Download

1 / 17

170 likes | 665 Views

Financing the Supply Chain Legal Issues Harriette Resnick, Executive Director & Assistant General Counsel Central American Meeting on Secured Financing and Related Commercial Law Reform Tegucigalpa, Honduras February 28-29, 2008 Background

E N D

Financing the Supply Chain Legal Issues Harriette Resnick, Executive Director & Assistant General Counsel Central American Meeting on Secured Financing and Related Commercial Law Reform Tegucigalpa, Honduras February 28-29, 2008

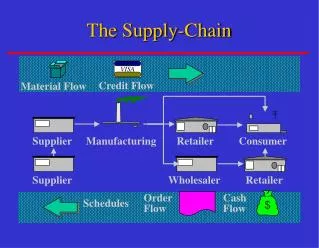

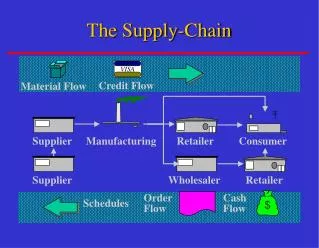

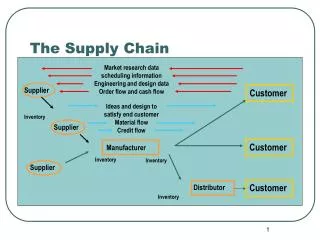

Background • Financing the Supply Chain: changes in Customer needs and the market and business environment. • Historically, Banks Supported Import Transactions by: • Letter of Credit • Purchase of L/c Drafts • Purchase of negotiable instruments (Trade Drafts or bills of exchange • Market trends • Declining Usage of Import L/cs • Increased preferences for open account transactions • Longer payment terms

Background • Products that help Customers obtain financial support for trade transactions on an open account basis: • Supply Chain Financing • Receivables Purchase/Discounting Facilities • Silent Payment Guarantee issued to suppliers

Common Features of These Products • Buyer owes account (payment obligation from sale of goods or services) to Seller. • Bank makes a payment to Seller in consideration for assignment of Buyer’s account to Bank. • Receivables (accounts) are assigned to Bank. • Bank takes the Buyer’s credit risk but has limited recourse to the Supplier in the event of nonpayment due to Buyer’s commercial dispute with the Supplier.

Common Features of these Products • Not an Independent Undertaking. • Buyer’s payment obligation to Bank as assignee from Supplier would be subject to defenses available to Buyer against Supplier. • Not subject to standard practice terms such as UCP or ISP. • Rights and obligations of the parties are determined by contractual terms. • Receivables purchase agreement between Bank and Supplier. • Contract between Buyer and Supplier determines Bank’s right to receive payment, unless Buyer waives defenses to payment.

Common Features of these Products • Relationship with Parties/Due Diligence. • Buyer/Obligor is a customer with available unsecured credit lines. • Full KYC review of Buyer, OFAC screening and CIP process. • Supplier may or may not be a credit customer of Bank • If a customer, including an account holder: Bank conducts a full KYC review OFAC screening before any payment to Supplier, and CIP process.

Common Objectives • Bank needs to acquire an enforceable payment obligation to Buyer/account debtor • Bank needs to have a perfected interest in the payment obligation, ahead of the claims of supplier’s creditor. • owner of asset is purchaser of receivables • receivables are not Supplier’s assets • receivables are not subject to prior claims of Supplier’s creditors

Legal Issues • What are the necessary steps for Bank to obtain ownership? • Can Buyer’s account be assigned? • Are future accounts assignable? • How to ensure that Buyer’s payment must be made directly to Bank? • What defenses to payment can be raised by Buyer against Bank? • What law determines the answer to these questions?

Answers under US Secured Transactions Law • -What law determines the answer to these questions? • US: Look to the law of Supplier’s /Assignor’s Location • Relevant Excerpts from Uniform Commercial Code (UCC) Article 9 • -What are the necessary steps to obtain ownership of the payment obligation? • Perfection of Ownership/Security Interest – Filing UCC financing statements Benefits of Notice Filing System – Transparency • Any financing party that has been granted a security interest in, or sold accounts (receivables) by the debtor (Supplier) does not have an interest that can be enforced against third parties unless it does the appropriate filing. • This prevents secret liens or disputes as to when security or ownership interest were assigned to the financing party.

