Download

1 / 23

260 likes | 539 Views

Chapter 7 Posting and Trial Balance. Main Points 1. General Ledger 2. Posting 3. Trial Balance Time Allocated: 4 Periods. Learning Objectives. In this chapter the students will learn: the nature of general ledger the meaning of posting

E N D

Chapter 7 Posting and Trial Balance Main Points 1.General Ledger 2. Posting 3. Trial Balance Time Allocated: 4 Periods

Learning Objectives In this chapterthe students will learn: • the nature of general ledger • the meaning of posting • the reason of the unbalance of the trial balance • how to post transactions from general journal to the general ledger • how to make a trial balance for ledger accounts

Revision (1) 1. What does the accounting cycle refer to? The accounting cycle refers to the accounting process that begins with the analysis of transactions to the closing of books. 2. What are the steps in the accounting cycle? 1) Identify the transactions from source documents. 2) Record the transactions in the journal. 3) Post journal entries to the ledger entries.

Revision (2) 4) Prepare the trial balance to make sure that debits equal credits. 5) Prepare adjusting entries to record accrued and deferred accounts. 6) Post adjusting entries to the ledger accounts. 7) Prepare adjusted trial balance. 8) Prepare the financial statements. 9) Prepare closing entries. 10) Post closing entries to the ledger accounts. 11) Prepare the post-closing financial balance.

Revision (3) 3. What is the function of source documents? Source documents are used as evidence that a particular transaction occurred. 4. What is the journal? The journal is the chronological record of business transactions. 5. When are transactions recorded in the journals? Transactions are recorded in the journals day by day.

What? Warm-up Discussion: 1. What’s the step in accounting cycle after recording the transactions in the journals? Transfer the transactions from the general journals to the general ledger. 2. What’s the next step then? Prepare the trial balance to make sure that debits equal credits.

Presentation When transactions occur throughout the accounting period, accountants identify the transactions from source documents, record the transactions in the journals, and then post the journals entries to the ledger entries. A business often sets up several ledgers including sales ledger, purchase ledger, and general ledgers. The general ledger is a collection of the business’ accounts, which is used to classify and summarize transactions to prepare data for financial statements.

1. Posting (1) Questions & Answers: 1. What is posting? Journal entries are transferred to the ledger. This process is called posting. 2. When is posting usually done? Posting is usually done after several entries have been made, for example, at the end of the day, depending on the number of transactions.

1. Posting (2) Practice: Post the transactions ( George Ross Photocopy Company’s transactions in March) from the general journal ( in Chapter 6) to the general ledger.

2. Trial Balance (1) Questions: 1. What’s the result caused by errors in the process of recording and calculating in the journal? 2. Does the balance of debits and credits mean that there is not any error during the recording and calculating? Why or why not? 3. What is the reason of the unbalance of the trial balance?

2. Trial Balance (1-1) Questions & Answers: 1. What’s the result caused by errors in the process of recording and calculating in the journal? -- The result is that the total of the debits do not equal the total of the credits. 2. Does the balance of debits and credits mean that there is not any error during the recording and calculating? -- No, it doesn’t.

2. Trial Balance (1-2) 3. What is the reason of the unbalance of the trial balance? -- The reason is calculating a ledger account balance wrongly or summarizing the debits and credits of the trial balance wrongly.

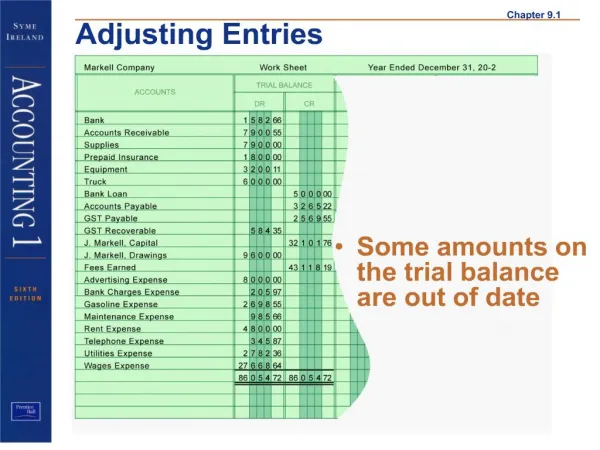

2. Trial Balance (2) Practice: Make the trial balance for the general ledger accounts ( George Ross Photocopy Company) on Page 46-49.

In-class Activities 1. Do further reading on Page 46-51 and get more information aboutposting and trial balance. 2. Do Exercise One on Page 51. Transfer the transactions happened in Grissom Agency from the general journal to the general ledger (posting) according to the general journal given, and then make a trial balance for the ledger accounts.

In-class Activities (1) Answers for Exercise One:

In-class Activities (8) Grissom Agency Trial balance May 31, 20 ××

Homework 1. Review Chapter 7 to get further understanding. 2. Do Exercise Two on Page 52 and write assignment. 3. Further discuss the two questions in Exercise Four on Page 54 with your partners after class. 4. Preview Chapter 8.