Download

1 / 28

310 likes | 960 Views

Beginning the Accounting Cycle – Journalizing, Posting, and the Trial Balance. Chapter 3. Journalizing: analyzing and recording business transactions into a journal. Learning Objective 1. The Accounting Cycle. Accounting procedures are performed over a period of time.

E N D

Beginning the Accounting Cycle –Journalizing, Posting,and the Trial Balance Chapter 3

Journalizing: analyzing and recording business transactions into a journal. Learning Objective 1

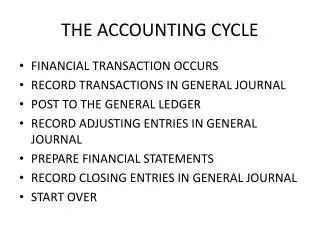

The Accounting Cycle • Accounting procedures are performed over a period of time. • Procedures are performed in a definite order in the accounting cycle. • The accounting period is a period of time covered by the income statement. • Usually this is a twelve month period. • The accounting cycle has sequential steps to be performed again each year.

The Accounting Cycle • Accounting is the process that... • analyzes, • records, • classifies, • summarizes, • reports, and... • interprets.

The Accounting Cycle A sole proprietorship: • has one owner • begins with a monthly accounting cycle • owner has a capital and withdrawals account

Business Organizations • All three types of business entities use the same basic accounting system. Sole proprietorship Partnerships Corporations

Recording Business Transactions The Accounting Period One Year Calendar year Fiscal year Less than One Year Quarterly Monthly

Learning Unit 3-1 • The Accounting Cycle: • Analyzing • Recording transactions – journalizing • Posting to the ledger accounts • Preparing the trial balance • The accounting cycle has some variations in a computerized accounting system.

Learning Unit 3-1 What is the general journal? • It is the book of original entry. • Transactions are written in a journal in chronological order. • The format of the journal is important. • Journalizing is the process of entering information as debits and credits to the correct accounts.

Learning Unit 3-1 What is the general ledger? • It is the book of final entry. • The information from the journal is transferred to the ledger in the posting process. • Debits and credits in the journal remain exactly the same when posted to the accounts in the ledger.

Learning Unit 3-1 What is the chart of accounts? • It is the list of accounts used by a business. • Each business entity has its unique chart of accounts. • Every chart of accounts has the same numbered account categories: • Assets, Liabilities, Owner’s Equity • Revenues, Expenses

Learning Unit 3-1 Journalizing • Debits are always recorded first. • Indent, then record the credit below the debit. • A short explanation is included on the second line. • Leave a space between journal entries.

Learning Unit 3-1 • Debits must always equal credits. • Amounts incurred for items that benefit future accounting periods are recorded as assets. • What are some examples? • prepaid rent • prepaid insurance

Learning Unit 3-1 • Amounts for items used (expenses incurred) in the current accounting period are recorded as expenses. • What are some examples? • supplies used • rent for the month • expired insurance

Learning Unit 3-1 • Amounts are recorded as revenue on the date in which they are earned. • When are revenues earned? • When services are performed, not necessarily when cash is paid.

Posting: transferring information from a journal to a ledger. Learning Objective 2

Learning Unit 3-2 Posting • All transactions are recorded in the journal, then amounts are copied to the ledger accounts named on the journal line. • Once the amounts are entered into the accounts, a posting reference (PR) must be entered in the journal. • New balances are computed in the running ledger accounts.

Learning Unit 3-2 Posting Account: Cash Account: 1000 Balance Date ref. debit credit debit credit June 1 jr1 5,000 5,000 Insert the number of the journal page.

Example Journal Page 1 Date Account and Explanation Post Ref. debit credit June 1 Cash 1000 5,000 Clara J. Capital 3010 5,000 Initial investment

Example Journal Page 1 Date Account and Explanation Post Ref. debit credit July 3 Phone Expense 5040 155 Accounts Payable 2000 155 Paid phone bill

Example Journal Page 1 Date Account and Explanation Post Ref. debit credit July 6 Insurance Expense 5060 150 Cash 1000 150 Paid insurance bill

Example Journal Page 1 Date Account and Explanation Post Ref. debit credit July 8 Accounts Payable 2000 200 Cash 1000 200 Paid Accounts Payable

Example Journal Page 1 Date Account and Explanation Post Ref. debit credit July 8 Accounts Receivable 1020 850 Service Revenue 4000 850 Performed Services

Preparing a trial balance. Learning Objective 3

Learning Unit 3-3 Preparing the Trial Balance • The trial balance lists the accounts that have balances in the same order as they appear in the chart of accounts. • The trial balance will show if debits/credits have been interchanged, or if amounts have been transposed, or if a debit/credit was omitted or recorded twice.

Learning Unit 3-3 • Some errors do not show, such as omissions or recording to the wrong account. • Corrections before posting are made in the journal. • An audit trail must be left. • Do not erase – cross out errors and enter corrections.

Learning Unit 3-3 • What about corrections after posting? • This means that errors are also in the ledger accounts. • Cross out incorrect amounts, change to corrected amounts, and record balance changes.