- What do you file? • Filing of a simple record (financing statement) with limited information: • Name of the debtor (Supplier); secured party (Bank) and a description of the collateral which reasonably identifies it (UCC 9-108, 9-502, 9-504 ) • - Where do you file? • This record is filed in a centralized, public recording office. • If Supplier is a US corporation, the financing statement is filed with the secretary of state of Supplier’s state of incorporation. • To perfect under US law, Bank can file in Washington D.C. against foreign Suppliers from countries that do not have notice filing systems

- Effect of filing? • The only way in which to perfect an ownership or security interest in accounts to file a financing statement in the appropriate public recording office. • Financing statements generally are effective for 5 years unless terminated or there has been a change in Supplier’s name or location. • - How to get Priority? • The rule is “First to file”. (UCC 9-322) • A financing statement covering the same collateral which has been filed previously in the appropriate public recording office will give the named secured party a prior interest in that collateral. • If there are prior filings, waivers must be obtained or the filings terminated for subsequent filings to have priority.

- Lien Searches; Waivers • These records can be searched and copies of any filed financing statements obtained. • As a result, can determine with certainty whether there are other existing liens or security before agreeing to purchase accounts or provide secured financing. • - Who can file? • Bank, if authorized by Supplier or if Supplier has signed a security agreement covering the collateral described the financing statement (UCC 9-509) • - When can you file? • A financing statement can be filed before the security interest attaches or becomes enforceable. • The security interest attaches or becomes enforceable against Supplier and its creditors only after it is granted by Supplier to Bank and value is given by Bank. (UCC 9-502(d), 9-203)

Can the Buyer’s payment obligation be assigned? • Buyer’s payment obligation can be effectively assigned or pledged, even if the contact between Buyer and Supplier prohibits such assignment. (UCC 9-406(d)). • These provision enables free assignability of such financial assets. • It also protects Supplier from being in default under or subject to termination of its contract with Buyer solely due to such assignment or pledge.

Are future payment obligations assignable? • An agreement may create or provide for a security or ownership interest in accounts acquired by Supplier after the date of the agreement. (UCC 9-204(a)). • This permits multiple financing or purchase transactions without the need to sign a separate assignment or security agreement for each purchase or pledge of accounts. • A financing statement covering accounts will be effective to give Bank a perfected interest in Supplier accounts created or sold after the date of the filing.

How does Bank ensure that Buyer’s payment must be made directly to Bank, not Supplier? Buyer must pay Bank if it receives notification that the amount due or to become due has been assigned and that payment is to be made to the Bank. After receipt of such notification, Buyer may only discharge its obligation by paying the Bank. The notice may be provided by Bank or Supplier (UCC 9-406(a)). Notification can be given by electronic means that meet authentication requirements giving such message the effect of writing.

-What defenses to payment can be raised by Buyer against Bank? • As assignee, Bank would acquire the right to receive payment of Supplier’s subject to the following defenses of Buyer: • All defenses available against Supplier in the transaction generating the account; and • Any other defenses available against Supplier that accrue before Buyer receives notice of assignment. (UCC 9-404(a)). • However, Buyer may make an enforceable agreement not to assert such defenses or claims against Bank. • This agreement would be enforceable by Bank so long as it has given value to Supplier in good faith without notice of a defense to payment. (UCC 9-403(b). • A waiver of defenses by Buyer is part of the Supply Chain Finance product. • As this may not be true of all receivables purchases from Supplier, Bank requires the right to recover from Supplier any reductions in payment due to contractual disputes with Buyer.

Challenges of Cross-Border Transactions • Choice of Law rules (which country’s law applies) vary • Absence of notice filing system • Notice of assignment to Buyer - Formalities of Assignment Documentation - Assignment of Future Receivables may not be possible • FX Restrictions • Delivery of original invoices may be required