuel in the bulk system? • Persons dealing in taxable fuel above-the-rack before removal from the terminal rack may have excise tax responsibilities, including registration and information-reporting requirements, even though they have no excise tax liabilities • Who may have excise tax responsibilities? • Operator of a butane storage facility • Commodities traders such as banks

Alternative Fuels IRC 4041 • Formerly known as special fuels • Liquids (and CNG) sold for use or used as fuel in motor vehicle or motorboat • Includes biodiesel (B100) and LPGs such as propane • Excludes fuel taxable under 4081

Alternative Fuels When and Who 1. Delivery into fuel supply tank of vehicle in connection with sale • Seller liable 2. Sale in bulk & buyer gives seller certificate saying it’s all for a taxable use - Seller liable 3. Delivery into fuel supply tank by vehicle operator when #1 and #2 didn’t apply - Operator liable

Alternative FuelsExemptions • Alternative fuel tax doesn’t apply to fuel used: • In farming • By states and nonprofit schools • In an off-highway business use • CNG tax doesn’t apply to fuel used in certain buses

Alternative FuelsHot Topics • Does taxpayer deliver alternative fuel into the fuel supply tank of a motor vehicle? • Are sales made to exempt users?

Renewable Fuel IncentivesIRC 40, 40A, 6426, 6427 • Alcohol fuels • Biodiesel and renewable diesel • Small ethanol and small agri-biodiesel producers • Cellulosic biofuel producers • Alcohol fuel mixtures • Biodiesel and renewable diesel mixtures • Alternative fuels • Alternative fuel mixtures

Renewable Fuel Incentives (cont’d) IRC 40, 40A, 6426, 6427 • All the renewable fuel incentives have been extended through 2011 • The incentive amounts vary • Each incentive has different claim rules • Some are nonrefundable income tax credits • Some are excise tax credits • Some may be excise tax payments • Some may be refundable income tax credits

Renewable Fuel IncentivesHot Topics • Is taxpayer the proper claimant for the renewable fuel incentives? • Has taxpayer complied with IRS registration rules? • Required registration for producers of alcohol, biodiesel, and cellulosic biofuel to avoid failure to register penalty • Alternative fuel claimants must be registered before claim may be allowed • IRS to issue guidance on claims covering periods during 2010

Environmental Taxes • Ozone-depleting chemicals (ODCs) • Oil spill • Expired Superfund

ODCs Montreal Protocol • Montreal Protocol is a series of international agreements relating to stratospheric ozone • Intent is to eliminate production and use of specified ODCs worldwide • Initial agreement effective January 1, 1989 • Under current Montreal Protocol • Developed countries would not produce or use specified ODCs after 1995 • Developing countries would not produce or use those chemicals after 2009 • Congress implemented Montreal Protocol by imposing excise tax on certain ODCs and imported products manufactured using those ODCs, effective January 1, 1990 • IRC 4681

ODCsIRC 4681-4682 • Imposes tax on importer’s sale or use of “imported taxable products” • Imported taxable product is any product entered into United States for consumption, use, or warehousing if any listed ODC was used in the manufacture of the product • Amount of tax based on weight of ODCs used in manufacture of product • Who is liable for tax? • The importer; that is, the person that entered the product into the United States for consumption, use, or warehousing

ODCs IRC 4681-4682 (cont’d) • Lists taxable ODCs • Includes CFC-11 (foams), CFC-12 (air conditioners and refrigerators), and CFC-113 (electronics) • Assigns an ozone-depletion factor to each listed ODC • Congress set ozone-depletion factor for each ODC in accordance with each ODC’s risk of depleting the ozone layer • The ozone-depletion factor for CFC-11 and CFC-12 is 1.0; the ozone-depletion factor for CFC-113 is 0.8 • Sets base tax amount for each year • In 1990, the base tax amount was $1.37 per pound • In 2011, the base tax amount is $12.55 per pound • For each year, the rate of tax for each ODC (per pound) is the product of the base tax amount and the ozone-depletion factor for that ODC

ODCs26 CFR part 52 • Regulations under 26 CFR part 52, Environmental Taxes • Imported products rules have not been updated since 1993 • What is an “imported taxable product”? • Any product entered into the United States for consumption, use, or warehousing, AND • Listed in the Imported Products Table (Table) in the regulations • Products listed in the Table include: • Electronics • Refrigerators and freezers • Foam sofas and chairs • Cars and trucks

ODCs 26 CFR part 52 (cont’d) • Generally, how is ODC weight determined for imported taxable products? • Exact method: the actual weight of each ODC used in manufacturing the product • Table method: the ODC weight listed in the Table for the product, if exact method is not used • Under the Exact Method how does importer determine whether ODCs were used in manufacture of product? • Exact method must be supported by sufficient and reliable information, such as a letter to the importer signed by the manufacturer that adequately identifies the product and states the weight of each ODC used in the product’s manufacture

ODCsHot Topics • Does taxpayer import articles that may be subject to the ODC tax? • Electronics • Refrigerators and freezers • Foam sofas and chairs • Cars and trucks • Recent IRS examination focus on ODC tax • IRS agreement with the U.S. Customs and Border Protection agency to receive import information on potentially taxable articles, by Harmonized Tariff Schedule (HTS) number • Issuance of IRS ODC Excise Tax Audit Techniques Guide in September 2008

Oil SpillIRC 4611 • Tax on crude oil and imported petroleum products (IRC 4611) • Crude oil received at a U.S. refinery • Petroleum products entered into the U.S. for consumption, use, or warehousing • Oil spill rate of tax is $.08 per barrel • IRC 4611(c)(1)(B) • Person liable for tax is: • Operator of refinery for crude oil received • Enterer of petroleum products

Oil SpillHot Topics • Legislative proposals could increase oil spill tax to as much as $.78 per barrel • No published guidance on scope of “petroleum products”

SuperfundHot Topics • Legislative proposals could reinstate the superfund taxes: • Tax on crude oil and imported petroleum products (IRC 4611) • Tax on certain chemicals (IRC 4661) • Lists the chemicals subject to tax • Tax on certain imported substances (IRC 4671) • Imported substances made using the chemicals listed in IRC 4661 • Corporate environmental tax (IRC 59A) • Taxes would fund the Hazardous Substance Superfund Trust Fund