Download

1 / 45

450 likes | 459 Views

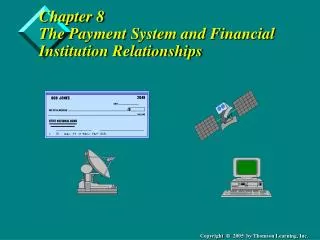

Chapter 8 The Payment System and Financial Institution Relationships. The Cash Flow Timeline. Order Order Sale Cash Placed Received Received

E N D

Chapter 8The Payment System and Financial Institution Relationships

The Cash Flow Timeline • Order Order Sale Cash • Placed Received Received • Accounts Collection • < Inventory > < Receivable > < Float > • Accounts Disbursement Time ==> • < Payable > < Float > • Invoice Payment Cash • Received Sent Paid

Learning Objectives • Explain, understand, and calculate float • Explain the roles of the two major components of the payment system • Describe the major paper-based and electronic-based payment systems • Understand the ACH and how its fits with the EDI • Use an availability schedule • Explain the uses of an account analysis statement

Value of Float • The delay in value transfer from the time a check is written until it finally is charged to the payor’s account. • Value of float is based on differences in present value based on time delay.

U.S. Payment System • Banking system • Payment mechanisms

Financial Institutions • Product differences, Ex 8.1 • Geographical restrictions • Safety considerations

Federal Reserve System • Organization, Ex 8.2, 8-3 • Fed’s involvement in payment system • Check clearing

Organization, Ex 8.2 • Board of Governors • FOMC • Federal Advisory Council • District banks, Fig 8.2 • Member banks

Fed’s Involvement • Circulate new money • Check processing, 16.5 billion checks/yr • Check settlement • ACH • FedWire • Regulate availability schedules

Check Clearing • MICR line, Exhibit 8.5 • Clearing process, Exhibit 8.4

MICR Line, Exhibit 8.5 • 2 digit Fed Bank Code • 2 digit Fed Office Code • 4 digit ABA Code • 1 digit verification code • Account number • Sequence number • Encoded amount

MICR CODE Pay to the xxxxxxxx7.75 Order of $ Dollars ABA Bank# Chk Sequence # Fed Bank Code Check Digit Fed District Code Account Number Encoded Field

2. Supplier (payee) receives 1. Customer sends check check 8. Customer’s bank account is debited 3. Supplier 6. Supplier’s account is credited deposits check 7. Check is presented for payment to customer’s bank Clearing agent: “on-us”, or Fed, or correspondent, or clearinghouse. 4. Check forwarded 5. Supplier’s bank is credited The Clearing Process, Exhibit 8.4 writes check

Clearing Mechanisms • House/On-us checks • Local items • Transit items

“On-us” Items • Payee deposits check in the bank on which it is drawn • Bank credit depositor’s account • Bank debits payor’s account

Local Items • Checks may be sent by courier to be swapped for checks drawn on itself at another bank • Checks may be processed through correspondent bank relationship • Local clearing house may be used

Transit Items • Direct send • Correspondent bank • Fed Reserve

Concept of Float • Types of float • Components of float

Types of Float • Collection float • Disbursement float

Components of Float • Mail float • Processing float • Clearing float

Fed Float • When the Fed grants the depositing bank credit according to a preset availability schedule, but is not always able to present the check to the drawee bank for payment within the same period. • Methods used to reduce float • check truncation • high-dollar group sort • inter-district transportation system • later presentment and deposit deadlines

Paper-Based Payments • Types • Ledger balance • Collected balance

Types • Checks • Drafts • DTCs

Ledger Balance • All credits and debits • Not all spendable

Collected Balance • Adjusted ledger • Reg CC, (2 and 5 days)

Electronic-Based Payments • Wire transfers • Automated clearinghouses • POS debit cards

International Payment Systems • Paper-based systems • Giro systems • Value dating • Electronic payments • Clearing House Interbank Payment System, CHIPS • Society for Worldwide Interbank Financial Telecommunications, SWIFT

Managing the Bank Relationship • Objectiveto ensure that all the company’s banking services are provided reliably at a reasonable cost

Services Provided • Collections • Payments • Information • Credit • Investments

Collections • Coin & currency • Standard check processing • Lockbox services • Electronic collections • Deposit reporting service

Payments • Demand deposit accounts • Zero balance accounts • Controlled disbursements • Payroll

Information • Balance reporting services • Account reconciliation • Electronic delivery systems • Advisory or consulting services

Credit • Shifting from a direct financing role • Moving toward role of risk-sharing or guarantor

Investments • Repurchase agreements • CDs • Commercial paper • Corporate agency services • Trends

Bank Selcction • Location • Bank/Company Fit • Service Quality and Breadth • Bank Creditworthiness • Bank Specialties • Price

Managing the Relationship • Account Analysis Statement, Ex 8-14 • Required Compensating Balance Calculation SCRCMP = ----------------- ecr (1-rr)(------)n 365 • Balances vs. Fees • Bank’s view: Advantages of Balances • Corp View: Disadvantages of balances

Bank’s View: Advanatages of Balances • Effect of increasing deposits for the bank • Balances can be lent • Form a cushion in case of loan default

Corp View: Disadvantages of Balances • ECR is < investment rate • Fees are tax deductible • Fees offer tangible expense that can be monitored • Fees are generally fixed and thus comparable, ECR floats

Daylight Overdrafts and the Availability Schedule • Define: when a bank’s Federal Reserve account book balance is negative during the day

Optimizing the Banking Network • Check list • what is bank’s compensation rate and how will it be paid, fees or balances, etc.? • if balances, over what time period? • multiyear agreement available with capped price increases? • compare a proforma account analysis statement • who is the account officer? • who is the customer service rep? • how will float be computed? • what performance guarantees are offered? • penalties for customer overdrafts?

NonBank Service Providers • Pepsico’s loan to Marriot • Almost half of all consumer and business loans held by nonbank companies • Third-party vendors of information between banks and companies

Financial System Trends • Nationwide banking in the US • Economic unification of Europe • Both of these will be catalysts for an ongoing drift toward concentration and globalization in the banking industry. • Imaging • Information services • Banking on the Internet • International aspects of banking relationships • Global bank consolidation

Summary • We developed the uniqueness of the US payment system and its major components • We discussed the role the Federal Reserve plays • We discussed the payment system using paper-based and electronic-based methods • We discussed bank selection and relationship management • We concluded with financial system trends