Download

1 / 5

50 likes | 61 Views

Prior to continuing further, let us initially break down the assets of. Do recall one thing that because of proceeds with market uptrend

E N D

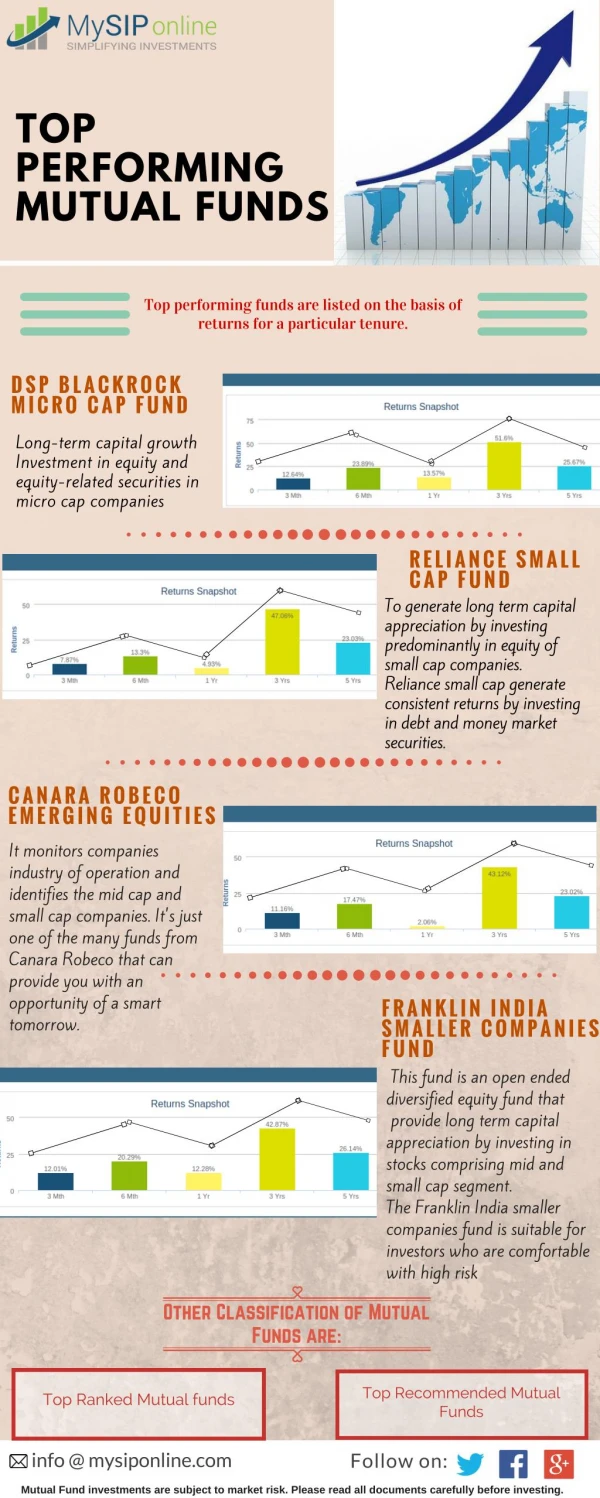

Top Performing Mutual Funds in India 2019: To Put Resources into India In 2018 Prior to continuing further, let us initially break down the assets of. Do recall one thing that because of proceeds with market uptrend, the dominant part of value reserves Top Performing Mutual Funds in India 2019 performed well and given you better returns. Notwithstanding, my worry is dependably to go for a reserve which is old, experienced all market cycle, given you consistence execution and furthermore with drawback insurance. Notice that few assets since a year not ready to beat the benchmark file. Notwithstanding, they have effortlessly beaten the benchmark in the event that you take a gander at 3 yrs., 5 yrs. or 10 yrs. returns. Henceforth, you no compelling reason to stress in this front.

Why I need to contribute? Prior to a BLIND speculation, it is in every case best that you should know the explanation behind your venture. Subsequently, before bouncing into venture read what I am sharing underneath. You should have a legitimate Financial Goal I saw that a considerable lot of financial specialists basically put resources into common supports just they have some surplus cash. The second reason might be somebody guided that shared assets are best in long run contrasted with Bank FDs, PPF, RDs, or even LIC enrichment item. On the off chance that you have lucidity like why you are contributing, when you require cash and the amount you require cash around then, at that point you will show signs of improvement clearness in choosing the item. Henceforth, first recognize your money related objectives. You should know the present expense of that specific objective. Alongside that, you should likewise know the swelling rate related with that specific objective. Keep in mind that each monetary objective to have its own swelling rate. For instance, training or marriage cost of your child’s is distinctive expansion that the swelling rate of family unit costs. By distinguishing the present cost, time skyline and swelling rate of that specific objective, you can undoubtedly discover the future expense of that objective. This future expense of the objective is your objective sum. I have composed a different post on the best way to set your monetary objectives. Read the equivalent at Resource Allocation is MUST

Subsequent stage is to distinguish the benefit portion. Regardless of whether it is here and now objective or long haul objective, the best possible resource allotment among obligation and value is an absolute necessity. I for one incline toward the underneath resource allotment. Keep in mind that it might contrast from individual to person. Be that as it may, the essential thought of advantage designation is to secure your cash and easily sail to achieve the money related objectives. In the event that the objective is underneath 5 years-Don’t contact value item. Utilize your preferred obligation results like FDs, RDs or Debt Funds. While picking obligation item, ensure that the development time of the item should coordinate your monetary objectives. For instance, PPF is best obligation item. In any case, it must match your monetary objectives. On the off chance that the PPF development period is 13 years and your objective is 10 years, at that point you will miss the mark regarding meeting your monetary objectives. Return Expectation Next and the greatest advance is the arrival desire from every benefit class. For value, you can anticipate that around 10% will 12% return. For obligation, you can expect around 7% return desire. At the point when your desires are characterized, at that point there is less likelihood of going amiss or taking automatic responses to the unpredictability. Portfolio Return Expectation

When you see how much your arrival desire from every benefit class is, at that point the following stage is to distinguish the arrival desire from the portfolio. Give us a chance to state you characterized the advantage designation of obligation: value as 30:70. Return desire from obligation is 7% and value is 10%, at that point the general portfolio return desire is as underneath. The amount to contribute? Once the objectives are characterized with target sum, resource designations is done, return desire from every benefit class is characterized, at that point the last advance is to recognize the sum to contribute every month. There are two different ways to do. One is steady month to month SIP all through the objective time frame. Second is expanding some repaired % every year to the objective time frame. Choose which suits best to you. Expectation the above data will give you clearness before hopping into value common store items. What numbers of shared assets are sufficient? What number of common assets do we have? Is it 1, 3, 5 or more than 5? The appropriate response is straightforward… you needn’t bother with more than 3-4 assets for putting resources into common assets. Regardless of whether your venture is Rs.1,000 per month or Rs.1 lakh multi month. With the most extreme of 3-4 reserves, you can without much of a stretch make a differentiated value portfolio. Having some good times does not give you enough broadening. Rather, as a rule, it might make you portfolio covering and prompts under performance. Presently let us move to the determination of shared assets. Tax collection of Equity Mutual Funds for 2018-19

Keep in mind that Equity Funds and Debt reserves are exhausted in an unexpected way. Subsequently, you should comprehend the tax assessment part also before hopping into speculation. I endeavored to clarify the equivalent in underneath picture. Click Here: Know the Profits from Your Endowment Best Ulip Plans in India 2019