Download

1 / 30

300 likes | 304 Views

Explore the concept of equilibrium in economics and how it is affected by government interventions such as price floors and ceilings. Learn about excess supply, shortage, and the impact of rent control laws. Discover the relationship between supply and demand, and how technological advancements can affect market outcomes.

E N D

Equilibrium Review Economics Mr. Bordelon

Key Terms • The point at which quantity demanded and quantity supplied are equal.

Key Terms • The point at which quantity demanded and quantity supplied are equal. • Equilibrium

Key Terms • Any situation in which quantity supplied exceeds quantity demanded.

Key Terms • Any situation in which quantity supplied exceeds quantity demanded. • Excess supply • Surplus

Key Terms • Any situation in which quantity demanded exceeds quantity supplied.

Key Terms • Any situation in which quantity demanded exceeds quantity supplied. • Excess demand • Shortage

Key Terms • A government-mandated minimum price that must be paid for a good or service.

Key Terms • A government-mandated minimum price that must be paid for a good or service. • Price floor

Key Terms • A government-mandated maximum price that is allowed to be charged for a good or service.

Key Terms • A government-mandated maximum price that is allowed to be charged for a good or service. • Price ceiling

Main Ideas • What role does the government play in determining some prices?

Main Ideas • What role does the government play in determining some prices? • The government can offer price floors, such as farm subsidies or minimum wage, and price ceilings, such as rent control.

Main Ideas • What problem can a price floor cause?

Main Ideas • What problem can a price floor cause? • Price floors can cause excess supply.

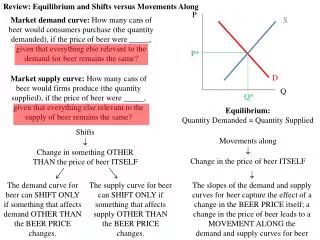

Main Ideas • Explain how to interpret the supply and demand graph. • Equilibrium • Demand • Supply • Price and Quantity • Shift of Supply or Demand

Main Ideas • Where is equilibrium? How do you know? • Where is a shortage? How do you know? How much is that shortage? • Where is a surplus? How do you know? How much is that surplus?

Main Ideas • Where is equilibrium? How do you know? $1.50, Qd = Qs. • Where is a shortage? How do you know? How much is that shortage? $0.50 - $1.00, Qd > Qs, 200 ($0.50) or 100 ($1.00) • Where is a surplus? How do you know? How much is that surplus? $2.00 - $3.00, Qs > Qd, 100 ($2.00), 200 ($2.50), or 300 ($3.00)

Critical Thinking • Why have some cities and towns passed rent control laws? How do these laws affect price equilibrium? What happens when these laws are repealed?

Critical Thinking • Why have some cities and towns passed rent control laws? How do these laws affect price equilibrium? What happens when these laws are repealed? • Rent control laws are enacted to control inflation of prices and assist lower-income groups. The laws cause disequilibrium, resulting in a shortage. When rent control is repealed, the prices increase to equilibrium, and lower-income residents are forced to leave.

Random • What kind of goods would governments place price ceilings?

Random • What kind of goods would governments place price ceilings? • Essential but generally too expensive.

Random • What happens when we have a minimum wage?

Random • What happens when we have a minimum wage? • In theory, businesses would hire fewer workers because they would have to pay higher than the equilibrium price.

Random • What happens when the supply of a good is greater than the consumer wants to buy, that is, how do we get rid of the surplus?

Random • What happens when the supply of a good is greater than the consumer wants to buy, that is, how do we get rid of the surplus? • Either the good remains unsold or the price drops (the latter more likely).

Random • Technology reduces production costs. If demand remains unchanged, what happens to the product sold? (Hint: Supply increases!)

Random • Technology reduces production costs. If demand remains unchanged, what happens to the product sold? (Hint: Supply increases!) • More goods will be sold at a lower price.