Enron:

520 likes | 1.8k Views

Enron:. the scandal, the legend. Derivative. A derivative is an instrument whose value is “derived” from the underlying value of something else, such as a stock, a bond, or in the case of Enron’s derivatives, a unit of electricity.

Enron:

E N D

Presentation Transcript

Enron: the scandal, the legend

Derivative • A derivative is an instrument whose value is “derived” from the underlying value of something else, such as a stock, a bond, or in the case of Enron’s derivatives, a unit of electricity. • Derivatives are useful because they enable an investor to hedge against a decline in value. • Example: Enron could enter a contract with a purchaser of electricity, such as a utility, guaranteeing that the purchaser would pay a certain price for a certain amount of electricity at a certain date in the future.

WhistleBlower • The technical term for these often brave people is "whistle blower," as in the expression "blowing the whistle on corruption (or on government lies, etc)." • Whistle blowers are people who reveal generally harmful or very unfair activities, often of which they have become aware because of their employment position within their employer's organization and, or their access to otherwise unavailable communications from within the organization.

Internetbandwidth • By the late 1990s Enron controlled some 25 percent of all electricity and natural gas contracts traded worldwide and were considered the best in the business. • This success led Enron to act as a market middleman for other commodities as diverse as lumber and Internetbandwidth (the rate at which data can be delivered over the Internet).

401kPlan • Pension Plans- Employee 401k contributions are automatically deducted from their paycheck each pay period. This money is taken out before the employees’ paycheck is taxed. • The contributions are invested at the employees’ direction into one or more funds provided in the plan. • Employers often "match" employee contributions, but are not required to do so. • While the investments grow in the employees 401k account, they do not pay any taxes on it.

SPE • SPE- Acronym for Special Purpose Entities. • SPE’s reflect a common financing technique for companies. Companies can cut their risk by moving assets into separate partnerships that can be sold to outside investors. • In Enron’s case, assets that were losing money were sold to partnerships. Enron listed the sales of these assets as earnings. However, to be legitimate, accounting rules require that an SPE be legally isolated from the company that created it. • In Enron’s case this was not true. The SPE’s relied upon Enron managers for leadership and Enron stock for capital. When outside auditors told Enron to treat some of the 4,000 SPE’s it had created as part of Enron, the company had to take the $1-billion charge against earnings.

Key Players in the Enron Scandal • Kenneth Lay • Former CEO of Enron, helped start the company. • Enron extended to him $7.5 million revolving credit line, which he reportedly used and repaid with Enron stock 15 times within a period of just several months • He quit as CEO in February 2001 • He returned as CEO in August 2001until he resigned on Jan. 23, 2002 • He quit the Enron board altogether on Feb. 4. • Sherron Watkins said Lay was "duped" by top executives

Jeffrey Skilling • Enron's chief executive in the first half of 2001 • Since joining the company in 1990, Skilling helped transform Enron from a natural-gas pipeline company into an energy-trading powerhouse. • Between January and August 2001 he sold off about $20 million in Enron stock • Resigned after the close of markets on Aug. 14 2001 • Being charged with conspiracy, fraud and insider trading

David Duncan • Enron's chief auditor at Anderson • His job was to check Enron’s accounts • He is accused of ordering the shredding of thousands of Enron-related documents in an effort to hide them from Securities and Exchange Commission investigators

Andrew Fastow • Former Chief Financial Officer of Enron • The mastermind behind the deceptive accounting practices • Lea Fastow (his wife) also plead guilty to signing and filing a tax return that did not include income the Fastow’s had received from Mike Kopper

Sherron Watkins • Known as the "Enron whistle-blower" • Was Enron's vice president of corporate development • Wrote a letter to Kenneth Lay about “suspicions of accounting improprieties" • Not really a “whistle-blower” because she never went public with her suspicions

Enron What Went Wrong?

How did the collapse begin? • Energy companies lobbied congress in the 1980s for deregulation of the energy business • Energy policy was changed and Washington lifted controls on who could produce energy and how it was sold • Jeff Skilling took and aggressive approach to expand Enron by trading futures in gas contracts

Skilling’s Plan • Under Skilling’s new plan Enron bet against future movements in the price of gas-generated energy • “Enron bought and sold tomorrow’s gas at a fixed price today” • With every trade, Enron took a cut for transaction costs • Using the internet to promote trading, Enron became the most successful player in the futures game; 90% of Enron’s income came from trades

Early2000 • Enron took advantage of the dot.com boom and traded internet bandwidth • The value of Enron’s online transactions was huge ($880 billion) • The problem was Enron wasn’t making money on many of their online trades because they made the market very efficient

Fuzzy Numbers • Enron began tweaking the numbers in their financial statements with accounting techniques to hide their losses • Enron created partnerships, and then passed the assets (losses) to these partnerships which eliminated the losses from their balance sheets

Andrew Fastow (Chief Finance Officer) created the partnerships • Condor and Raptor were two major partnerships

Sherron Watkins, the Enron “Whistleblower” noticed the fuzzy accounting that had been used in relationship to the Condor and Raptor partnerships and wrote a letter to Kenneth Lay and Arthur Anderson warning him that the Enron was unstable.

