Download

1 / 8

100 likes | 668 Views

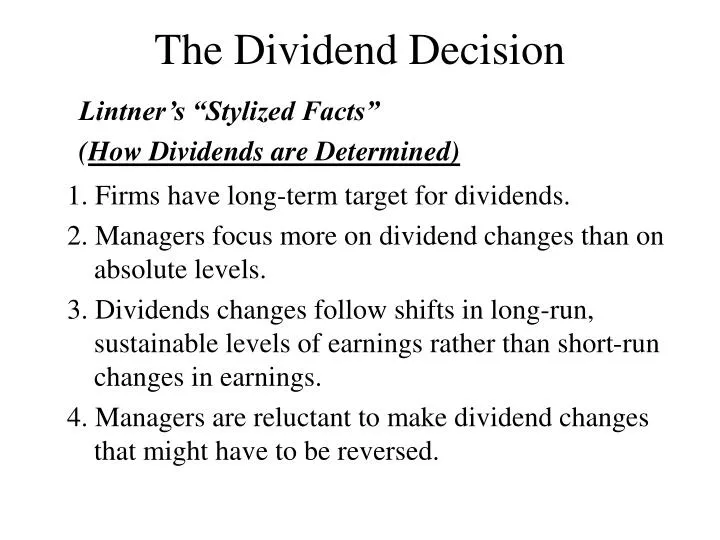

The Dividend Decision. Lintner’s “Stylized Facts” ( How Dividends are Determined). 1. Firms have long-term target for dividends. 2. Managers focus more on dividend changes than on absolute levels.

E N D

The Dividend Decision Lintner’s “Stylized Facts” (How Dividends are Determined) 1. Firms have long-term target for dividends. 2. Managers focus more on dividend changes than on absolute levels. 3. Dividends changes follow shifts in long-run, sustainable levels of earnings rather than short-run changes in earnings. 4. Managers are reluctant to make dividend changes that might have to be reversed.

Remember Gordon model Constant Growth DDM - A version of the dividend growth model in which dividends grow at a constant rate (Gordon Growth Model). Given any combination of variables in the equation, you can solve for the unknown variable. Gordon actually had r increasing due to risk. This implies dividends increase value.

Dividend Policy is Irrelevant • MM III • Since investors do not need dividends to convert shares to cash they will not pay higher prices for firms with higher dividend payouts. In other words, dividend policy will have no impact on the value of the firm • V(x-d)+V(d)=V(x+d-d)=V(x).

Dividends Decrease Value Tax Consequences Companies can convert dividends into capital gains by shifting their dividend policies. If dividends are taxed more heavily than capital gains, taxpaying investors should welcome such a move and value the firm more favorably. In such a tax environment, the total cash flow retained by the firm and/or held by shareholders will be higher than if dividends are paid.

Stock buy-backs • A firm has 1 million shares with a price of £10 and wanted to give a dividend of £1 per share. Let us call this choice A. • It could simply buy back 100,000 shares for £10 each instead. Let us call this choice B. • What are the price of the stock after A and B? Explain.

Interesting Point • Norway doesn’t tax dividends. This should make foreign investors want to sell pre-dividend day. • Pb-tg(Pb-P0)=E[Pa]-tg(E[Pa]-P0)+D(1-td) • Elton & Gruber [1970] found ex-day drop to be 77.8% of the dividend. • Some say that taxes on dividends can be avoided by various tricks, so it returns to MM world.

Dividends increase value • Clientele theory again (some people like the high dividends). Still, would a change attract these people. • Incomplete contracts: Manager’s incentives. It can be used to punish managers or reduce their free cash. • Can help keep them honest or stop them from making poor investment decisions. • Some institutions are restricted by which stocks they buy: only those with dividends. • May reduce transaction costs.

Dividends Increase Value Dividends as Signals Dividend increases send good news about cash flows and earnings. Dividend cuts send bad news. Because a high dividend payout policy will be costly to firms that do not have the cash flow to support it, dividend increases signal a company’s good fortune and its manager’s confidence in future cash flows. Worth reading this on dividends and just 141 pages! http://fic.wharton.upenn.edu/fic/papers/01/0121.pdf