Download

1 / 2

20 likes | 121 Views

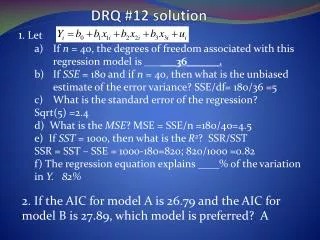

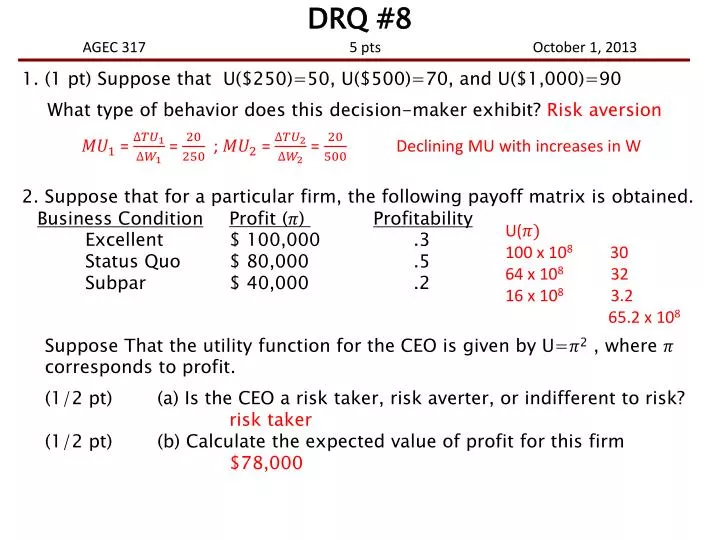

DRQ #8 AGEC 317 5 pts October 1, 2013. 1. (1 pt ) Suppose that U($250)=50, U($500)=70, and U($1,000)=90 What type of behavior does this decision-maker exhibit? Risk aversion 2 . Suppose that for a particular firm, the following payoff matrix is obtained.

E N D

DRQ #8AGEC 317 5 pts October 1, 2013 1. (1 pt) Suppose that U($250)=50, U($500)=70, and U($1,000)=90 What type of behavior does this decision-maker exhibit?Risk aversion 2. Suppose that for a particular firm, the following payoff matrix is obtained. Business ConditionProfit () Profitability Excellent $ 100,000 .3 Status Quo $ 80,000 .5 Subpar $ 40,000 .2 Suppose That the utility function for the CEO is given by U=2 , where corresponds to profit. (1/2 pt) (a) Is the CEO a risk taker, risk averter, or indifferent to risk? risk taker (1/2 pt)(b) Calculate the expected value of profit for this firm $78,000 = = ; = = Declining MU with increases in W U( 100 x 108 30 64 x 108 32 16 x 108 3.2 65.2 x 108

DRQ #8AGEC 317 5 pts October 1, 2013 (1 pt) (c) Calculate the expected utility for the CEO. 652 x 107 65.2 x 108 set = 65.2 x 108 = 8.0747 x 104 (1 pt) (d) What is the risk premium? EV - = 80,746.62 $28,000 - $80,746.62 = -$2,746.52 3. (1 pt) The certainty equivalent of any investment typically is associated with yield on riskless U.S. government securities. Suppose that this yield is 3%. Suppose that capital investment for a business venture is $200,000. Suppose that the expected value in regard to this business venture is $50,000. What is the minimum certainty equivalent adjustment to justify this investment? certainty equivalent adjustment factor= = = .12 The “price” of one dollar in this risky venture is equivalent to 12 cents in certain dollar terms.