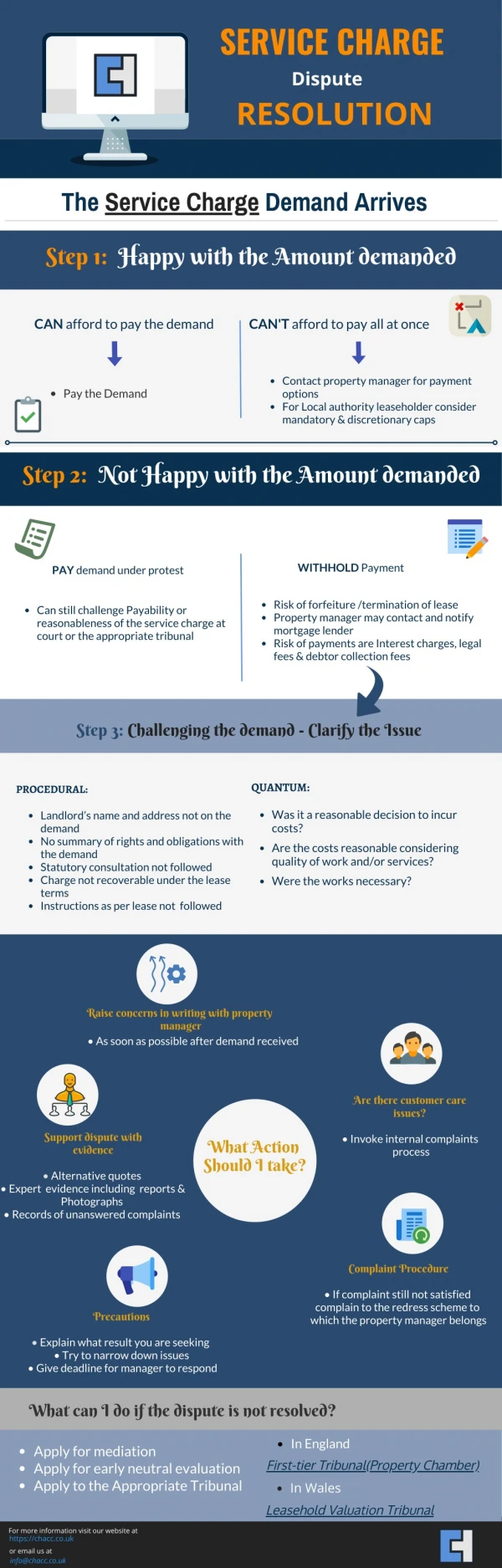

TRANSPARENCY IN LEASEHOLDERS SERVICE CHARGE

200 likes | 575 Views

TRANSPARENCY IN LEASEHOLDERS SERVICE CHARGE. Presented By: Anita Shields K & A Management Services Ltd Tel. 01604-401656, Email: anitaroussillon@aol.com. WHY DID SOUTHWARK APPROACH ME?. Audit Commission recommendation Similar experiences with other London Boroughs

TRANSPARENCY IN LEASEHOLDERS SERVICE CHARGE

E N D

Presentation Transcript

TRANSPARENCY IN LEASEHOLDERS SERVICE CHARGE Presented By: Anita Shields K & A Management Services Ltd Tel. 01604-401656, Email: anitaroussillon@aol.com

WHY DID SOUTHWARK APPROACH ME? • Audit Commission recommendation • Similar experiences with other London Boroughs • Easier to “Control” individual?

WHY ANOTHER AUDIT? • LEASEHOLDERS UNSATISFIED BY PREVIOUS AUDIT REPORT AND LACK OF TRANSPARENCY

Leaseholder Council Term of Reference • TR1-Traceability of Records • TR2-Accuracy of Order, Cost codes, Cost centre • TR3-Existence of Schedule of Rates • TR4-Existence of Contract Register • TR5-Method of measurement to calculate Ground Maintenance • TR6-Frequency of monitoring Account • TR7-Explanation for District heating and Lift charge

ELEMENTS OF SERVICE CHARGE TO REVIEW Cost on window cleaning, responsive repairs, etc.. Elements example: • Block Cleaning; • Estates • Refuse • Ground Maintenance • Etc…

HRA Grass & Beds On Housing Estates Split: 87% (based on land- mass, Type of work i.e. Man hours No review GENERAL FUND Park & Space outside estates (Common land) Split: 13% No review Rationale for split on shared areas-Ground Maintenance

WHY THE RESENTMENT AGAINST EXTERNAL AUDIT? • The Council Executive Officers resented being pressured by a lobby group i.e. Leaseholders Council to appoint their own “External Independent Auditor”

WHAT WAS THE DECISIONS FOR NOT CHOOSING PwC • Conflict of Independence and interest. • PwC could not act as External Auditor as they were already contracted as Internal Auditors. • Their Terms of Reference did not address issues • Level of Fee

REASONS FOR THE DIRECT APPROACH v TENDERING Conditions for appointment: • Security, Re-assurance. Recommended by Audit Commission • Contract had to be a maximum of £50k (No tendering requirement up to that level) • Maximum duration 4 months

TYPES OF PROBLEMS ENCOUNTERED • Delays in providing working papers for 05/06 year by Executives! • Deliberate obstruction in auditing process • Filtering of information by the Internal Audit • No authorisation signature for cleaners productive hours or any reconciliation to Agency Time sheet • Recharging cost not transparent or equitable

POOLE BUDGET A pro-rata basis for recharging cost Example: 1 Block= 3 flats= 90 Leaseholders Calculation Fee P.A.: 1000 Cleaners hrs @ £6.50=£6,500/3 £2,167/40=£54.17 per Leaseholder RESOURCE ACCOUNTING Allocate the “whole” cost into a unique cost centre Cleaners Hours: Block1-Flat40= 4 hrs@£6.50=£26 Block2-Flat126= 10hrs@ £6.50=£65 ACCOUNTING METHODS COMPARISON

ADVANTAGE Speed and simplicity Only require a pro-rata calculation i.e. useful for Rent DISADVANTAGE: Does not recharge the “Whole” cost POOLE BUDGET BENEFIT

ADVANTAGE Provides: Accountability Transparency and Traceability DISADVANTAGE: Require structure Skills Staffs training RESOURCE ACCOUNTING (Accrual) BENEFITS

WHICH METHOD WAS ADOPTED AND WHY? (What do you think?…)

THE EASIEST METHOD • Yes…The Poole Budget….

WHAT CONCLUSIONS CAN BE DRAWN? Some examples for transparency: • Management of the site transferred to the Leaseholders • Financial Management elected by Leaseholders • Leaseholders control all expenditure on their block, Estate, Flat

MAKE YOURSELVES HEARD • Challenge the way Service charge is accounted for • Ask for transparency • Provide Seminars and workshop for re-addressing accountability issues

Q & A • Now you know the fact, can I be of assistance?...It is up to you… Contact Details: K & A MANAGEMENT SERVICES LTD Tel. 01604-401656 Email: anitaroussillon@aol.com