Whywasn’tEnroncaughtearlier? • Throughout all of this, Enron and its key members were making political contributions to the white house and congress. • Kenneth Lay donated $100,000 to President Bush in 2000, and in 2001 Bush invited Lay to become an advisor to his transition team.

In the year 2000, Kenneth Lay met three times with Dick Cheney to discuss energy policy review. • When the review was published in May 2001, it was very favorable to the Enron and the energy sector.

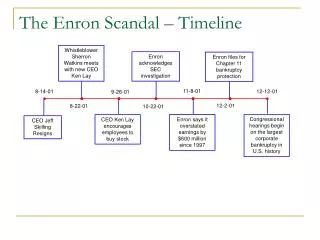

Aug 14, 2001 Jeff Skilling resigned, Kenneth Lay became CEO once again. • Stock prices began to fall, as investors were uncertain about the company’s stability. • This started a chain reaction: Enron had hedged against its own stock, so as long as the stock price was declining, it could not recover its losses.

December 2001, Enron filed for chapter 11 bankruptcy • It’s share price had collapsed from about $95 to under $1.

Chapter11Bankruptcy • Companies and large firms that are facing severe and unmanageable debt may seek to file chapter 11 bankruptcy, which allows them to re-organize so they can either continue their day-to-day operations or go out of business entirely. • Under chapter 11, a company is protected from damaging lawsuits and other negative measures, but in exchange the company is usually required to have all its major business decisions approved by the bankruptcy court.

WhatNow • “Enron is in the midst of restructuring various businesses for distribution as ongoing companies to its creditors and liquidating its remaining operations.”

Investor Sentiment • ``Enron has been elevated to a symbol,''says Woody Dorsey of Market Semiotics, an institutional forecasting service,``There's a whole new level of uncertainty about profits, about the integrity of the accounting profession and of Wall Street.'' • With a crisis like Enron,during a bear market, stocks typically take about 12 months to recover. • From 2000 to mid-2002 prices of stocks for the nation’s largest companies fell by more than 33 percent, while technology stocks dropped 70 percent (more factors than just Enron). • But, then again…

Market Efficiency • ``The market has already responded to the potential of overstated profits in the same way it responds to an unexpected negative event:ready, fire, aim,'' says Jeffrey M. Applegate, chief investment strategist at Lehman Brothers Inc. • This assumes a fully efficient market, one where all current information is already included in the prices.

Rocking Washington • After investors’ reaction to Enron and fear of more such scandals, Conservatives have learned a sobering lesson: • “The clamor for accountability in the financial system means more rules and regulations in a sector they have spent decades trying to deregulate.” • Democrats, though, were soon out calling for limits on the amount of company stock in 401(k) plans and moves to ease shareholder suits against corporate officers, directors, and auditors.

Dems vs. Reps • Democrats see Enron as justification for a strong assertion of government power to outlaw conflicts of interest and even restore the ban on companies operating in both the banking and securities industries. • The GOP would instead cater to the Investor Class with more transparency: • On Feb. 13, the SEC took a large step in that direction by announcing plans to impose far stiffer disclosure rules on companies, like insisting that significant trading in company stock by officers and directors must be revealed immediately & that any important changes in business must be reported within days.

Corruption & Regulation$ • After Enron, 89% of investors strongly favor the criminal prosecution of corporate officials who are implicated in serious financial fraud. • New York Stock Exchange and the National Association of Securities Dealers issued a proposal that would limit compensation that analysts can receive from investment-banking activity. • Other rules: restrict analysts' trading of stocks they cover, ban them from reporting to their firm's investment bankers, and prohibit them from promising favorable ratings to companies they cover.

Public Company Accounting Reform & Investor Protection Act • created the Public Company Accounting Oversight Board under the SEC’s supervision • board given the power to set accounting standards and to investigate whether companies and certified public accounting (CPA) firms are conforming to the standards • board also had the power to fine certified public accountants (CPAs) and their firms for violations, suspend CPAs and their firms, and recommend criminal investigations by the Justice Department • law also required CPA firms to separate their consulting & auditing services in order to avoid conflicts of interest like those in the Enron scandal

The Best Advice! • Investors were left wondering whether they could trust corporations, auditors, or stock analysts. • And thebest outcome from the present wave of angst would no doubt be a return to commonsense investing. Investors should place their bets on rationality, not the next skyrocketing stock.